Click the icon to add a specified price to your Dashboard list. This makes it easy to keep track on the prices that matter most to you.

This week, PVC prices witnessed a fall in the Asian region.

An industry source in Asia on condition of anonymity informed a Polymerupdate team member, “A US-brokered ceasefire deal between Ukraine and Russia, having the potential to lay the groundwork for a broader peace plan, exerted a bearish pressure on prices. This development has offset concerns arising from geopolitical tensions in the Middle East.”

The source added, “Lower import offers from a major Taiwanese manufacturer, coupled with lacklustre demand trends, have contributed to a decline in PVC prices across the Asian market. On the cost front, fluctuations in calcium carbide prices, along with variations in the prices of ethylene and vinyl chloride, are critical factors warranting attention. The movement of these raw material prices is intrinsically linked to the production costs of PVC, which subsequently impacts the profitability of the industry. Despite March being a traditionally busy season, the volume of orders from downstream sectors remains suboptimal, resulting in limited market support. Currently, the PVC market continues to experience an imbalance between supply and demand, suggesting a likelihood of further price declines rather than increases.”

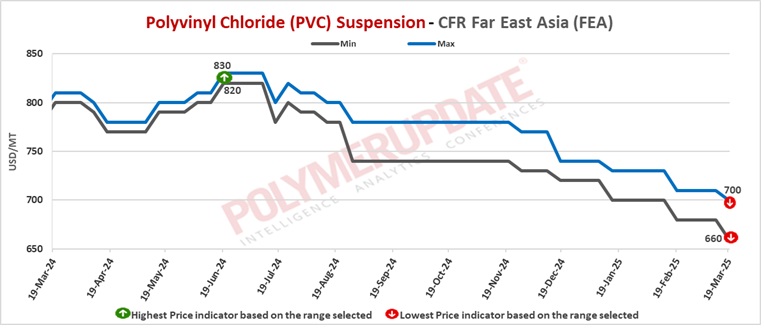

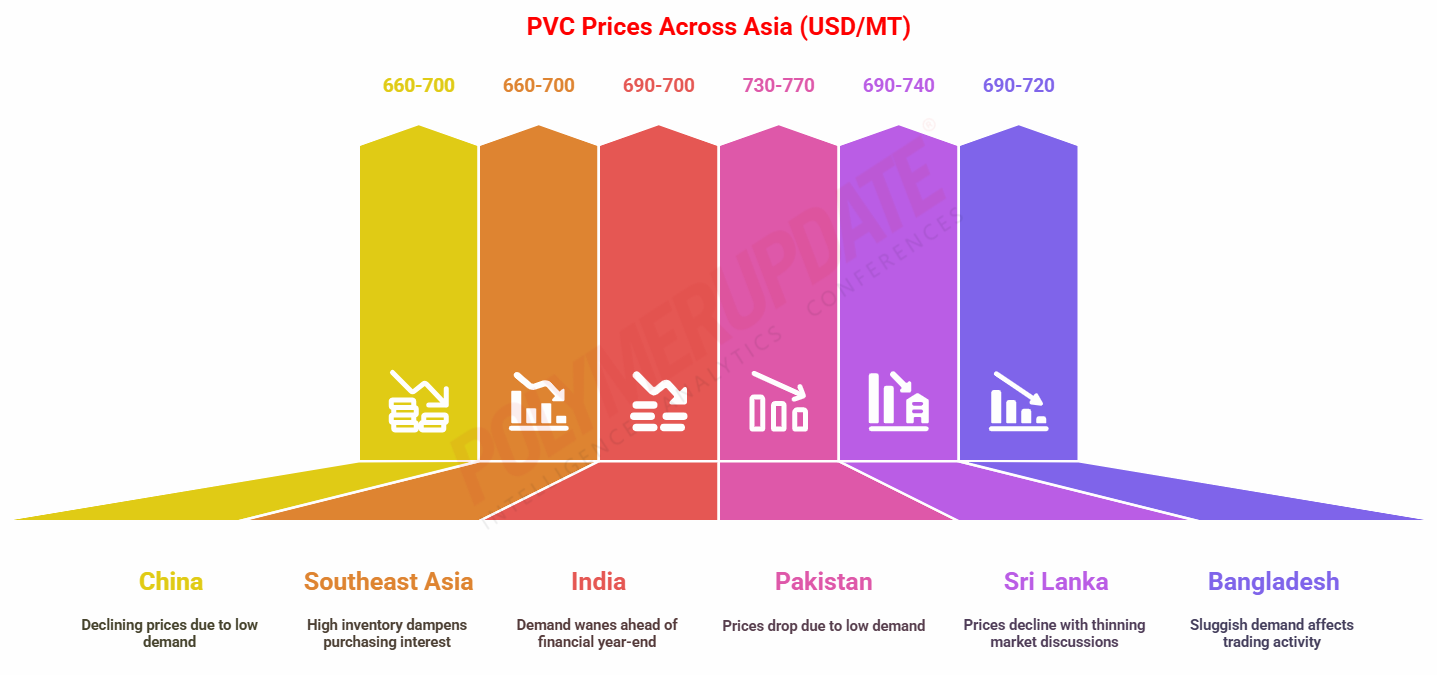

In China, PVC prices were assessed at the USD 660-700/mt CFR levels, a fall of USD (-10/-20/mt) week on week.

In China, Taiwanese producer offers PVC resin suspension grade at the USD 700/mt levels, for shipment in April 2025.

This week, Chinese PVC prices experienced further declines, influenced by decreasing feedstock costs and a lack of buying interest nationwide.

PVC futures continued to drop, reflecting the previous week's losses amid a downturn in related commodities in China, uncertainties regarding potential additional tariffs on finished goods entering the US, and concerns about a possible slowdown in the US economy. Spot PVC transactions in China also diminished, as converters exercised caution regarding overstocking due to the ongoing price declines observed in recent weeks. The domestic supply of PVC remained abundant, with production levels consistently high throughout China.

In the export market, discussions further softened this week, as international buyers reduced their bids for Chinese-origin shipments. Both domestic supply and demand for PVC are exhibiting weak growth rates. Short-term maintenance activities are limited, and cost pressures are hindering the increase in production capacity for PVC manufacturers. Domestic downstream demand is primarily characterized by essential needs, with forward orders showing poor performance. Some companies are taking the opportunity to replenish their stocks at lower prices.

The production and market supply of PVC are anticipated to continue their steady increase. However, the growth rates for both domestic and foreign trade demand have slowed. Domestic terminal purchases are primarily driven by necessity, while a wait-and-see attitude has become more prevalent among international buyers. The overall macroeconomic environment remains weak, and the lacklustre performance of bulk commodities continues to impact market sentiment. Given the pressures of supply and demand, along with subdued macroeconomic expectations, the PVC spot market is likely to experience fluctuations at the lower end.

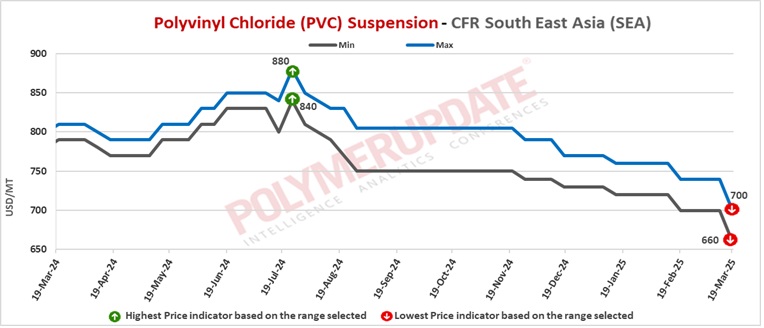

In Southeast Asia, PVC prices were assessed at the USD 660-700/mt CFR levels, a steep drop of USD (-40/mt) from last week.

In Vietnam, a producer from Taiwan offers PVC resin suspension grade at the USD 700/mt levels, for shipment in April 2025. Chinese producer offers PVC resin suspension grade at the USD 660/mt levels, for shipment in April 2025.

Southeast Asian PVC import prices experienced a decline this week, attributed to a surplus of supply in the region and persistently high inventory levels among converters. Ethylene-based PVC from China was generally offered at prices ranging from USD 660-670/ton cfr Vietnam, while carbide-based PVC offers were primarily seen in the range of USD 620-630/ton cfr Vietnam. Freight rates from China to Southeast Asia significantly decreased at the beginning of 2025 and have remained stable thus far in March. However, there are anticipations that renewed buying interest in Southeast Asia, following Ramadan and the Thai New Year, could lead to an increase in container freight rates in the upcoming months.

The supply of PVC in Southeast Asia continues to be ample, driven by favourable operating rates among domestic manufacturers aiming to optimize caustic soda production, alongside a robust import market. The high inventory levels among converters in the region are also dampening any further purchasing interest for PVC, as many have already stocked up sufficiently in preparation for the Holy Month of Ramadan.

Additionally, various public holidays in Southeast Asia are expected to result in certain demand segments becoming inactive later in the second quarter. The commissioning of a regional PVC unit in Thailand is anticipated to be finalized by the second quarter, following some delays. It is still too early to conclude that the initiation of new s-PVC production in Thailand will significantly alter the s-PVC balance, as the producer will also be managing production expansions of chlor-alkali and EDC to support the new facility later in the year.

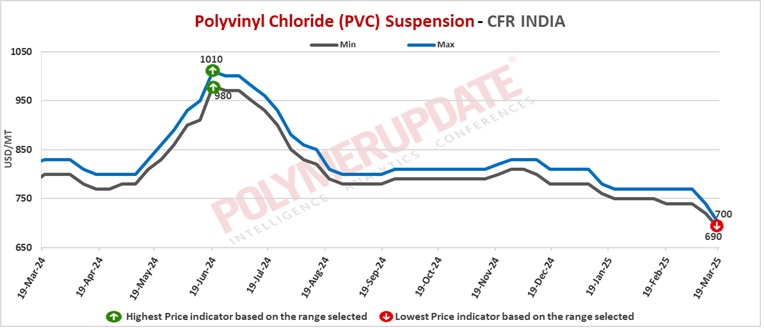

In India, PVC prices were assessed at the USD 690-700/mt CFR levels, a week on week decline of USD (-30/-40/mt).

In India, a major Taiwanese producer is heard to have offered its PVC resin Suspension grades at the USD 700/mt level. These offers are lower by USD 40/mt from the offer made by the producer in the previous month. These offers are for April 2025 shipment on CIF Nhava Sheva/Mundra/Chennai ports basis (LC at Sight).

Indian PVC prices were lower this week, with demand remaining lackluster across the country. Prices also fell as major Taiwanese producer Formosa lowered its offers for April shipments.

The current supply and price levels in India are largely influenced by competitively priced s-PVC shipments from China. However, the demand for these imports is beginning to wane, as many Indian converters are opting to keep their inventories low ahead of financial year-end. They are anticipating further price reductions from China in the near future due to ongoing global macroeconomic uncertainties. Some industry participants have suggested that the final findings of India's investigation into anti-dumping duties (ADDs) on PVC resin may be announced early next week, as the investigation approaches its one-year deadline on March 25, 2025.

Government of India has issued disclosure statement of Anti-dumping investigation into imports of “Polyvinyl Chloride Suspension Resins" originating in or exported from China PR, Indonesia, Japan, Korea RP, Taiwan, Thailand and United States of America - Please click here to download the full PDF file

Meanwhile, demand for carbide-based PVC in India remains subdued in light of forthcoming Bureau of Indian Standards (BIS) quality regulations. Traders have noted that additional interest in these products is being limited by existing stock purchased at higher prices, which has proven difficult to sell in the pipe sector during the first quarter.

The enforcement of BIS quality standards in India is expected to significantly restrict imports of carbide-based s-PVC, as these would surpass the allowable residual vinyl chloride monomer (RVCM) content of 2 parts per million in PVC.

In India, trade discussions regarding paste PVC (e-PVC) have slowed down with converters opting to hold minimal inventories as the financial year draws to a close. The existing anti-dumping duties (ADDs) are also impacting the demand for e-PVC imports, although this effect is primarily felt with specific origins rather than the overall performance of downstream markets. This week, there were few new offers from Asia, as many stakeholders opted to hold off until the next round of proposals before presenting new pricing. Similarly, European e-PVC manufacturers are postponing their new offers, with ongoing reports of rising energy costs in Europe further constraining margins in both the domestic and export markets

Please click on the link to download the PDF file to know the quantum of duties proposed to be levied on e-PVC and s-PVC imports as per the final findings by the Director General of Trade Remedies (DGTR)

In Pakistan, PVC prices were assessed at the USD 730-770/mt CFR levels, down USD (-10/mt) from the previous week.

In Pakistan, overseas producers offered PVC resin suspension grades in the range of USD 730-770/mt levels, for shipment in April 2025.

In Pakistan, prices have continued to decline due to a scarcity of offers and a lack of purchasing interest, influenced by elevated inventory levels and low demand. The stagnation in demand is prevalent nationwide as market players have winded down operations during the Holy Month of Ramadan. Domestic producers have decreased their prices in response to excess stock, which has made local products more competitive and has further slowed down trading activity.

There was minimal buying interest for US-origin cargoes in the market. Buyers have adopted a cautious approach, influenced by the competitive pricing of domestic materials and a seasonal decrease in demand.

In Sri Lanka, PVC prices were assessed at the USD 690-740/mt CFR levels, a week on week decrease of USD (-10/mt). In Sri Lanka, prices edged lower on the back of lower offers and thinning market discussions.

In Sri Lanka, overseas producers offered PVC resin suspension grades in the range of USD 690-740/mt levels, for shipment in April 2025.

In Bangladesh, PVC prices were assessed at the USD 690-720/mt CFR levels, a fall of USD (-10/mt) week on week.

In Bangladesh, a producer from Taiwan offered PVC resin suspension grade at the USD 710-720/mt levels, for shipment in April 2025. A Chinese producer offered PVC resin suspension grade at the USD 680-690/mt levels, for shipment in April 2025.

In Bangladesh, the absence of PVC trading has resulted in a decrease in the weekly price range, as demand continues to be sluggish nationwide due to a lack of new offers. The overall demand remains stagnant as market participants have winded down their activities in observance of the Holy Month of Ramadan.

Feedstock EDC prices were assessed stable at the USD 220-230/mt CFR China level while CFR South East Asia EDC prices were also assessed flat at the USD 230-240/mt levels.

Feedstock CFR South East Asia VCM prices were assessed at the USD 545-555/mt level while CFR China VCM prices were assessed at the USD 520-530/mt levels, both rolled over week on week.

Feedstock ethylene prices on Tuesday were assessed at the USD 850-860/mt CFR North East Asia levels, a fall of USD (-15/mt) from last week. Meanwhile, CFR South East Asia ethylene prices were assessed stable at the USD 915-925/mt levels.

In plant news, Yibin Tianyuan is in plans to undertake a maintenance shutdown at its Polyvinyl chloride (PVC) plant in end March 2025 for maintenance. The plant is expected to remain offline for about one week. Located in Sichuan province, China, the PVC plant has a production capacity of 380,000 mt/year.