Click the icon to add a specified price to your Dashboard list. This makes it easy to keep track on the prices that matter most to you.

This week, Polypropylene prices down adjusted in the Asian region.

An industry source in Asia, on condition of anonymity, informed a Polymerupdate team member, “Despite the International Energy Agency (IEA) lowering its global oil demand growth projections, the bearish effect on crude oil prices has been minimal. This is largely due to a decrease in worries regarding potential trade conflicts, following the U.S. decision to implement a 90-day suspension on increased tariff rates.”

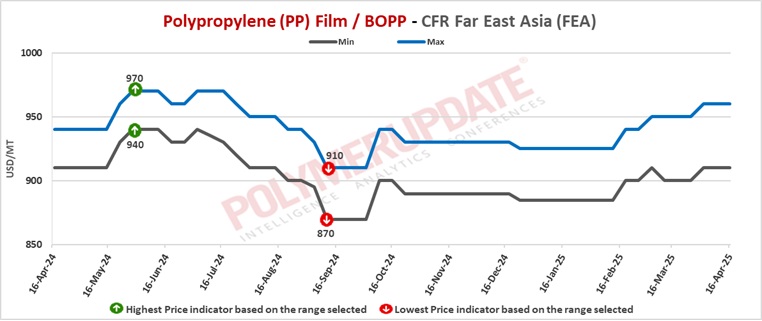

The source added, “The decline in prices for polypropylene (PP) was primarily attributed to reduced import offers from international suppliers and a lack of strong purchasing interest in the region.” In Far East Asia, PP raffia and PP injection prices were assessed at the USD 860-910/mt CFR levels, both lowered by USD (-5/NC/mt) week on week. PP BOPP prices were assessed at the USD 880-930/mt CFR levels, a week on week decrease of USD (-10/NC/mt). Meanwhile, PP block copolymer prices were assessed at the USD 920-950/mt CFR levels and PP film were assessed at the USD 910-960/mt CFR levels, both rolled over from the previous week.

In Far East Asia, PP raffia and PP injection prices were assessed at the USD 860-910/mt CFR levels, both lowered by USD (-5/NC/mt) week on week. PP BOPP prices were assessed at the USD 880-930/mt CFR levels, a week on week decrease of USD (-10/NC/mt). Meanwhile, PP block copolymer prices were assessed at the USD 920-950/mt CFR levels and PP film were assessed at the USD 910-960/mt CFR levels, both rolled over from the previous week.

In China, Middle eastern producers have offered their PP raffia and PP injection at the USD 860-910/mt levels, for shipment in May 2025.

In China, the polypropylene market is currently facing considerable overcapacity, exacerbated by a decline in new orders from downstream industries. There has been a noticeable decrease in interest for international orders, which has further stalled market prices. While it is more probable that polypropylene prices will decline, they are encountering obstacles to any potential increase, leading to increased caution within the industry and a growing bearish outlook.

A prevailing atmosphere of risk aversion characterizes the polypropylene market, as the effects of tariff policies have resulted in a significant reduction in overseas inquiries and a marked decline in export activities. As a result, overall downstream demand remains weak, prompting terminal factories to take a more cautious stance on procurement.

This situation has worsened the existing supply-demand imbalance. On the demand front, there has been no notable improvement, with the turnover of industrial chain inventories remaining sluggish. The decrease in overseas inquiries, influenced by tariff policies, has further affected export transactions, complicating resource consumption. Currently, weak demand is the primary driver of fluctuations in polypropylene prices.

In the Chinese domestic market, buying activity was subdued as the majority of market participants were occupied with ChinaPlas 2025.

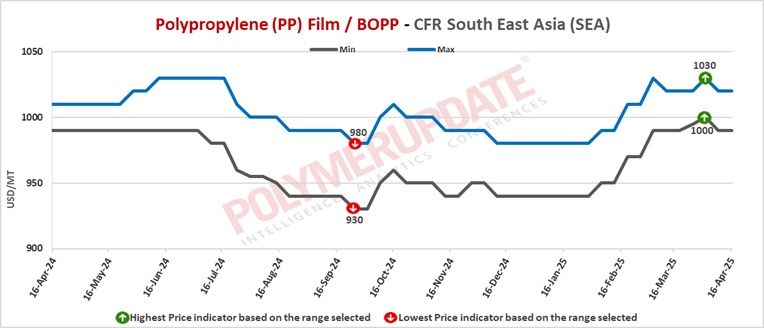

In Southeast Asia, PP raffia and PP injection grade prices were assessed at the USD 930-960/mt CFR levels, both week on week down USD (-10mt). PP film prices were assessed at the USD 990-1020/mt CFR levels, a drop of USD (-10/mt) from the previous week. BOPP prices were assessed at the USD 950-990/mt CFR levels while PP block copolymer prices were assessed at the USD 1000-1020/mt CFR levels, both week on week decreased by USD (-10/mt).

In Indonesia, a Chinese producer concluded deal for PP raffia and PP injection grade at the USD 950-960/mt levels, for shipment in May 2025.

In Thailand, a producer from China has closed deal for PP raffia and PP injection grade at the USD 935/mt, for shipment in May 2025.

Meanwhile, in Southeast Asia, some Chinese producers have offered their PP raffia and injection grade in the range of USD 920-950/mt, for shipment in May 2025.

In Southeast Asia, polypropylene (PP) prices have experienced a slight decline. Some suppliers have begun to offer May shipments at minor discounts due to a notable decrease in buyer demand. Regional producers had anticipated improved profit margins in April, driven by lower feedstock costs, such as naphtha. However, buyers are likely to advocate for reduced prices as well, particularly in light of the ongoing tariff situation.

The new tariffs imposed by the Trump administration on Chinese imports to the United States, effective April 9, have raised concerns about diminished demand in the Asia-Pacific region. Additionally, market participants are closely monitoring PP price trends in China, as demand may also decrease there. In Malaysia, PRefChem, a major player in the petrochemical sector, is expected to resume partial operations at its refinery in May. Their No.2 PP plant, with a capacity of 450,000 tons per year, is scheduled to restart, while the No.1 plant, also with a capacity of 450,000 tons per year, has been intermittently operational since February. These additional volumes are likely to contribute to the regional supply in the near future.

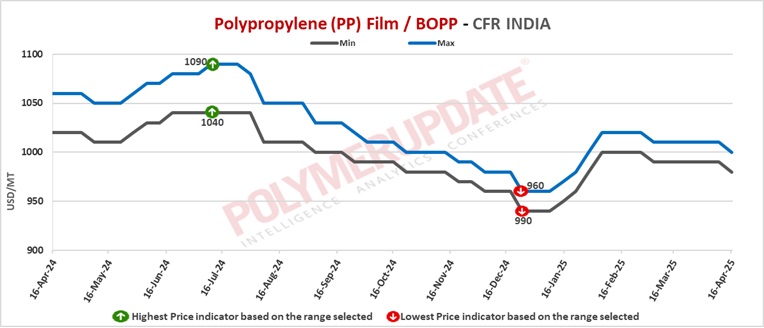

In India, PP raffia and PP injection prices were assessed at the USD 950-970/mt CFR levels, a week on week drop of (-10/mt). PP film and BOPP prices were assessed at the USD 980-1000/mt CFR levels, a week on week decline of USD (-10/mt). PP block copolymer prices were assessed at the USD 1000-1010/mt CFR levels, down adjusted by USD (-10/mt) from last week.

In India, Middle eastern producers have offered their PP raffia and PP injection at the USD 950-970/mt levels, for shipment in May 2025.

In India, market participants adopted a cautious approach this week following the introduction of significant new tariffs by the United States. Purchasing activity diminished, as many opted to remain on the sidelines to assess the situation before committing to transactions. There is a widespread anticipation that prices may decline due to the prevailing uncertainty surrounding the reciprocal tariffs.

Additionally, downstream demand is experiencing pressure from the newly imposed levies, particularly within the polymers sector. Spot demand is projected to remain subdued this month, with limited potential for recovery. In India, prices for PP homo-grade have decreased due to tepid demand and softer pricing trends. Buyers are postponing purchases in hopes of securing better deals in light of falling crude oil prices and escalating concerns regarding global trade tensions.

Conversely, prices for PP block co-polymer have remained stable, primarily due to a reduction in offers and tighter supply conditions. The recent US tariffs on Chinese imports are prompting concerns about their broader economic implications. One potential consequence could be an increase in PP exports from China to markets such as India, which may negatively affect local market sentiment. However, a domestic plant shutdown is anticipated soon, which could restrict local supply and sustain import demand, thereby mitigating some of the adverse market sentiments.

In Pakistan, PP raffia and PP injection grade prices were assessed at the USD 950-990/mt CFR levels, both dropped by USD (-10/mt) from the previous week. PP film and BOPP prices were assessed at the USD 990-1040/mt CFR levels, both week on week lower by USD (-10/mt). PP block copolymer prices were assessed at the USD 1000-1070/mt CFR levels, a fall of USD (-10/mt) from the previous week.

In Pakistan, Middle eastern producers have offered their PP raffia and PP injection at the USD 950-990/mt levels, for shipment in May 2025.

In Pakistan, the recent decision by the U.S. government to postpone tariff increases on imports has been positively received by local converters. However, the general market sentiment remains negative. Nevertheless, in the Pakistan and Bangladesh markets, restocking activities are expected to pick up pace with the approaching Eid ul-Adha festival in early June.

In Sri Lanka, PP raffia and PP injection grade prices were assessed at the USD 1000-1040/mt CFR levels, both down USD (NC/-10/mt) from the previous week. PP film and BOPP prices were assessed at the USD 1050-1070/mt CFR levels, both dropped week on week by USD (NC/-10/mt). PP block copolymer prices were assessed at the USD 1070-1080/mt CFR levels, lower by USD (NC/-10/mt) from last week.

In Sri Lanka, Middle Eastern producers have offered their PP raffia and PP injection at the USD 1000-1040/mt levels, for shipment in May 2025.

In Sri Lanka, the decision by the U.S. to delay tariff hikes on imports has been positively received by domestic converters. Nevertheless, the general market outlook remains pessimistic, primarily due to persistent political instability. Additionally, purchasing activity was subdued because of a national holiday in the region.

In Bangladesh, PP raffia and PP injection prices were assessed at the USD 980-1010/mt CFR levels, both down adjusted by USD (-10/mt) from the previous week. PP film and BOPP prices were assessed at the USD 1000-1030/mt CFR levels, both week on week declined by USD (-10/mt). PP block copolymer prices were assessed at the USD 1040-1090/mt CFR levels, a fall of USD (-10/mt) from the previous week.

In Bangladesh, Middle eastern producers have offered their PP raffia and PP injection at the USD 980-1010/mt levels, for shipment in May 2025.

In Bangladesh, the recent choice by the U.S. government to delay tariff hikes on imports has been positively welcomed by domestic converters. Nevertheless, the general market outlook continues to be pessimistic, largely attributed to persistent political instability. Conversely, with Eid ul-Adha approaching in early June, restocking activities are likely to pick up.

Market players are optimistic that prices may decline further as a result of ongoing trade tensions. This hesitation could result in lower sales and accumulation of inventory for sellers.

Feedstock propylene prices on Tuesday were assessed at the USD 820-830/mt CFR China levels, an increase of USD (+5/mt) from the previous week. FOB Korea propylene prices were assessed at the USD 780-790/mt levels, a week on week fall of USD (-15/mt).

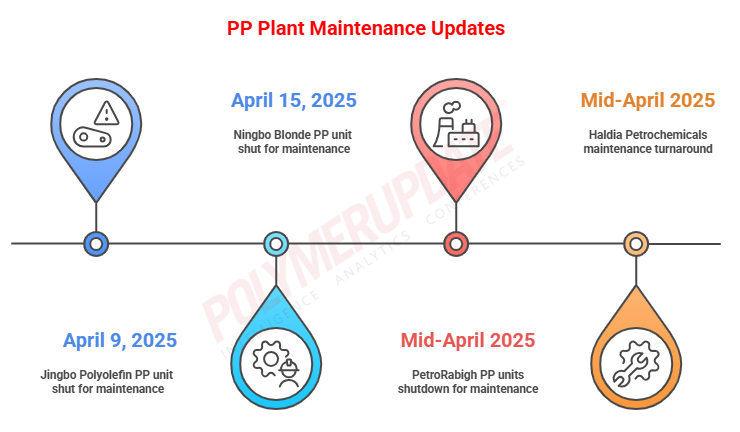

In plant news, Rabigh Refining and Petrochemical Co (PetroRabigh) has shut down its No.1 and No.2 polypropylene (PP) units from mid-April 2025. The units are slated to remain offline for about 60 days. Located in Rabigh, Saudi Arabia, the two PP units have individual production capacities of 350,000 mt/year.

In other plant news, Haldia Petrochemicals ltd (HPL) is likely to start maintenance turnaround at its petrochemical complex by mid-April 2025. The shutdown is expected to remain in force until end May 2025. Located in Haldia in the eastern Indian state of west Bengal, the complex comprises a cracker with an ethylene capacity of 700,000 mt/year and propylene capacity of 350,000 mt/year. Downstream units at the complex comprise a PP unit with a production capacity of 350,000 mt/year.