This week, HDPE prices quoted unchanged in the Asian region.

An industry source in Asia on condition of anonymity informed a Polymerupdate team member, “International oil prices gained even as global markets remained focused on developments unfolding in the Middle East while the US dollar experienced a decline against other major global currencies.”

The source added, overall market sentiment was steady to soft, with most buyers already having sufficient stock and not in a rush to make new purchases.

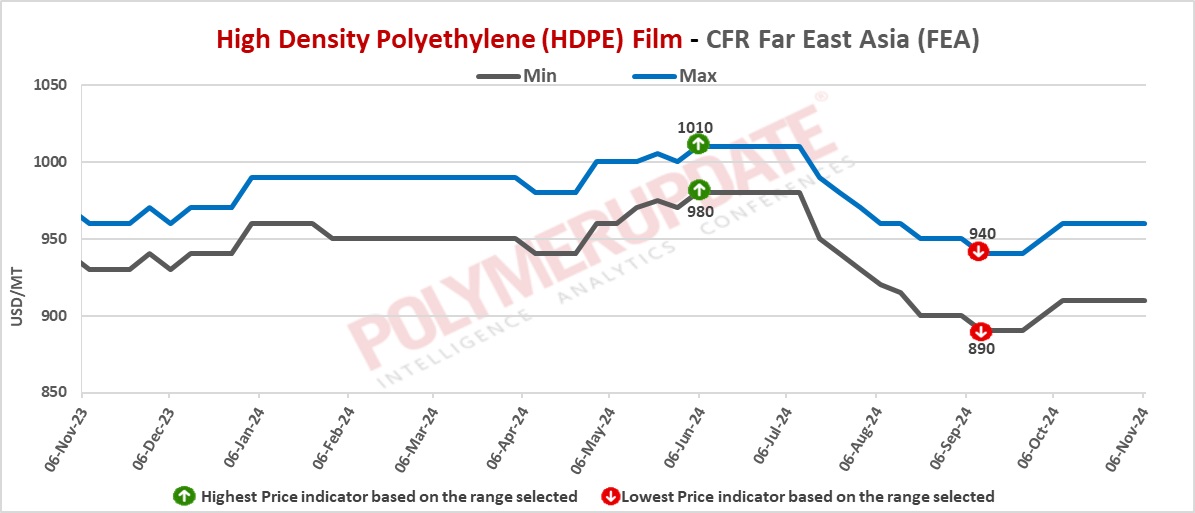

In Far East Asia, HDPE film prices were assessed at the USD 910-960/mt CFR levels, recording a week on week rollover. HDPE blow moulding prices were assessed steady at the USD 890-940/mt CFR levels while HDPE yarn prices were also assessed flat at the USD 920-940/mt CFR levels. HDPE injection prices were assessed at the USD 890-910/mt CFR levels, constant from the previous week.

China’s PE import market activity weakened, even as the yuan currency appreciated. Import buying indications are currently limited, remaining at low levels as converters anticipate new capacity additions expected in the fourth quarter. Additionally, there has been an increase in the import volumes of North American-origin cargoes coinciding with year-end de-stocking efforts.

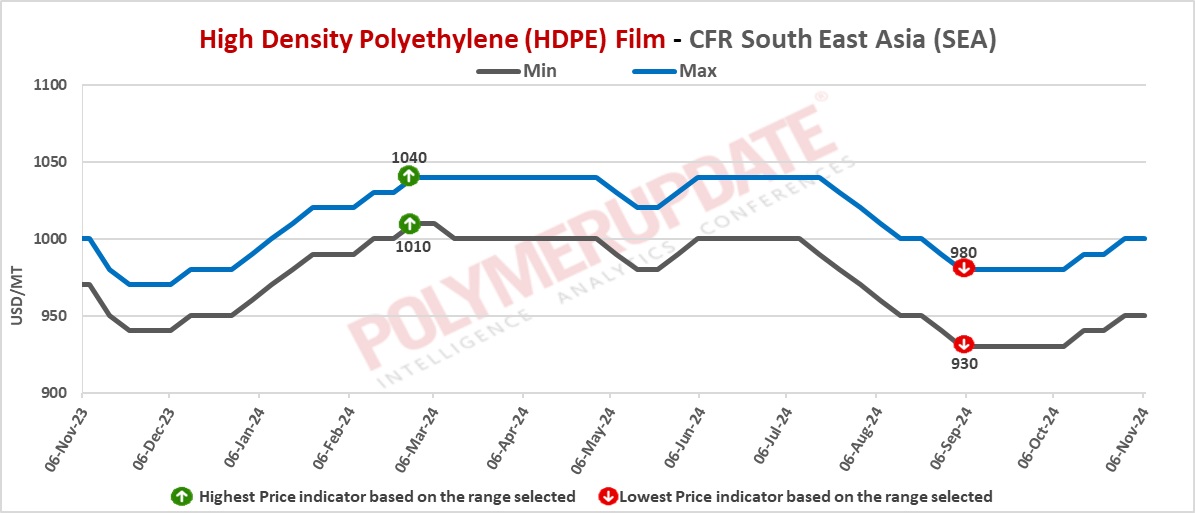

In Southeast Asia, HDPE film prices were assessed at the USD 950-1000/mt CFR levels, steady week on week. HDPE injection prices were assessed flat at the USD 940-990/mt CFR levels. HDPE BM prices were assessed flat at the USD 960-1000/mt CFR levels, and HDPE yarn prices were also stable at the USD 980-1020/mt CFR levels.

In Southeast Asia, selling indication was heard at the USD 950-960/mt levels from the Middle Eastern producers while bidding was happening in between USD 930-940/mt levels. Other Asian producers offered HDPE film grade at the USD 990-1010/mt levels.

It was also heard that buyers are focusing on domestic material rather than import material. The PE (polyethylene) import price assessments were primarily influenced by recent deals and offers in the market. The sentiment surrounding high-density polyethylene (HDPE) has been characterized as weak due to several factors. There is an ample supply of HDPE in the market, which has resulted in competitive offerings from various suppliers. This oversupply and competition are putting downward pressure on prices, leading to a lackluster demand environment and diminishing buyer confidence. As a result, the overall market sentiment for HDPE remains subdued. The arrival of competitively-priced U.S. cargoes, expected by December, has led to a decrease in import prices in Vietnam, especially for HDPE film. This increase in affordable U.S. supplies is putting downward pressure on the market, resulting in lower costs for this material.

In northern Thailand, industrial and commercial activities began improving after the monsoon season. Local converters are optimistic that demand for finished products will rise during the peak travel period in November-December. However, most polyethylene (PE) converters have enough stock to maintain operations until late November.

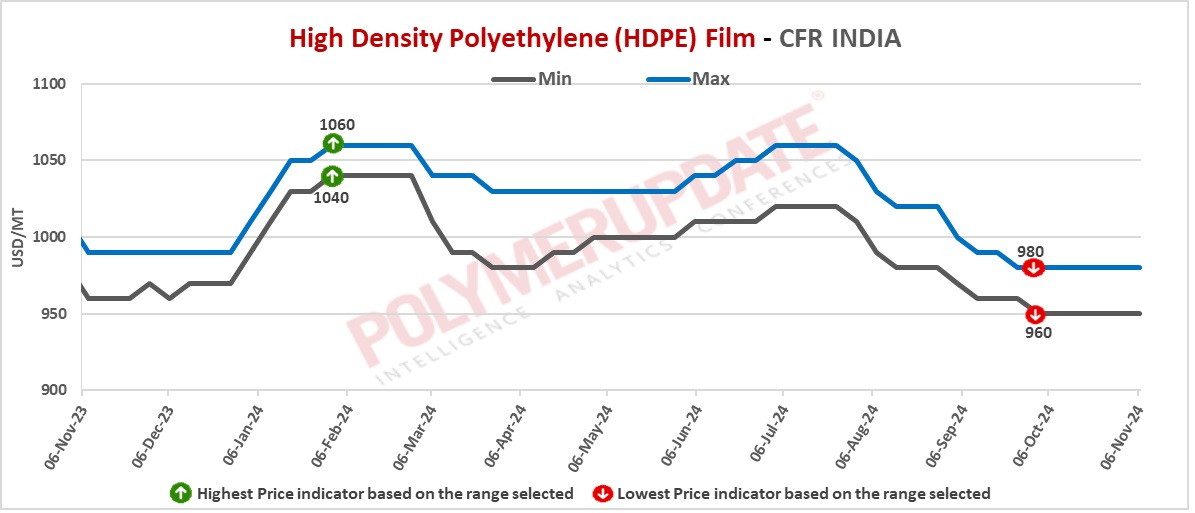

In India, HDPE film prices were assessed at the USD 950-980/mt CFR levels while HDPE BM prices were assessed at the USD 950-970/mt CFR levels, both rolled over from the previous week. HDPE Injection prices were assessed steady at the USD 940-980/mt CFR levels and HDPE yarn prices were also assessed flat at the USD 950-970/mt CFR levels. . An industry source in Asia on condition of anonymity informed a Polymerupdate team member, Reliance Industries Limited rolled over HDPE prices with effect from November 1, 2024.

In India, PE prices were assessed stable as market was quiet due to Diwali festival last week. Buyers are expected to replenish stock as needed, with the assumption that supply will remain adequate for the remainder of the year.

In Pakistan, HDPE yarn grade prices were assessed at the 980-990/mt CFR levels and HDPE injection grade prices were assessed at the USD 970-998/mt CFR levels, both constant from the previous week. HDPE BM grade prices were assessed at the USD 980-1000/mt CFR levels while HDPE film prices were assessed at the USD 980-1000/mt CFR levels, both rolled over week on week. Trader from Middle East was heard offering HDPE film grade below USD 980/mt levels, but there is no official confirmation.

In Sri Lanka, HDPE film prices were assessed flat at the USD 1010-1050/mt CFR levels and HDPE BM prices were assessed stable at the USD 1010-1050/mt CFR levels. HDPE injection grade prices were at the USD 1000-1030/mt CFR levels while HDPE yarn grade prices were also assessed at the USD 1010-1040/mt CFR levels, both unchanged week on week.

In Pakistan and Sri Lanka, overseas producers initially announced higher import offers, but market participants were reluctant to purchase at those price levels due to weak demand. As a result, the overseas suppliers lowered their offers.

In Bangladesh, HDPE BM prices were assessed stable at the USD 1010-1030/mt CFR levels and HDPE film prices were assessed flat at the USD 1010-1030/mt CFR levels. HDPE Injection grade prices were assessed at the USD 1000-1020/mt CFR levels while HDPE yarn prices were assessed at the USD 1000-1020/mt CFR levels, both rolled over from the previous week.

In Bangladesh, overseas suppliers have announced fresh offers, but buyers are reluctant to accept them due to weak demand. Geopolitical issues have further dampened market sentiment in the region.

Feedstock CFR North East Asia prices were assessed at the USD 845-855/mt levels, a gain of USD (+10/mt) week on week. Meanwhile, ethylene CFR South East Asia ethylene prices were assessed stable at the USD 935-945/mt levels.

In plant news, Bora Lyondellbasell Petrochemical has taken off stream its High density polyethylene (HDPE) unit for maintenance around October 30, 2024. Further details on the duration of the shutdown could not be ascertained.” Located in Panjin, Liaoning in China, the unit has production capacity of 350,000 mt/year.