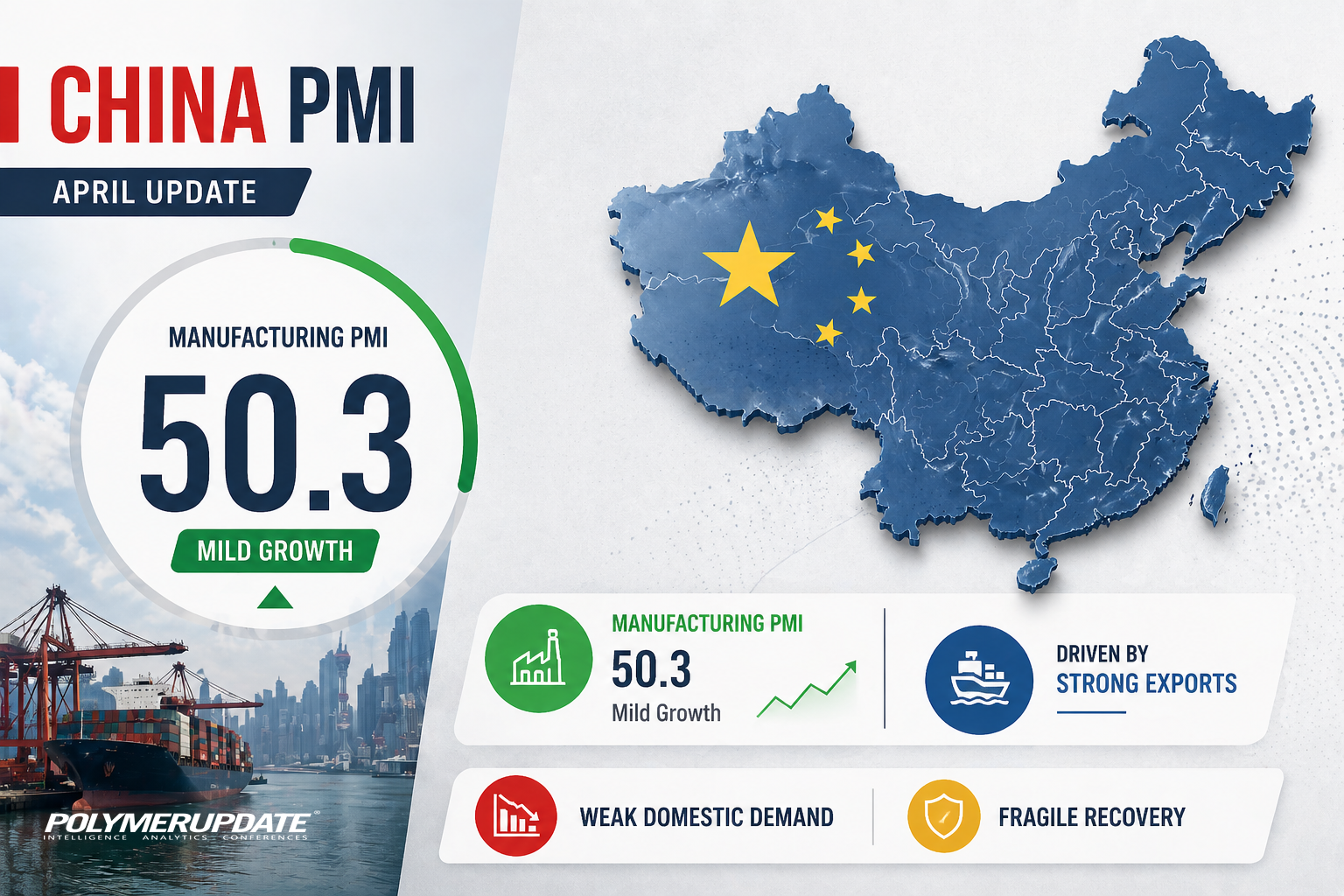

China’s factory activity showed modest improvement in April, with the official manufacturing Purchasing Managers’ Index (PMI) coming in at 50.3, according to data released by the National Bureau of Statistics (NBS) on Wednesday. The reading was slightly above analysts’ expectations of 50.1, indicating a continued, albeit mild, expansion in the manufacturing sector. A PMI reading above 50 signals growth, suggesting that industrial activity is stabilising after recent softness.

The uptick in April was largely driven by sustained expansion in high-tech and equipment manufacturing, reflecting ongoing structural shifts within China’s industrial base. These segments have remained relatively resilient amid broader economic uncertainties, supported by policy measures aimed at boosting advanced manufacturing and innovation. However, the overall pace of growth remains moderate, highlighting the need for continued policy support to strengthen demand and sustain momentum.

Lynn Song, Chief Economist for Greater China at ING Economics, stated, “China’s Purchasing Managers’ Index fared better than expected, as new export orders and imports returned to expansion for the first time since early 2024. However, softer domestic activity pushed the non-manufacturing PMI back into contraction. Price pressures also remained firmly in expansionary territory, suggesting that China’s reflation is continuing.”

Second monthly growth

Second monthly growthApril marked the second consecutive month of expansion, albeit at a slightly softer pace, supported by stronger government spending earlier in the year. Output growth accelerated to its fastest pace in four months, rising to 51.5 from 51.4 in March, indicating continued resilience in production activity. However, momentum in demand showed signs of moderation, with new orders easing to 50.6 from 51.6 in the previous month.

External demand provided some support, as new export orders rebounded to 50.3 in April from 49.1 in March, returning to expansion territory. This improvement suggests a gradual stabilisation in global demand conditions, offering some relief to manufacturers amid ongoing domestic softness. Nonetheless, the overall growth trajectory remained uneven, with the slowdown in new orders highlighting lingering demand-side challenges.

While activity remained in expansionary territory, growth moderated from the previous month’s year-high levels. The composite PMI edged lower to 50.1 in April from 50.5 in March, reflecting the combined impact of softer domestic demand and only modest improvements in external conditions. The data points to a fragile recovery, with sustained policy support likely needed to maintain momentum in the coming months.

Non-manufacturing fallsChina’s official NBS Non-Manufacturing PMI slipped back into contraction territory in April 2026, falling to 49.4 from 50.1 in March and undershooting market expectations of 49.9. The decline signals renewed weakness in the services-led segment of the economy, reversing the modest expansion seen in the previous month. The data suggests that the recovery in domestic activity remains fragile, with momentum proving difficult to sustain.

The slowdown was broad-based across key sub-components. The business activity index declined for both construction, dropping to 48.0 from 49.3 in March, and services, which eased to 49.6 from 50.2. Sentiment weakened across most industries, indicating softer demand conditions, although pockets of resilience were seen in transport and telecom-related services, which continued to perform relatively better than the broader sector.

Demand-side pressures remained evident, with new orders contracting further to 44.3 from 45.0, underscoring subdued domestic demand. While the employment index showed a marginal improvement to 45.5 from 45.2, it remained firmly in contraction territory, pointing to continued labour market softness. Overall, the data highlights persistent headwinds in the non-manufacturing sector, suggesting that stronger policy support may be required to stabilise growth.

“Non-manufacturing PMI data for April was less encouraging, slipping back to 49.4 and matching January’s level, a 40-month low. The new orders sub-index dropped to 44.3, its weakest reading since 2022, highlighting persistent demand weakness. New export orders showed a modest improvement to 47.3, but remained in contraction for the 16th consecutive month. The only positive takeaway was a slight uptick in business expectations, which rose to 54.7 and ended a three-month streak of declines, offering a tentative sign of improving sentiment despite the broader softness in activity,” said an analyst with AnandRathi Investment Services.

Sub-indices’ performanceIn terms of the key sub-indices, production edged up 0.1 percentage point (pp) to 51.5, while employment also moved 0.2pp higher, staying in contraction at 48.8. However, overall new orders dropped quite significantly to 50.6 from 51.6, suggesting weak orders domestically. The more encouraging data points were the new export orders subindex, which rose 1.2pp to 50.3. It returned to expansionary levels for the first time since April 2024, as did the imports subindex, which eked back into expansionary territory at 50.1 for the first time since March 2024. This data suggests that trade activity remained solid in April.

In terms of price pressures, the raw material purchase price index (63.7) and ex-factory prices (55.1) both remained quite elevated, though down slightly from March's levels. This early data suggest that the reflation trend is continuing, likely to be confirmed by the inflation data out on 11 May. The RatingDog manufacturing PMI also beat expectations solidly. It rose to 52.2, up from 50.8. The outperformance of this measure, which samples more export-oriented private firms, suggests that external demand continues to outpace domestic demand.

Moderating input costsInput price pressures moderated in April, with the index easing to 51.7, though it remained in expansionary territory for the sixth consecutive month. This indicates that firms continue to face elevated cost pressures, albeit at a slightly slower pace than before. The persistence of input cost inflation suggests that upstream price dynamics have yet to fully normalise.

However, these cost pressures have not been passed on to consumers. The sales price component remained in contractionary territory for the 31st straight month, coming in at 48.1, highlighting weak pricing power among businesses. This divergence between input costs and output prices points to margin compression, as firms absorb higher costs in an environment of subdued demand.

The trend is particularly evident in China’s services sector, which is more domestically oriented than manufacturing and has begun to underperform in recent months. Softer domestic demand conditions have limited firms’ ability to raise prices, reinforcing disinflationary pressures across the sector. This dynamic underscores the broader challenge facing the economy, where uneven demand recovery continues to weigh on business sentiment and profitability.

DILIP KUMAR JHA

Editor

dilip.jha@polymerupdate.com