Click the icon to add a specified price to your Dashboard list. This makes it easy to keep track on the prices that matter most to you.

This week, PVC prices gained in the Asian region._prices_rise_in_Asia.png) An industry source in Asia, on condition of anonymity, informed a Polymerupdate team member, "Prices have risen mainly due to a rise in competitive import offers from international suppliers. A major Taiwanese manufacturer has increased its offer prices for the Asian market, citing an increase in freight costs. While heightened costs related to shipping and logistics have contributed to the overall price rise, the augmented import offers indicate the higher expenses encountered by suppliers. As a result, market prices have strengthened due to these supply-side influences, encompassing both the increased offers from abroad and the rising freight expenses.”

An industry source in Asia, on condition of anonymity, informed a Polymerupdate team member, "Prices have risen mainly due to a rise in competitive import offers from international suppliers. A major Taiwanese manufacturer has increased its offer prices for the Asian market, citing an increase in freight costs. While heightened costs related to shipping and logistics have contributed to the overall price rise, the augmented import offers indicate the higher expenses encountered by suppliers. As a result, market prices have strengthened due to these supply-side influences, encompassing both the increased offers from abroad and the rising freight expenses.”

The source added, “Mounting concerns over a potential supply surplus driven by the prospect of a production increase by the OPEC+ alliance in July has exerted a bearish pressure on global oil prices. Meanwhile, prices have also come under pressure with Iran indicating a willingness to scale back its nuclear program in talks with the United States.”

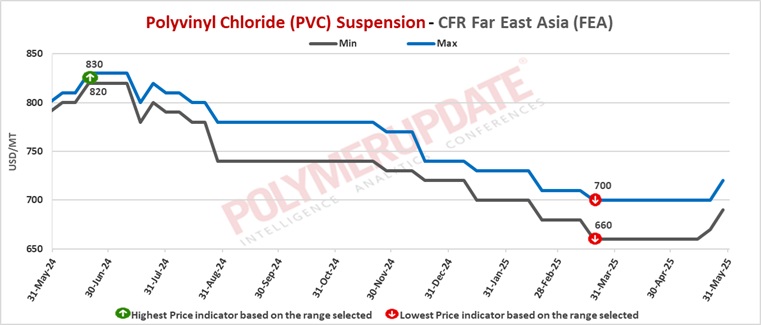

In China, PVC prices were assessed at the USD 690-720/mt CFR levels, an increase of USD (+20/mt) from the previous week.

In China, a Taiwanese producer has offered its PVC resin suspension grades at the USD 710/mt, for shipment in June 2025.

In China, the domestic PVC market saw additional price drops yesterday, driven by low-cost transactions and high volumes, predominantly linked to spot trades, as downstream inventories remain priced low. Concurrently, the pre-sale shipping prices of PVC in Asia for June have risen by USD 10-20 per ton. However, as ocean freight costs are expected to increase, any actual price alterations are likely to be slight.

Additionally, India's import rules have caused exporters to be cautious about shipping PVC to that market. In the short term, industry regulations have little impact, but supply and demand factors remain constrained. This week saw a decrease in the maintenance requirements for PVC plants, and as halted production restarts, supply-side pressure remains. Downstream demand stays weak, offering minimal fundamental support. Overall, it is expected that PVC spot market prices will continue to face persistent downward pressure in the near future.

China's PVC prices rose this week in spite of declining PVC futures, mirroring comparable drops in crude oil futures. The declines in PVC futures this week were less noticeable than the drops seen earlier last week. Domestic market trading activity was constrained this week, as converters opted to sell their current finished goods to the US ahead of the conclusion of the 90-day exemption on reciprocal tariffs. PVC restocking among converters continued to be restricted due to a decline in new orders for finished goods, while the impending new PVC capacities set for June and the third quarter are further dampening demand for spot cargoes. Market participants have noted that container shipping companies are rerouting ships from different trade lanes to focus on transporting as many containers as they can from the US to China, following the recent tariff adjustment between the nations. This has impacted the costs of container shipping, especially between China and India

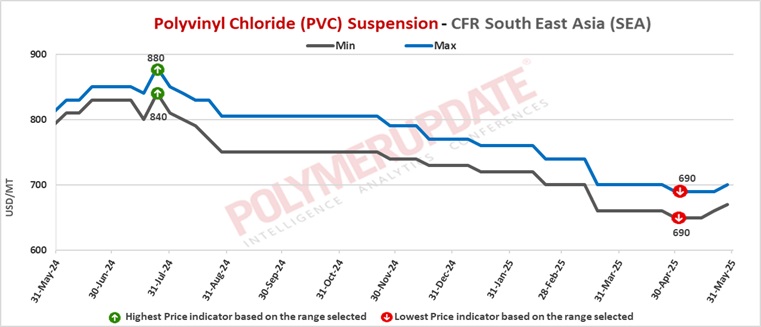

In Southeast Asia, PVC prices were assessed at the USD 670-700/mt CFR levels, a week on week gain of USD (+10/mt).

In Southeast Asia, a producer from Taiwan has offered its PVC resin suspension grade at the USD 740/mt, for shipment in June 2025.

In Vietnam, a producer from Indonesia has offered its PVC resin suspension grade at the USD 670-680/mt for shipment in June 2025. A producer from Thailand has offered its PVC resin suspension grade at the USD 670-675/mt, for shipment in June 2025.

This week, PVC prices in Southeast Asia increased, in spite of consistently sufficient supply from China and slow demand growth throughout the region. Higher import offers into Southeast Asia were primarily evident from a major Taiwanese producer.

Certain converters in Malaysia reported a decline in price offers for Chinese ethylene-based PVC, but transactions had not yet been finalized due to reduced demand for additional cargo. Demand in Southeast Asia continues to be significantly low during May, with participants observing a prolonged supply equilibrium both within the region and worldwide. The commencement of new PVC capacities in China starting in June, along with the postponed initiation of a PVC unit in Thailand in the third quarter, is creating heightened expectations for a prolonged supply balance in the latter half of 2025, with prices anticipated to mirror any possible changes in freight costs or export prices from China due to reduced short-term demand growth expectations in Southeast Asia.

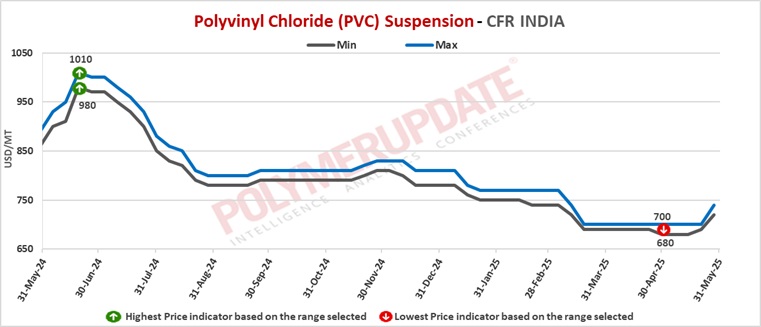

In India, PVC prices were assessed at the USD 720-740/mt CFR levels, higher by USD (+30/+40/mt) from last week. A domestic industry source informed a Polymerupdate team member, “Reliance Industries Limited has raised PVC prices by Re.1/kg basic, with effect from May 24, 2025.”

In India, A major Taiwanese producer has offered its PVC suspension grades (S65D/S65/S60/S70) at the USD 720/mt while (S57) grade is on offer at the USD 730/mt and (B57) grade has been offered at the USD 740/mt levels. These offers are on CIF Nhava Sheva/Mundra/Chennai port basis with shipment for June-July 2025 (LC at sight). These offers are higher by USD 20/mt from previous month offers. Add USD 30/mt for CIF Pipavav port. For LC 90 days (Add USD 10/mt).

Another producer from Taiwan has offered its PVC resin suspension grade at the USD 720/mt (for quantity less than 500 mt) and USD 730/mt (for quantity more than 500 mt) for shipment in June 2025 (LC at sight).

South Korean producers have offered their PVC resin suspension grades in the range of USD 740-760/mt, for shipment in June 2025. A producer from Thailand has offered its PVC resin suspension grade at the USD 740/mt for shipment in June 2025. This price is exclusive of duty.

Meanwhile, a Chinese producer has offered its PVC (ethylene-based) grade at the USD 680/mt CFR levels, for shipment in June 2025.

In India, PVC prices increased slightly due to stronger June-shipment offers, bolstered by higher shipping expenses. Freight rates from China to India increased over the week, and stakeholders expect additional hikes as Chinese exporters rush to send outbound shipments to the US during the initial phase of the 90-day tariff break.

Shipping expenses from China to India have risen this week because of a surge in demand from Chinese exporters keen to ship goods to the US during the initial stages of the 90-day tariff break. Yet, market activity remains subdued, with many suppliers hesitant to finalize offers for June shipments due to uncertainty about the degree of freight cost increases.

Reports indicate that multiple carbide-based PVC shipments from China to India were cancelled last week, heightening buyer reluctance regarding new orders for Chinese deliveries. In terms of demand, PVC consumption is anticipated to decrease shortly due to the influence of the monsoon season on downstream construction and agricultural activities. Amid ongoing market uncertainties, a recent Supreme Court ruling is likely to accelerate the release of final anti-dumping duty outcomes, potentially significantly influencing trade dynamics and pricing in the near future.

Concerns are mounting about the impending Bureau of Indian Standards (BIS) certification deadline scheduled for June 24. Expected challenges in obtaining clearance related to this requirement are probably going to reduce interest in products from China, especially since numerous suppliers still do not have the necessary certification. However, the significant impact on prompt demand still mirrors the postponed ADD announcements regarding s-PVC imports into India, as local authorities now have until the end of June, or 15 months after the start of the investigation, to present final ADD conclusions.

BIS quality regulations are anticipated to be implemented in India on June 24, which will subsequently affect the availability of both s-PVC and e-PVC. Most northeast Asian, excluding China, and southeast Asian s-PVC manufacturers are presently BIS certified, indicating that nearly 40% of the annual import supply to India, as of 2024, may be eliminated from the market if BIS quality regulations are not prolonged and Chinese s-PVC manufacturers are not authorized promptly.

In Pakistan, PVC prices were assessed stable at the USD 710-750/mt CFR levels.

In Pakistan, overseas producers have offered PVC resin suspension grades in the range of USD 710-750/mt, for shipment in June 2025.

In Pakistan, the prices for PVC imports have stayed stable throughout the week, showing an absence of significant price changes. This stability arises from restricted market involvement and minimal demand across the country. Currently, the total PVC inventory in Pakistan is adequate, primarily due to previous import shipments of PVC from China that have increased the existing stock. The interaction of stable prices, low demand, and sufficient inventories suggests a cautious market environment with no immediate requirement for price changes or increased buying activity.

In Sri Lanka, PVC prices were assessed at the USD 700-750/mt CFR levels, a rise of USD (+20/mt) from the previous week.

In Sri Lanka, a Chinese producer has offered its PVC resin suspension grade at the USD 700/mt, for shipment in June 2025. A producer from Taiwan has offered its PVC resin suspension grade at the USD 750/mt, for shipment in June 2025.

In Sri Lanka, the prices of PVC have seen an increase. This rise is mainly influenced by higher offers from producers. In spite of this price increase, the general demand outlook in the market continues to be weak. Buyers are hesitant to buy at elevated prices, and are refraining due to economic doubts, or are facing a decrease in buying activity. The interplay of increasing producer pricing and weakened demand indicates a situation where supply-side influences are driving prices higher, yet market engagement and buying interest remain low, possibly constraining the overall growth or stability of PVC prices in Sri Lanka

In Bangladesh, PVC prices were assessed at the USD 720-750/mt CFR levels, an increase of USD (+30/mt from last week.

In Bangladesh, a Taiwanese producer has offered their PVC resin suspension grades in the range of USD 720-740/mt, for shipment in June 2025.

Chinese producer has offered its PVC (ethylene-based) grade at the USD 695/mt CFR levels, for shipment in June 2025. Meanwhile, carbide-based PVC grade has been on offer at the USD 670/mt CFR levels.

In Bangladesh, PVC prices maintained an upward trajectory. Meanwhile, import activity for PVC remained subdued throughout the week, indicating limited purchasing or trading activity. Despite the low volume of imports, This price increase were primarily driven by new price offers from suppliers in Taiwan, which appeared bullish.

PVC prices continued to rise. Import activity for PVC continued to be low all week, suggesting restricted buying or trading activity. Even with limited import volumes, this price hike was mainly influenced by seemingly bullish price offers from suppliers in Taiwan.

Feedstock EDC prices were assessed at the USD 155-165/mt CFR China level while CFR South East Asia EDC prices were assessed at the USD 160-170/mt levels, both rolled over week on week.

Feedstock CFR South East Asia VCM prices were assessed at the USD 570-580/mt level, a week on week rise of USD (+10/mt). CFR China VCM prices were assessed at the USD 520-530/mt levels, a fall of USD (-15/mt) from last week.

Feedstock ethylene prices on Tuesday were assessed flat at the USD 775-785/mt CFR North East Asia levels. Meanwhile, CFR South East Asia ethylene prices were assessed at the USD 845-855/mt levels, a week on week decline of USD (-20/mt).

In plant news, Shanxi Huojiagou has taken off stream its Polyvinyl chloride (PVC) plant on May 20, 2025 for a maintenance turnaround. The plant is slated to remain offline until May 30, 2025. Located in Shanxi province, China, the PVC plant has a production capacity of 60,000 mt/year.

In other plant news, Xinjiang Yihua has shut down its Polyvinyl chloride (PVC) plant on May 20, 2025. The plant was slated to remain offline for about 7 days. Located in Xinjiang, China, the PVC plant has a production capacity of 300,000 mt/year.