Click the icon to add a specified price to your Dashboard list. This makes it easy to keep track on the prices that matter most to you.

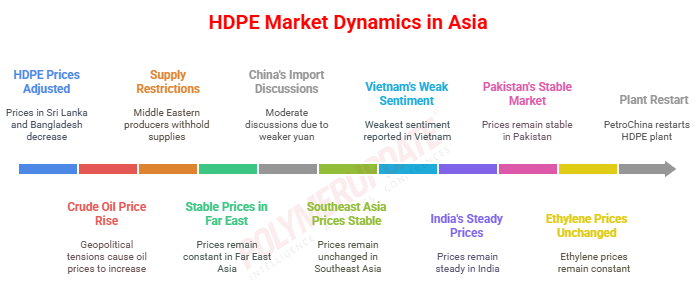

This week, HDPE prices down adjusted in Sri Lanka and Bangladesh while quoting flat in other parts of the Asian region. An industry source in Asia, on condition of anonymity, informed a Polymerupdate team member, “Crude oil prices experienced a significant rise amid ongoing geopolitical tensions and disruptions in supply, reflecting concerns over global economic stability and energy security. The escalation of conflicts and production setbacks have heightened uncertainty in the market, underscoring the delicate balance between geopolitical developments and energy supply dynamics."

An industry source in Asia, on condition of anonymity, informed a Polymerupdate team member, “Crude oil prices experienced a significant rise amid ongoing geopolitical tensions and disruptions in supply, reflecting concerns over global economic stability and energy security. The escalation of conflicts and production setbacks have heightened uncertainty in the market, underscoring the delicate balance between geopolitical developments and energy supply dynamics."

The source added, “Offers remained largely restricted as certain producers, particularly in the Middle East, withheld their supplies due to worries about reduced profitability, unpredictability about market trends leading up to the Eid al-Adha festival, and the necessity to keep track of freight expenses.”

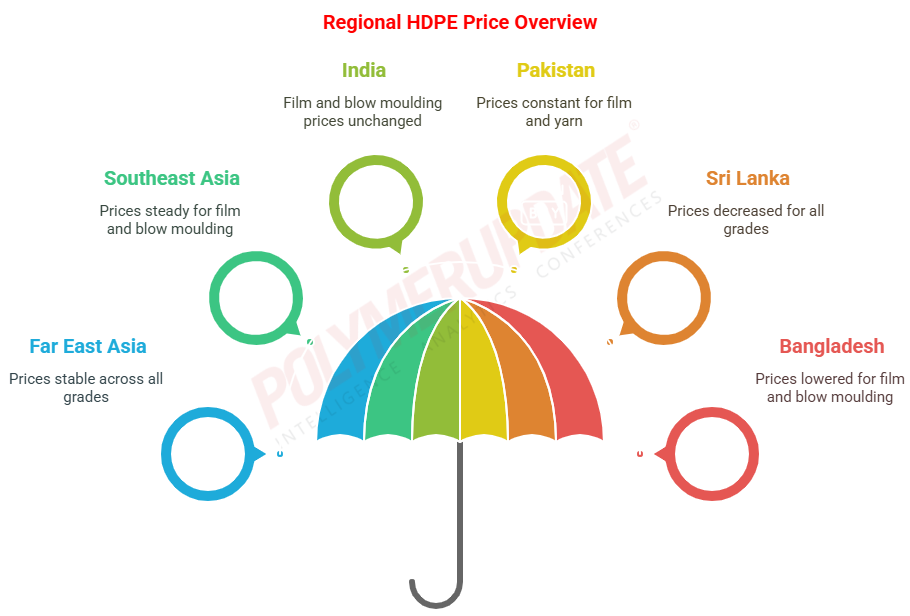

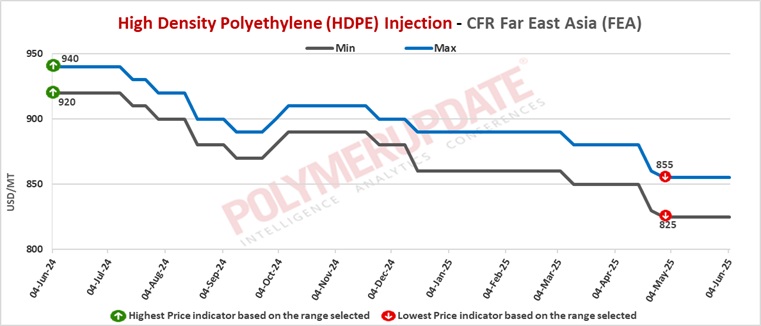

In Far East Asia, HDPE film prices were assessed at the USD 840-900/mt CFR levels, rolled over from the previous week. HDPE blow moulding prices were assessed flat at the USD 835-895/mt CFR levels. HDPE injection prices were assessed at the USD 825-855/mt CFR levels, and HDPE yarn prices were assessed at the USD 875-895/mt CFR levels, both constant week on week.

In China, a Saudi Arabian producer has offered its HDPE film grade at the USD 910/mt CFR levels, for shipment in June 2025. An overseas supplier has offered its HDPE film grade at the USD 850/mt CFR levels, for shipment in June 2025.

In China, discussions about the domestic polyethylene (PE) import prices typically showed a more moderate and subdued tone. This change was mainly caused by a reduction in import arbitrage margins. The decrease in these margins was mainly due to weaker domestic yuan prices in China, which diminished the overall profitability and appeal of importing PE into the nation. Consequently, purchase interest dampened among importers and traders, resulting in a cautious stance during negotiations.

Few international sellers reacted to the subdued market environment by reducing their prices for Chinese buyers to encourage sales. Even with these price cuts, numerous sellers encountered difficulties in finalizing actual transactions, as traders and buyers stayed cautious. This reluctance was additionally complicated by the presence of US-origin shipments being offered at very competitive prices for loading periods in June and July. The competitive pricing of these US-origin shipments made it increasingly challenging for sellers from different regions to obtain firm commitments from Chinese purchasers, adding to the overall softening and wary environment in the PE import market throughout the week.

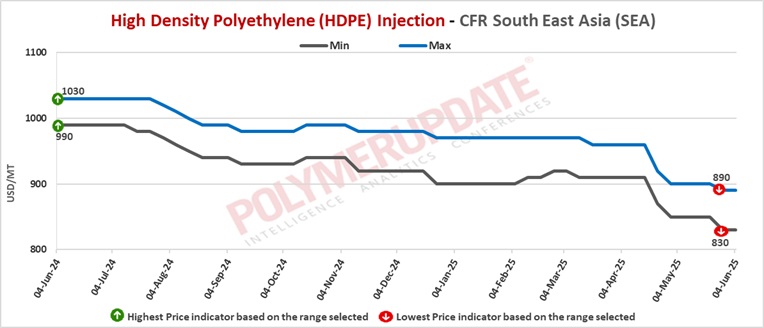

In Southeast Asia, HDPE film prices were assessed at the USD 870-930/mt CFR levels while HDPE blow moulding grade prices were assessed at the USD 840-880/mt CFR levels, both stable from the previous week. HDPE injection prices were assessed flat at the USD 830-890/mt CFR levels. HDPE yarn prices were assessed at the USD 910-950/mt CFR levels, unchanged week on week.

In Vietnam, a Middle Eastern producer has offered its HDPE film grade at the USD 870-880/mt CFR levels, for shipment in June 2025. A producer from Saudi Arabia has offered its HDPE film grade at the USD 870/mt CFR levels, for shipment in June 2025.

In Southeast Asia, Offers for PE supplies from the Middle East remained mostly stable during the week, yet sellers encountered challenges in increasing transaction volumes. Instability in PE prices along with a lacklustre demand forecast caused buyers to be wary while restocking, while opting for local or regional import resources due to shorter delivery times.

A few foreign sellers decreased their offers to buyers in China but found it difficult to finalize firm deals, as some traders offered US-sourced shipments for June-July loading at highly attractive prices. In the PE import market of southeast Asia, there were sporadic conversations about some newly available Middle Eastern products, with the majority of transactions later finalized within the assessment ranges. The unexpected developments regarding the US strategy to impose tariffs globally kept creating uncertainty in the market, particularly for economies like Vietnam and China who are facing elevated tariff rates.

Furthermore, participants in the Southeast Asian market were vigilant for updates regarding the reopening of significant production sites in the region, as discussions suggested that such events might occur in the following weeks and months. In Vietnam this week, HDPE sentiment remained the weakest, as numerous suppliers reported a lack of purchasing interest for any of their announced offers.

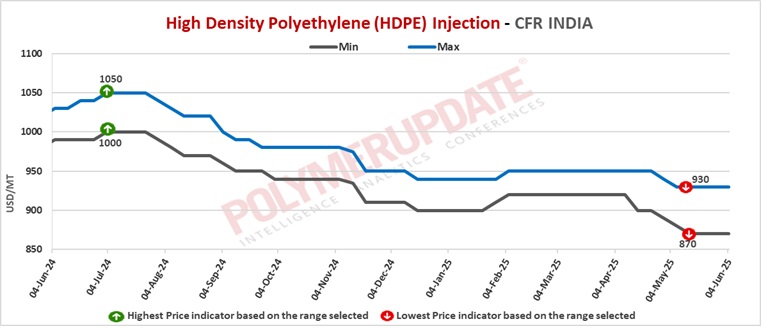

In India, HDPE film prices were assessed at the USD 880-920/mt CFR levels and HDPE blow moulding prices were assessed at the USD 880-910/mt CFR levels, both steady week on week. HDPE yarn prices were assessed at the USD 870-910/mt CFR levels and HDPE Injection prices were assessed at the USD 870-930/mt CFR levels, both rolled over from the previous week.

A domestic industry source informed a Polymerupdate team member, “Reliance Industries Limited has rolled over HDPE grade prices, with effect from June 1, 2025.”

In India, a Middle Eastern producer has offered its HDPE film grade at the USD 920/mt CFR levels, for shipment in June 2025. A Saudi Arabian producer has offered its HDPE film grade at the USD 890-940/mt CFR levels, for shipment in June 2025.

In India, PE prices generally held steady throughout the week due to a scarcity of new spot offers in the market for June shipment material. Domestic supply is expected to rise as a key producer intends to restart operations in early June. This enhanced availability, along with a usual decrease in demand post-summer for items like shrink films and packaging materials utilized in the food and beverage sector, is expected to lessen the appeal of imports soon. Moreover, certain industry players indicated that converter stocks remain low, potentially prompting some short-term replenishment efforts.

Demand is likely to be dampened even more during the monsoon season in India, as infrastructure projects may be halted during spells of heavy rainfall, leading to a slowdown in the issue of new tenders and cautious market engagement by participants. This temporary decline may affect the overall economic progress in segments dependent on infrastructure growth.

In Pakistan, HDPE film prices were assessed at the USD 920-940/mt CFR levels, constant from last week. HDPE yarn grade prices were assessed at the 930-950/mt CFR levels and HDPE injection grade prices were assessed at the USD 920-940/mt CFR level, both steady week on week. HDPE blow moulding grade prices were assessed stable at the USD 930-950/mt CFR levels.

In Pakistan, a Middle Eastern producer has offered its HDPE film grade at the USD 920/mt CFR levels, for shipment in June 2025. A Saudi Arabian producer has offered its HDPE film grade at the USD 940/mt CFR levels, for shipment in June 2025.

In Sri Lanka, HDPE film prices were assessed at the USD 960-990/mt CFR levels and HDPE blow moulding prices were assessed at the USD 960-990/mt CFR levels, both down adjusted by USD (-10/mt) from the previous week. HDPE injection grade prices were assessed at the USD 960-980/mt CFR levels while HDPE yarn grade prices were assessed at the USD 970-990/mt CFR levels, both week on week declined by USD (-10/mt). Muted trading activity continued to weigh negatively on prices.

In Sri Lanka, a Middle Eastern producer has offered its HDPE film grade at the USD 970/mt CFR levels, for shipment in June 2025. A Saudi Arabian producer has offered its HDPE film grade at the USD 1000/mt CFR levels, for shipment in June 2025.

In Bangladesh, HDPE blow moulding prices were assessed at the USD 960-990/mt CFR levels, while HDPE film prices were assessed at the USD 950-980/mt CFR levels, both lower by USD (-10/-20/mt) from the previous week. HDPE Injection grade prices were assessed at the USD 970-990/mt CFR levels and HDPE yarn prices were assessed at the USD 970-990/mt CFR levels, both week on week decreased by USD (-10/mt).

In Bangladesh, a Middle Eastern producer has offered its HDPE film grade at the USD 980/mt CFR levels, for shipment in June 2025. A Saudi Arabian producer has offered its HDPE film grade at the USD 1000/mt CFR levels, for shipment in June 2025.

In the Pakistan and Bangladesh market, buyers expressed reluctance in committing to a few fresh offers that surfaced from Middle Eastern suppliers towards the end of the week. Since buyers were hesitant to make major purchasing decisions at that moment, they opted to delay their commitments until after the Eid al-Adha festival and the Hajj pilgrimage period. This cautious stance was probably prompted by the timing of these religious occasions, which frequently cause changes in market activity, consumer expenditure, and buyer preferences, leading buyers to postpone significant purchases until the celebrations and religious observances are over. Traders and converters have voiced concerns regarding the negative impact that an early monsoon season may have on activities in the South Asian region.

Feedstock ethylene prices on Tuesday were assessed at the USD 845-855/mt CFR South East Asia levels while CFR North East Asia ethylene prices were assessed at the USD 775-785/mt levels, both unchanged from the previous week.

In plant news, PetroChina Lanzhou Petrochemical Yulin Chemical has restarted its High density polyethylene (HDPE) plant in end May 2025 following a turnaround. The plant was shut for maintenance on May 10, 2025. Located in Yulin, China, the HDPE plant has a production capacity of 400,000 mt/year.