Click the icon to add a specified price to your Dashboard list. This makes it easy to keep track on the prices that matter most to you.

India’s factory output growth, as measured by the Index of Industrial Production (IIP), declined to 1.5 percent in June, marking a 10-month low due to contractions in mining and electricity sector output. The data reflects a broader manufacturing sector slowdown, driven by subdued overall activity following the early onset of the monsoon this year. According to the National Statistics Office (NSO), India’s industrial output growth slipped to 1.5 percent in June 2025, compared to an upwardly revised 1.9 percent (from 1.2 percent) in May. In comparison, IIP growth in June 2024 stood at 4.9 percent. The June 2025 figure marks the slowest growth since August 2024, when factory output remained flat.

According to the National Statistics Office (NSO), India’s industrial output growth slipped to 1.5 percent in June 2025, compared to an upwardly revised 1.9 percent (from 1.2 percent) in May. In comparison, IIP growth in June 2024 stood at 4.9 percent. The June 2025 figure marks the slowest growth since August 2024, when factory output remained flat.

Rajani Sinha, Chief Economist at Care Ratings Ltd, said, “Growth in India’s industrial production slowed to 1.5 percent in June, compared to an upwardly revised 1.9 percent in May. A marginal pickup in manufacturing sector growth was more than offset by contractions in both mining and electricity sector output. IIP growth has remained relatively subdued in recent months, with growth for the April–June 2025 quarter at 2 percent—significantly lower than the 5.4 percent recorded in the same quarter last year.”

Sector-wise growth

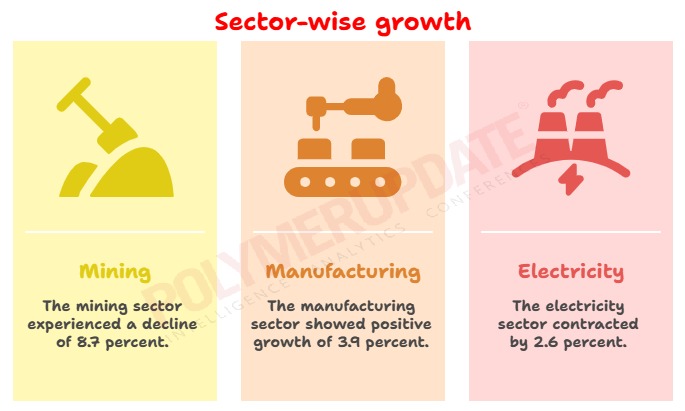

The growth rates of the three sectors—mining, manufacturing, and electricity—for June 2025 were (-)8.7 percent, 3.9 percent, and (-)2.6 percent, respectively. The Index of Industrial Production (IIP) for the same month stood at 123.2 for mining, 152.3 for manufacturing, and 217.1 for electricity.

Within the manufacturing sector, 15 out of 23 industry groups recorded positive growth in June 2025 compared to June 2024. The top three contributors to growth during the month were manufacture of basic metals (9.6 percent), manufacture of coke and refined petroleum products (4.2 percent), and manufacture of fabricated metal products, except machinery and equipment (15.2 percent).

In the basic metals group, item categories such as MS slabs, HR coils and sheets of mild steel, and pipes and tubes of steel contributed significantly to the growth. In the manufacture of coke and refined petroleum products category, diesel, naphtha, and petrol/motor spirit were the key growth drivers.

Similarly, in the manufacture of fabricated metal products, except machinery and equipment group, steel frameworks or skeletons for construction of towers including pit props, fabricated metal products including forged blanks, and stainless steel utensils were the major contributors to growth.

Sinha added, “On the investment front, infrastructure and construction goods posted a healthy 7.2 percent growth in June, up from 6.7 percent in May. While private capex is yet to show meaningful traction, public capex continues to remain encouraging. However, persistent global uncertainties are weighing on overall investment sentiment.”

Use-based classification

As per the use-based classification, the indices for June 2025 stood at 151.3 for primary goods, 115.2 for capital goods, 167.9 for intermediate goods, and 198.3 for infrastructure/construction goods. Additionally, the indices for consumer durables and consumer non-durables were recorded at 130.8 and 144.6, respectively, according to NSO data.

The corresponding year-on-year growth rates of the IIP by use-based classification for June 2025 were (-)3.0 percent for primary goods, 3.5 percent for capital goods, 5.5 percent for intermediate goods, 7.2 percent for infrastructure/construction goods, 2.9 percent for consumer durables, and (-)0.4 percent for consumer non-durables. Based on this classification, the top three contributors to IIP growth in June 2025 were infrastructure/construction goods, intermediate goods, and consumer durables.

Meanwhile, demand-side signals remained mixed in June 2025. Output of consumer non-durable goods continued to weaken, remaining in the contractionary zone for the fifth consecutive month, while output of consumer durable goods improved. Urban consumption, in particular, continues to lag.

Nonetheless, consistent easing of inflation, a favourable monsoon, and recent policy rate cuts by the Reserve Bank of India (RBI) are positives for the consumption outlook. Against this backdrop, both demand and investment trends will need to be monitored closely in the coming months.

DILIP KUMAR JHA

Editor

dilip.jha@polymerupdate.com