Click the icon to add a specified price to your Dashboard list. This makes it easy to keep track on the prices that matter most to you.

The United States’ 50 percent tariff on imports from India could lead to a single-digit decline in revenue for the Indian chemical industry, according to a recent study by rating firm India Ratings & Research published on Tuesday. The decline could extend to the low teens for companies with significant exposure to non-exempt products exported to the United States. The direct impact of tariffs on profitability is expected to be limited to 10–15 percent of profit margins but will depend on additional tariff cost-sharing arrangements. Given the varying dynamics across different chemical segments, the impact of tariffs will not be uniform across the sector. Domestically focused companies engaged in products not exported to the United States are likely to see minimal impact, while entities with higher exposure to non-exempt products in the US market could face greater pressure.

Given the varying dynamics across different chemical segments, the impact of tariffs will not be uniform across the sector. Domestically focused companies engaged in products not exported to the United States are likely to see minimal impact, while entities with higher exposure to non-exempt products in the US market could face greater pressure.

Effective August 1, the United States imposed a 25 percent reciprocal tariff on Indian-origin goods, which was raised to 50 percent effective August 27, 2025, along with an additional 25 percent penal tariff on India for purchasing Russian crude oil. The United States accounts for around 15 percent of India’s exports, of which nearly half fall under the exempted products category.

Demand equation

The direct impact of tariffs on the sector’s profitability for the year is likely to be limited to 10–15 percent of Earnings Before Interest, Tax, Depreciation, and Amortization (EBITDA) margins, with the China demand-supply balance remaining a key determinant of global chemical prices and profitability. Although still below the cyclical average, lower price erosion is expected to cushion the sector’s EBITDA in FY 2025–26. The sector’s EBITDA margins recovered marginally to 14 percent during January–June 2025, compared with an average of 13 percent in the past four quarters, as inventory losses narrowed and volumes improved.

“Domestic demand is likely to remain healthy in FY 2025–26, as growth in end-user industries enables chemical companies catering to the domestic market to outperform their export-focused peers. Moreover, the balance sheets of most players have sufficient headroom to manage any immediate pressure on profitability and credit profiles. However, companies undertaking large capex projects or medium, small, and micro enterprises (MSMEs) with limited liquidity and financial flexibility could face challenges in the near term,” said Siddharth Rego, Associate Director, India Ratings & Research.

Turning from a turnaround

Most of the portfolio maintains comfortable liquidity, except for a few entities undertaking large capex projects. About 12 percent of the chemical portfolio was under a negative directional indicator as of end-August 2025. The Indian chemical sector was poised for a turnaround in FY 2025–26, driven by volume growth, gradual moderation in channel inventories, and near-bottoming of prices after two weak years. This trend was reflected in the improving performance during January–June 2025. However, the uncertainty and disruption stemming from the higher US tariff rate effective August 27, 2025, could affect near-term performance.

Exports are expected to remain under pressure amid muted global demand, further exacerbated by the elevated tariffs. The US accounts for nearly 15 percent of India’s chemical exports, with tariff rates now higher than those imposed on competing countries such as China, Canada, Mexico, Germany, and Ireland. Although India’s cost structure remains competitive compared with European producers, the tariff differential could offset this advantage, particularly impacting specialty chemical players. The silver lining is that roughly half of India’s exports to the US fall under the exempt list, limiting the first-order impact.

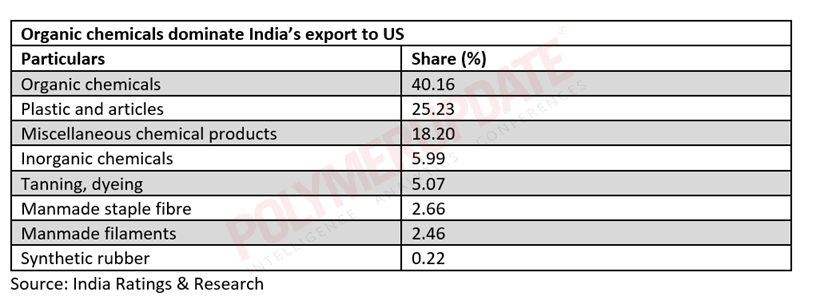

Organic chemicals and agrochemicals constitute the largest share of India’s chemical exports to the US. Dyes and inorganic chemicals have less than 10 percent exposure to the US market and will therefore experience limited direct impact. However, a slowdown in the textile sector, due to weaker export demand and the US tariffs, could dampen demand for dyes.

Shipment down

US bound chemical shipments slowed down in September 2025, even as discussions and negotiations are on with customers on possible sharing of the additional cost. While typically a critical component, the cost of chemicals is often a small part of the total value of the product, which may enable a higher pass-through to the end user in some cases. Furthermore, some large specialty chemical players are global leaders in their products with a high level of integration in the value-chain, placing them at a relative advantage compared to small players that may be easily replaced.

Given India’s relative tariff disadvantage over competing countries, the risk of losing market share does exist. The extent of market share loss will depend on the interplay of a) the share of the customer’s business, b) the criticality of the chemical in the final product performance, c) the proportion of the cost of the end-product, d) the scale of integration and cost competitiveness determining the ability to absorb additional cost, and e) the customer’s focus on supplying chain diversification.

Declining China’s share

China’s share in the US chemical imports declined to around 10 percent in 2023-2024 from an average of 12.8 percent during 2018-2022. However, India’s share remained largely stable at 3.5-4 percent over 2018-2024, indicating Indian exporters’ inability to gain the market share lost by China. However, the US remains India’s key chemical export destination. India’s chemical exports in FY2024-25 stood at US$ 34.6 billion, of which the US accounts for roughly 13 percent.

Players are also in discussion with other export customers, particularly in Europe and Latin America, to increase their market share, though that will happen only gradually. However, discussions with the US on tariff/trade deals has resumed due to which the current situation could change. While the reversal in India’s tariff differential with China limits the benefits of China+1 supply chain re-orientation, it also reduces some of the risks of excess capacities finding their way into the Indian markets.

DILIP KUMAR JHA

Editor

dilip.jha@polymerupdate.com