Click the icon to add a specified price to your Dashboard list. This makes it easy to keep track on the prices that matter most to you.

This week, Low density polyethylene prices down adjusted in the Asian region.

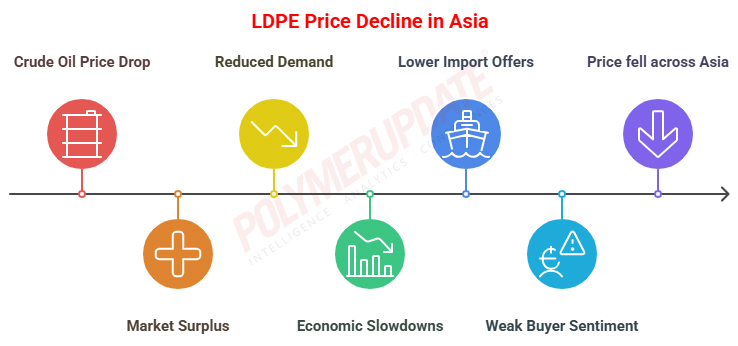

An industry source in Asia, on condition of anonymity, informed a Polymerupdate team member, “Crude oil prices have been on a downward trajectory, primarily due to persistent production pressures from the OPEC+ coalition, which comprises major oil-producing nations dedicated to sustaining high output levels. This surge in supply has led to a market surplus, thereby applying downward pressure on prices. Furthermore, global demand forecasts remain lacklustre, suggesting a prolonged decline in consumption across major economies. Economic slowdowns, inflation worries, and shifts in energy consumption patterns have all played a role in diminishing demand expectations. The interplay of high production levels and reduced demand has led to a continued decline in crude oil prices, highlighting a supply-demand mismatch and ongoing market volatility."

The source added, “The market has also seen a price drop in recent times, largely influenced by two primary factors: a decrease in import offers from foreign suppliers, which has resulted in lower supply availability and potentially reduced competition among sellers, and a weakening buyer sentiment stemming from economic uncertainties and other market issues, culminating in a decline in demand. These elements have collectively contributed to the prevailing downward trend in market prices.”

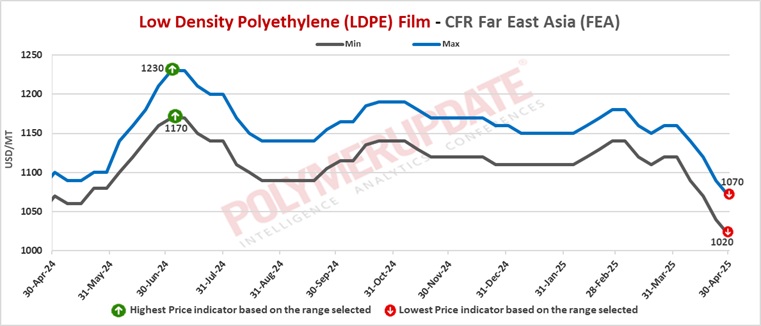

In Far East Asia, LDPE film grade prices were assessed at the USD 1020-1070/mt CFR levels, a drop of USD (-20/mt) from the previous week.

In China, Middle Eastern producers have offered their LDPE film grades in the range of USD 1020-1070/mt levels, for shipment in May 2025.

In China, the polyethylene (PE) import market encountered difficulties due to a further reduction in import margins, which hindered negotiations. While some suppliers independently lowered their offers, buyer interest remained subdued, diminishing China's appeal as a PE export destination. In the US dollar-denominated market, demand for PE was relatively weak, resulting in a decline in quotations. Domestic purchasing capacity was moderate, while the availability of imports gradually improved, applying short-term downward pressure on PE prices.

Overall, US dollar market prices remained stable; however, the narrowing price differential between domestic and international markets has effectively eliminated most import arbitrage opportunities. Market activity has significantly slowed, with participants primarily adopting a wait-and-see approach. Looking forward, attention will shift to changes in supply flows and emerging pricing trends. As the month concludes, market supply remained relatively tight while upstream prices held steady. However, downstream orders experienced a month-on-month decline, and restocking interest was minimal. Amid ongoing supply-demand dynamics, the PE market continued to exhibit fluctuations.

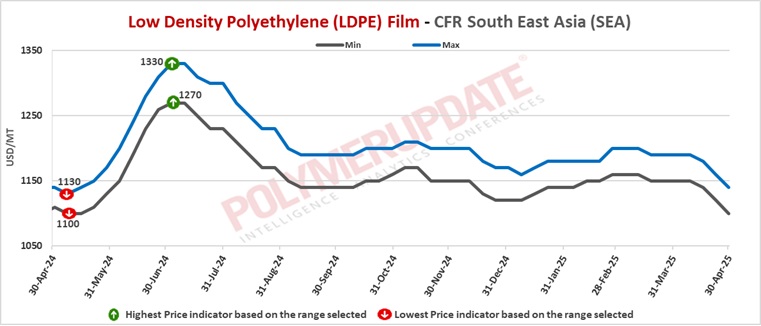

In Southeast Asia, LDPE film grade prices were assessed at the USD 1100-1140/mt CFR levels, lower by USD (-20/mt) week on week.

In Vietnam, Middle Eastern producers have offered their LDPE film grades at the USD 1100-1140/mt levels, for shipment in May 2025. Although selling indications were at the USD 1100/mt levels, buyers were bidding at the USD 1080-1090/mt levels.

In Southeast Asia, Polyethylene (PE) prices have declined amid shifting trade dynamics and market weaknesses. Market sources indicate that US PE shipments originally intended for China have been rerouted to Southeast Asia since last week.

This change, coupled with falling prices in the Chinese market, has intensified regional competition and contributed to a reduction in PE prices. Furthermore, weak demand from downstream sectors and competitive domestic pricing in the region have exacerbated the downward trend.

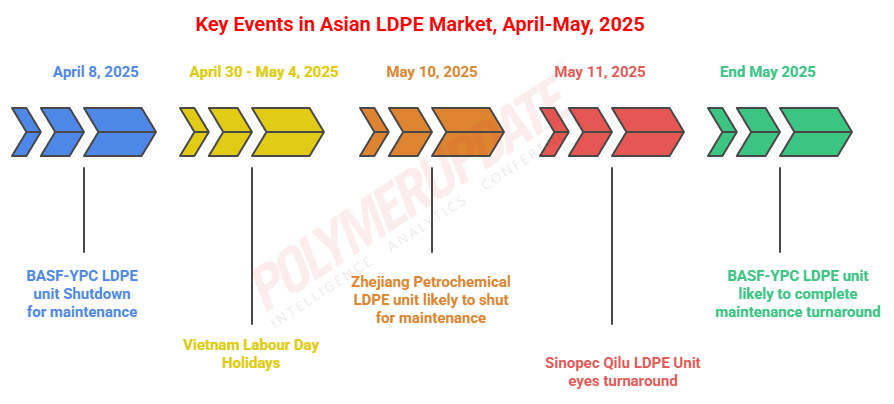

As a result, Middle Eastern suppliers have lowered their May shipment offers to Vietnam by USD 30–80 per tonne compared to the previous month, affecting various grades of PE. This price decrease is associated with the surge of US shipments into Vietnam and inventory pressures stemming from reduced netbacks for exports to China. Trading activity in Vietnam is expected to slow further next week as market participants take note of the Labour Day holidays from April 30 to May 4, 2025.

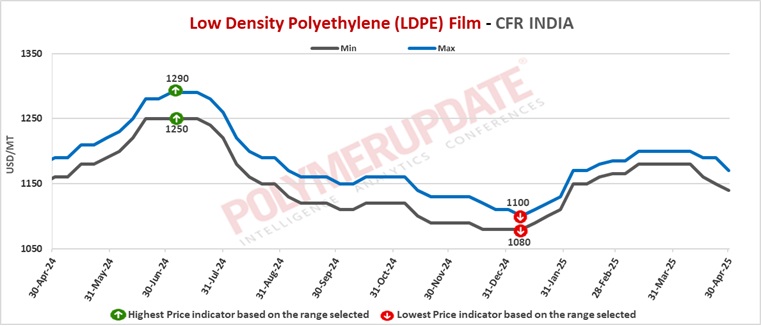

In India, LDPE prices were assessed at the USD 1140-1170/mt CFR levels, a drop of USD (-10/-20/mt) from last week.

In India, Middle Eastern producers have offered their LDPE film grades in the range of USD 1140-1170/mt levels, for shipment in May 2025.

In India, Polyethylene (PE) prices fell amid weak spot demand and a cautious market perspective due to ongoing trade tensions between the US and China. While some offers for May shipments were presented at lower price points, actual transactions were limited and occurred at reduced prices, reflecting a lack of buying interest.

Domestic producers sought to boost sales by offering volume-based incentives; however, overall restocking efforts were feeble, with buyers mainly concentrating on meeting immediate needs rather than increasing inventories. Furthermore, negative market sentiment in China and concerns regarding the potential diversion of US-origin PE supplies are anticipated to further limit short-term price negotiations, leading to the overall vigilant market environment.

In Pakistan, LDPE prices were assessed at the USD 1140-1160/mt CFR levels, week on week declined by USD (-10/-20/mt).

In Pakistan, overseas suppliers have offered their LDPE film grades in the range of USD 1140-1160/mt levels for shipment in May 2025.

In Pakistan, Polyethylene (PE) grade prices have continued to exhibit weakness this week. The main factor contributing to this ongoing decline is the lack of enthusiasm among buyers. This hesitance to engage in purchases is primarily attributed to the current high levels of stock in the market, which have been built up from previous cargo imports over the past few months. Consequently, with adequate inventories available, buyers are less motivated to initiate new purchases, resulting in either stable or decreasing PE prices in the market.

In Sri Lanka, LDPE prices were assessed at the USD 1160-1190/mt CFR levels, a fall of USD (-10/mt) from the previous week.

In Sri Lanka, Middle Eastern producers have offered their LDPE film grades in the range of USD 1160-1190/mt levels for shipment in May 2025.

In Sri Lanka, buyers have displayed minimal enthusiasm for restocking inventory, resulting in a sluggish demand environment. This limited interest in replenishing stock indicates a cautious purchasing approach, likely influenced by factors such as economic uncertainty, elevated inventory levels, or diminished consumer confidence, all of which have contributed to the overall tepid demand sentiment.

In Bangladesh, LDPE prices were assessed at the USD 1120-1140/mt CFR levels, lower by USD (-10/mt) from last week.

In Bangladesh, Middle Eastern producers have offered their LDPE film grades in the range of USD 1130-1150/mt levels for shipment in May 2025.

In Bangladesh, buyer sentiment in the LDPE market remains cautious due to ongoing trade tensions between the United States and China. Many market participants are opting to delay purchases in anticipation of further price declines. The recent decision by the U.S. government to postpone the implementation of additional import tariffs has been welcomed by local converters, offering temporary relief and easing immediate concerns. However, overall market activity continues to be subdued as buyers remain vigilant, monitoring global developments before committing to new purchases.

Feedstock ethylene prices on Tuesday were assessed stable at the USD 785-795/mt CFR North East Asia levels while CFR South East Asia ethylene prices were also assessed flat at the USD 865-875/mt levels.

In plant news, BASF-YPC is in plans to bring on stream its Low density polyethylene (LDPE) unit in end May 2025. The unit was shut for maintenance on April 8, 2025. Located in Nanjing, Jiangsu in China, the unit has a production capacity of 220,000 mt/year.

In other plant news, Zhejiang Petrochemical is planning to shut its LDPE unit from May 10, 2025 for maintenance. The unit is expected to remain offline until June 10, 2025. Located in Zhoushan, Zhejiang in China, the LDPE unit has a production capacity of 400,000 mt/year.

In another plant news, Sinopec Qilu Petrochemical is likely to undertake a planned shutdown at its Low density polyethylene (LDPE) unit on May 11, 2025 for maintenance. The unit is slated to remain offline until end June 2025. Located in Zibo, Shandong in China, the LDPE unit has a production capacity of 140,000 mt/year.