Click the icon to add a specified price to your Dashboard list. This makes it easy to keep track on the prices that matter most to you.

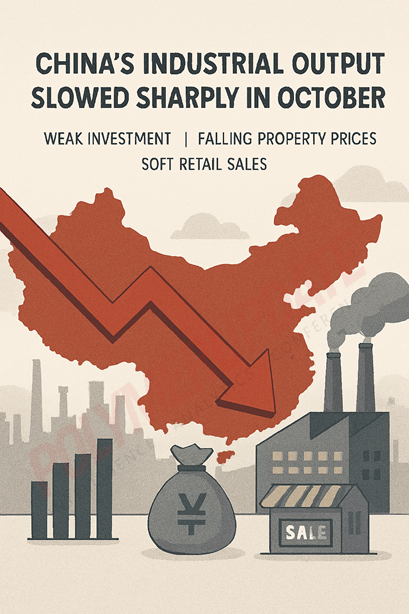

In a major setback for overall economic growth, China’s National Bureau of Statistics (NBS) reported industrial output growth of 4.9 percent in October, the weakest pace in over a year, due to the trade war with the United States and sluggish domestic consumption. On a monthly basis, industrial output rose by 0.17 percent. U.S. President Donald Trump has repeatedly threatened to impose punitive tariffs on Chinese imports, citing Beijing’s continued crude oil purchases from Russia, which has been at war with Ukraine since February 2022. China’s industrial growth in October marked a slowdown from the 6.5 percent increase recorded in September 2025 and fell short of analysts’ expectations of 5.5 percent. Notably, the October 2025 performance was weaker than the 5.3 percent growth posted in the same month last year and represented the softest increase since August 2024. Although the Chinese government attempted to offset weak domestic consumption by ramping up exports, it failed to gain the expected traction amid global economic uncertainty triggered by geopolitical conflicts and U.S. tariff measures imposed on countries worldwide.

China’s industrial growth in October marked a slowdown from the 6.5 percent increase recorded in September 2025 and fell short of analysts’ expectations of 5.5 percent. Notably, the October 2025 performance was weaker than the 5.3 percent growth posted in the same month last year and represented the softest increase since August 2024. Although the Chinese government attempted to offset weak domestic consumption by ramping up exports, it failed to gain the expected traction amid global economic uncertainty triggered by geopolitical conflicts and U.S. tariff measures imposed on countries worldwide.

China's key activity indicators continued to decelerate in October as policymakers appear to be delaying additional stimulus. While this year’s growth target may require only limited further support to be met, more robust policy measures will be essential to achieve long-term goals. China’s exports unexpectedly fell in October as producers struggled to maintain profitability in other markets after months of front-loading to pre-empt Trump’s tariff threats. Fu Linghui, an NBS spokesperson, said, “The external environment remains fraught with instability and uncertainty, while domestic structural adjustments face considerable pressure.”

Sector-wise performance

According to NBS data, China’s manufacturing activity slowed to 4.9 percent in October from 7.3 percent in September, while mining output rose by 4.5 percent compared with 6.4 percent in the previous month, partly due to the Golden Week holiday. During this period, consumption activity typically increases, but such support was absent this year, unlike in previous years. Meanwhile, production in the electricity, heat, gas, and water sector accelerated to 5.4 percent in October 2025, up from 0.6 percent in September 2025.

Within manufacturing, 29 of the 41 major industries recorded growth, including automotive (16.8 percent), computers and communications (8.9 percent), railway and shipbuilding (15.2 percent), ferrous metal smelting and rolling (1.4 percent), non-ferrous metal smelting and rolling (3.7 percent), chemical products (7.1 percent), coal mining and washing (6.5 percent), oil and gas (1.9 percent), food manufacturing (2.5 percent), heat production (5.9 percent), and textiles (0.2 percent). For the first ten months of the year, industrial production increased by 6.1 percent.

Slump in fixed asset investment

China’s fixed asset investment fell further by 1.7 percent year-over-year (yoy) year-to-date (ytd), marking the lowest level since June 2020. Once again, the data fell well short of already subdued forecasts. By category, infrastructure investment slipped into contraction territory at (–)0.1 percent yoy ytd, marking its first decline since 2020. Manufacturing investment, which had been a strong outperformer for several years, dropped to 2.7 percent yoy ytd. Private-sector investment declined 4.5 percent yoy ytd, while even government investment slowed to 0.1 percent yoy ytd, and appears likely to fall into contraction next month.

Lynn Song, Chief Economist for Greater China at ING Economics, stated, “The only silver linings were seen in China’s recent growth areas, namely the auto sector (17.5 percent) and rail, ships, and aeroplanes (20.1 percent). While the magnitude of the declines was somewhat surprising, the continued weakness of investment itself was not. Anti-involution policies targeting excessive price competition and the shift toward reducing redundant investments could be adding to the downward pressure.”

Recent credit data showed that new renminbi (RMB) loans contracted by RMB 20.1 billion in October. While October is typically a seasonally weak month due to the Golden Week holidays, the lack of borrowing demand has been evident ytd, with new RMB loans down 7.4 percent ytd. This suggests that real interest rates remain too high to attract potential borrowers.

Persisting property pressures

Property prices across 70 cities in October continued to face downward pressure, with new home prices falling 0.45 percent month-on-month (mom)—the steepest decline since October 2024. Used home prices dropped 0.66 percent mom, the sharpest fall since September 2024. After remaining flat in the first quarter, prices have been declining at an accelerating pace. From their peaks, new home prices are now down 11.8 percent, while used home prices have fallen 20.3 percent. Of the 70 cities, 45 have seen secondary market prices decline between 20 percent and 30 percent from their peaks, while three cities have recorded drops of more than 30 percent.

In the primary market, only six of the 70 cities saw prices stabilise or rise, the lowest proportion since September 2024. In the secondary market, October marked the second consecutive month in which not a single city recorded stable or increasing prices. With prices falling and inventory levels still elevated, it is unsurprising that property investment remains one of the major drags on the economy, with investment now down 14.7 percent yoy ytd. The recent downturn—characterised by accelerating price declines—has yet to be adequately addressed. More robust policy support will be needed to prevent a significant erosion of household wealth, which would severely undermine efforts to transition toward a consumption-driven growth model.

Retail sales moderation

China’s retail sales growth slowed to 2.9 percent year-on-year (yoy), down only 0.1 percentage point (pp) from September’s reading. This was slightly stronger than market expectations. Year-to-date (ytd), retail sales are up 4.3 percent yoy in October and should still finish 2025 above last year’s 3.5 percent growth for the same period. However, the loss of momentum in the second half of the year remains somewhat disappointing given the government’s emphasis on boosting domestic demand.

The impact of the trade-in policy continues to fade. Key beneficiary categories—including household appliances, communication equipment, and furniture—have all been on a declining trend. Household appliance sales in particular plunged 14.6 percent yoy in October, partly due to an unfavourable base effect created by similar promotions in 2024. This pattern was previously observed in auto sales, one of the earliest beneficiaries of the trade-in programme. A similar drag is likely to emerge for communication appliances early next year.

Outlook

In 2024, China’s total export revenue stood at approximately US$ 3.6 trillion, with the United States accounting for roughly US$ 438.95 billion of that total (based on U.S. import data from China). While the trade-in policy has been successful in front-loading consumption this year, a new policy direction will likely be needed to support consumption next year.

DILIP KUMAR JHA

Editor

dilip.jha@polymerupdate.com