Click the icon to add a specified price to your Dashboard list. This makes it easy to keep track on the prices that matter most to you.

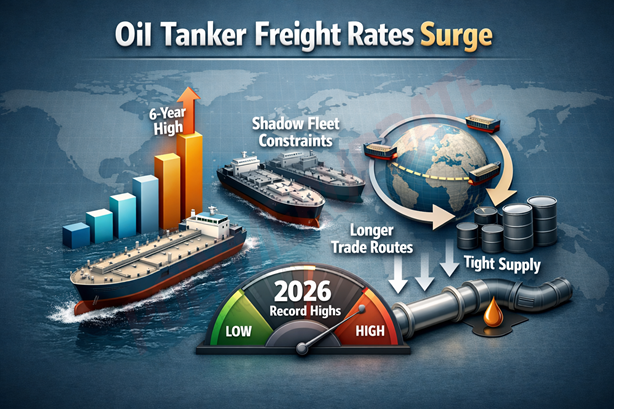

Global oil tanker freight rates have surged to their highest levels in six years, driven by escalating geopolitical tensions, tighter vessel availability, and longer trade routes that have significantly increased shipping demand, especially from the Middle East to global destinations. Fears of imminent U.S. attacks on Iran and the escalating Russia–Ukraine conflict have fuelled crude oil shipping rates, further supported by the partial shutdown of the Strait of Hormuz — a crucial maritime chokepoint connecting the Persian Gulf to the Gulf of Oman and transporting nearly 20 percent of the world’s crude oil supply. Spot earnings for Very Large Crude Carriers (VLCCs) — the workhorses of long-haul crude transport — have climbed sharply on key Middle East-to-Asia routes in recent weeks. The rally marks a dramatic turnaround from the softer conditions seen earlier, underscoring how quickly freight markets can tighten when geopolitical and structural factors converge.

Spot earnings for Very Large Crude Carriers (VLCCs) — the workhorses of long-haul crude transport — have climbed sharply on key Middle East-to-Asia routes in recent weeks. The rally marks a dramatic turnaround from the softer conditions seen earlier, underscoring how quickly freight markets can tighten when geopolitical and structural factors converge.

Prevailing rates

Oil tanker rates in early 2026 have surged to six-year highs, with Very Large Crude Carrier (VLCC) earnings exceeding $170,000 per day in February 2026. The rally has been driven by stronger demand for Middle Eastern crude, escalating geopolitical tensions — particularly fears of a potential U.S.–Iran conflict — and the expansion of the “shadow fleet,” which has reduced the number of vessels available in the mainstream market. The primary drivers include robust tanker demand in the Middle East, rising crude imports by India, and precautionary hoarding of shipping capacity amid concerns over possible U.S.–Iran hostilities.

VLCC rates on the Middle East-to-China route tripled to over US$150,000–170,000 per day by late February 2026, marking their highest levels since early 2020. Mid-size crude tankers also demonstrated notable strength in early 2026, despite a slight decline in overall cargo volumes in January. Meanwhile, the “shadow fleet” — comprising more than 900 tankers operating under or circumventing sanctions — has further tightened effective vessel supply for mainstream oil companies, thereby pushing freight rates higher.

Geopolitical tensions fuel risk premium

A primary trigger behind the spike has been heightened tensions in the Middle East, particularly involving Iran and the United States. Concerns over potential disruptions to crude flows through critical chokepoints such as the Strait of Hormuz have prompted charterers to secure vessels more aggressively.

This precautionary booking has reduced the availability of prompt tonnage, pushing up daily charter rates. At the same time, war-risk insurance premiums for vessels operating in sensitive waters have increased, adding to overall freight costs. Market participants say that even the perception of risk — rather than an actual supply disruption — has been enough to drive volatility in tanker markets.

Strong Middle East exports lift demand

Higher crude exports from key Gulf producers have also supported rates. Robust flows to Asia, particularly India and China, have sustained demand for VLCCs on long-haul voyages.

The shift in trade patterns following Western sanctions on Russian crude has further reshaped global oil flows. Many cargoes are now traveling longer distances, increasing so-called “ton-mile demand” — a measure of cargo volume multiplied by distance travelled. Even if total global oil demand grows modestly, longer voyages alone can significantly tighten vessel supply.

Shadow fleet and ageing vessels constrain supply

Another structural factor supporting freight rates is limited effective fleet availability. A sizeable number of older tankers has moved into the so-called “shadow fleet,” transporting sanctioned oil outside mainstream insurance and regulatory systems. These vessels are largely unavailable to major oil companies and established traders.

Additionally, a significant portion of the global tanker fleet is more than 15 years old, raising maintenance costs and compliance challenges amid tightening environmental regulations. This has constrained usable supply at a time when demand for compliant tonnage remains firm. New vessel deliveries are scheduled over the next few years, but the current orderbook remains moderate compared with previous shipping cycles, limiting immediate relief on the supply side.

Impact on crude trade and refiners

Elevated tanker rates increase the landed cost of crude, particularly for barrels shipped over long distances. This can erode refining margins and alter crude selection strategies.

For instance, higher freight costs may make geographically closer grades more competitive versus Atlantic Basin barrels destined for Asia. Traders note that freight volatility is increasingly influencing arbitrage economics, sometimes as much as the underlying crude price differentials.

Outlook

In the near term, tanker markets are expected to remain sensitive to geopolitical developments. Any escalation in Middle East tensions could drive rates even higher due to increased risk premiums and further vessel hoarding. Conversely, diplomatic de-escalation could cool sentiment and soften freight levels.

Over the medium term, the balance between fleet growth and global oil demand will be crucial. If crude trade continues to fragment along geopolitical lines — leading to longer and more complex shipping routes — tanker demand could remain structurally supported.

However, a slowdown in global oil consumption growth or a significant influx of new vessels could eventually ease current tightness. For now, the surge in tanker rates highlights a broader reality: in an increasingly fragmented energy market, shipping costs have become a critical variable in global oil pricing, reflecting not just supply and demand fundamentals but also geopolitical risk and evolving trade patterns.

DILIP KUMAR JHA

Editor

dilip.jha@polymerupdate.com