In India, Russia’s Rosneft-backed Nayara Energy Ltd is planning to 35-day maintenance shutdown early April which comes in the wake of global oil and gas supply constraints, emanating from escalating West Asia crisis. Mangalore Refinery and Petrochemicals Ltd (MRPL) has temporarily shut one of its 100,000 barrels per day (bpd) crude oil refinery units and several secondary processing units, including a hydrocracker, at its 300,000 bpd facility in Karnataka. Reliance Industries Ltd (RIL) has cut aromatics production, resulting in a loss of 75,000 tonnes of paraxylene (PX) output.

In South Korea, large-scale facilities at the Yeosu Petrochemical Complex in Jeollanam-do were successively halted on March 23, 2026. Leading chemical company LG Chem stopped operations at its naphtha cracker (NCC) facility producing ethylene at its Yeosu Plant 2, and nearby Yeochun NCC also halted operations at its propylene plant (OCU), another key product.

These are some examples of petrochemical plants shutdown in recent weeks due to unavailability of oil and gas. Since the West Asia crisis erupted on February 28, 2026, after Israel and the United States jointly attacked Iran and Tehran retaliated with attacks on Israeli cities and American infrastructure and military installations in the Middle East. Additionally, Iran blocked the Strait of Hormuz, the key transit line connecting Asia with Europe and the Americas and handling around a fifth of global crude oil supply.

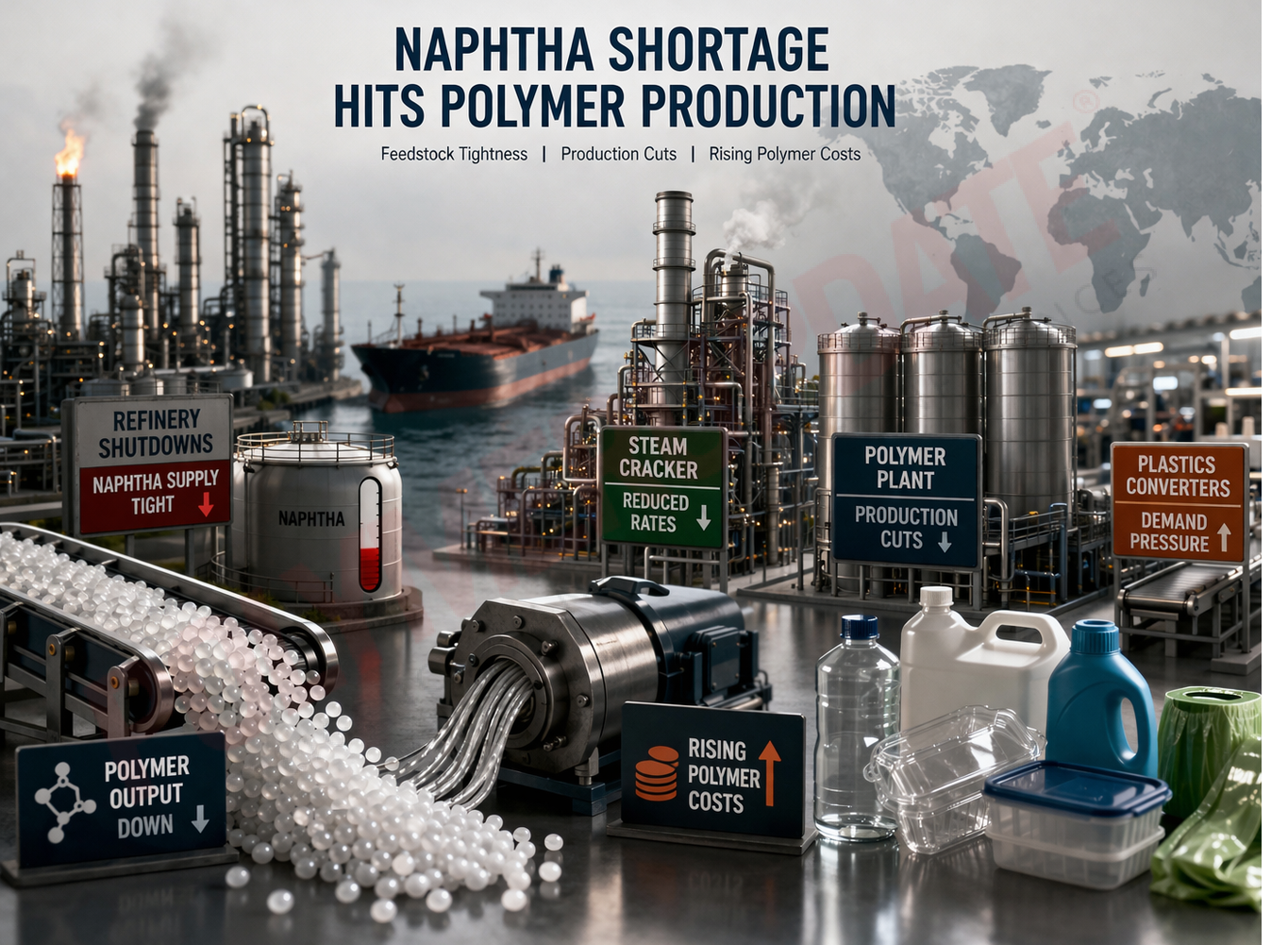

Deepening crisisThe global petrochemical industry is grappling with a deepening crisis as a shortage of naphtha—its most critical feedstock—disrupts production, squeezes margins, and exposes structural vulnerabilities in supply chains. Triggered by geopolitical tensions, refinery outages, and logistical bottlenecks, the shortage has sent shockwaves across Asia and Europe, where petrochemical manufacturing is heavily dependent on naphtha-based cracking. At its core, the issue underscores a fundamental reality: naphtha is not merely another refined product, but the backbone of global petrochemical production.

Naphtha is a key input for steam crackers, which produce essential building blocks such as ethylene, propylene, and aromatics. These derivatives form the foundation of a vast range of downstream industries—from plastics and packaging to textiles, automobiles, and construction materials.

In Asia and Europe, a significant portion of petrochemical capacity is designed to run on naphtha. Unlike the United States, where ethane-based production dominates due to abundant shale gas, many producers in these regions have limited flexibility to switch feedstocks. As a result, any disruption in naphtha supply has an immediate and disproportionate impact on production and profitability.

Supply disruptions and production cutsThe current shortage has been exacerbated by ongoing geopolitical tensions in key energy corridors, particularly in the Middle East, which accounts for a substantial share of global naphtha exports. Disruptions in shipping routes and uncertainty surrounding crude flows have tightened availability, while refinery outages—both planned and unplanned—have further constrained supply.

Petrochemical manufacturers across Asia have responded by cutting operating rates, with some forced to temporarily shut down crackers due to the unavailability or high cost of feedstock. These production cuts are beginning to ripple through the global supply chain, raising concerns over the availability of key petrochemical products.

The surge in naphtha prices, closely linked to crude oil benchmarks, has significantly eroded margins for petrochemical producers. Non-integrated players—those without upstream refining operations—are particularly vulnerable, as they are fully exposed to volatile feedstock costs. Even as product prices have risen, they have not kept pace with the spike in input costs, resulting in compressed spreads. In price-sensitive markets such as India, several producers have reportedly reduced operating rates sharply, as producing at current feedstock costs has become economically unviable.

Downstream impactThe effects of the naphtha shortage extend well beyond petrochemical plants. As the upstream segment struggles, downstream industries are beginning to feel the strain. Shortages or price increases in polymers and intermediates can disrupt manufacturing across sectors such as packaging, consumer goods, automotive, and infrastructure. This, in turn, introduces inflationary pressures into the broader economy, as higher input costs are passed down the value chain. The timing is particularly sensitive, given the already fragile global economic environment marked by slowing growth and persistent inflation concerns.

In response to the crisis, petrochemical producers are increasingly exploring alternative feedstocks such as ethane, propane, and other natural gas liquids (NGLs). However, the transition is neither immediate nor universal. Many existing crackers lack the technical flexibility to process alternative inputs without significant capital investment. Nevertheless, the current disruption is likely to accelerate long-term shifts in feedstock strategies. Companies may prioritize investments in flexible cracking technologies and diversify sourcing to reduce dependence on naphtha.

Changing global competitive landscapeThe shortage is also reshaping the global competitive balance. Producers in the United States and other regions with access to cheaper gas-based feedstocks are gaining a relative advantage, while naphtha-dependent producers in Asia and Europe face rising cost pressures. This divergence could lead to a reconfiguration of global trade flows, with increased exports from cost-advantaged regions and potential rationalization of high-cost capacity elsewhere.

Beyond the immediate crisis, the naphtha shortage highlights deeper structural challenges. As the global energy transition progresses and fuel demand patterns evolve, refinery economics may come under pressure, potentially reducing the availability of naphtha as a byproduct. At the same time, demand for petrochemicals is expected to remain robust, driven by population growth, urbanization, and rising consumption in emerging markets. This creates a paradox: a future where feedstock supply may become increasingly constrained even as demand continues to expand.

Outlook

The ongoing naphtha shortage is more than a transient supply disruption—it is a systemic stress test for the global petrochemical industry. By exposing the sector’s dependence on a single feedstock and its vulnerability to geopolitical and market shocks, the crisis is accelerating a shift toward greater resilience, diversification, and technological adaptation.

In the near term, volatility is likely to persist, with production disruptions, elevated costs, and supply chain uncertainties weighing on industry performance. Over the longer term, however, the lessons from this crisis could drive a more balanced and flexible petrochemical ecosystem—one better equipped to navigate an increasingly complex global energy landscape.

DILIP KUMAR JHA

Editor

dilip.jha@polymerupdate.com