Click the icon to add a specified price to your Dashboard list. This makes it easy to keep track on the prices that matter most to you.

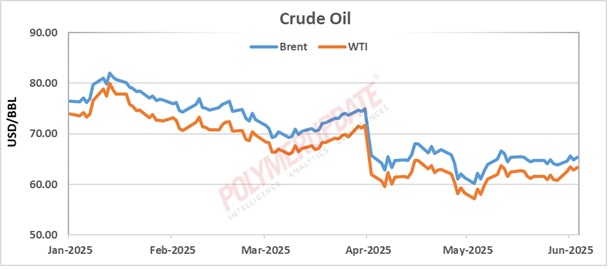

Crude oil prices settled higher last week, marking the first weekly gain in three weeks, driven by optimism surrounding the normalization of trade talks between the United States and China, along with favourable US job data. Energy prices were further supported by geopolitical conflicts, including US-Iran tensions and the Russia-Ukraine war, which kept risk premiums elevated. However, gains were capped by easing supply concerns from Canada’s wildfires and projections of oversupply, as OPEC+ (Organization of the Petroleum Exporting Countries and its allies) decided to continue raising output for the third consecutive month in July.

According to Polymerupdate Research, benchmark Brent crude futures for near-month delivery on the InterContinental Exchange (ICE) began the week at US$ 63.90 a barrel, climbing approximately US$ 1 a barrel for two consecutive days to reach US$ 65.63 a barrel on Tuesday. However, profit-taking midweek pulled prices down to US$ 64.86 a barrel on Wednesday. The trend reversed on Thursday as short-covering lifted prices to US$ 65.34 a barrel, followed by further gains to close the week at US$ 66.47 on Friday. Brent crude futures posted a weekly gain of over 4 percent, or US$ 2.57 a barrel.

Similarly, West Texas Intermediate (WTI) Cushing futures for near-month delivery on the New York Mercantile Exchange (Nymex) started the week at US$ 60.79 a barrel. Prices rose by approximately US$ 1 a barrel on both Monday and Tuesday, reaching US$ 62.85 a barrel on Wednesday. Despite a dip due to profit-taking, WTI futures rebounded, gaining about US$ 1 a barrel on Thursday and Friday to close the week at US$ 64.58 a barrel. This represented a weekly gain of 6.23 percent, or US$ 3.79 a barrel.

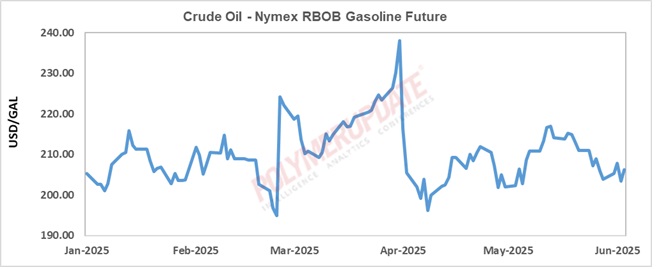

An analyst from Reliance Securities Ltd commented: “Crude oil and gasoline prices settled higher last week, buoyed by robust global economic data supporting energy demand. The US May payroll report released on Friday exceeded expectations, while the Eurozone's January-March 2025 gross domestic product (GDP) was revised upwards. Additionally, easing US-China trade tensions is expected to bolster global economic activity and, consequently, crude oil prices. Crude prices also extended gains on Friday after a Baker Hughes report showed active US oil rigs for the week ending June 6 had fallen to a three-and-a-half-year low. However, a stronger dollar limited the upside in crude prices.” US-China trade talks

US-China trade talks

The strained US-China trade relations appear to be easing following a 90-minute talk between US President Donald Trump and Chinese President Xi Jinping. Both leaders agreed to resume negotiations, with government-level discussions expected to begin shortly. The Trump-Xi conversation is anticipated to improve economic ties between the world’s two largest economies. Previously, both nations had imposed record-high tariffs on each other, with the United States levying duties of up to 145 percent on Chinese goods and Beijing responding with tariffs of up to 125 percent on American products. Trump’s call sought to resolve an impasse stemming from differing interpretations of agreements made during the May talks in Geneva.

Meanwhile, China's export growth slowed to 4.8 percent year-on-year (yoy) in May, down from 8.1 percent yoy in April. The data came in slightly below market forecasts, bringing year-to-date export growth to 6 percent yoy. Exports to the US unexpectedly decelerated despite a temporary reprieve in the trade war, declining by 34.5 percent yoy in May to US$ 28.8 billion, compared to a 21 percent yoy decline in April.

The slower export growth in May likely reflects the lingering impact of peak tariff periods. ING Economics expects US-bound exports to recover in the coming months. Exports to other regions continued to show strong growth during the same period. Shipments to ASEAN countries rose by 14.8 percent, while exports to the EU grew by 12 percent, demonstrating solid performance.

On a net basis, China's trade balance once again exceeded forecasts, rising to US$ 103.2 billion in May, the highest level in four months. Year-to-date, China's trade surplus stands at US$ 471.9 billion, reflecting a yoy increase of US$ 135.6 billion, or 40.3 percent.

Slowdown in US job market

Data compiled by the Bureau of Labour Statistics showed that the long-resilient US labour market softened slightly, adding 139,000 jobs in May—a decline from the higher-than-expected 147,000 jobs created in April. The unemployment rate remained steady at 4.2 percent, and wage growth continued to outpace inflation. Economists had forecast the US economy to add 130,000 jobs in May, with the unemployment rate holding at 4.2 percent. The actual job creation suggests that the US labour market is beginning to cool.

Meanwhile, job gains recorded in March and April were revised downward by a combined 95,000, bringing the average monthly job growth this year to approximately 124,000. This figure remains above the 100,000 threshold, which typically signals a healthy labour market. Falling below the 100,000 threshold could indicate a slowdown, aside from periods of recession. However, the current gains represent the lowest January-May period increase in the past 30 years.

Key tailwinds

US crude oil stockpiles, currently at 430 million barrels, are 7 percent below the five-year average, reflecting tight market conditions. Inventories declined for the second consecutive week ending May 30, 2025, approaching the lower end of the five-year range. Adding to this is robust global demand during the summer driving season, which could act as a key driver for near-term market balances and sentiment despite broader weaknesses in the market.

On May 30, 2025, the OPEC+ coalition announced a headline supply increase of 411,000 barrels per day (bpd) for July. However, the actual rise in global supply is expected to be more modest—around 225,000 bpd—because key producers like Iraq, Kazakhstan, and Russia are already operating near their recent production levels. While Saudi Arabia has boosted output by 375,000 bpd since February, its exports are expected to decline by about 200,000 bpd in July due to increased domestic demand during the summer months.

The supply outlook remains tilted to the upside, with OPEC+ likely to continue unwinding its previous 2.2 million bpd production cuts. The group is expected to announce additional increases in August, September, and October, potentially eliminating the remaining voluntary cuts. While the gradual return of barrels will increase global supply, domestic demand in key exporting nations and uncertainties over actual delivery may keep oil prices somewhat supported in the near term.

Notably, OPEC+ has been steadily unwinding production cuts since April, with further increases implemented in May, June, and July. This raises the likelihood of additional hikes in August and beyond, potentially pushing the oil market into a surplus of 600,000 bpd in the July-September 2025 period and up to 850,000 bpd in the October-December 2025 quarter.

Outlook

Crude oil prices are expected to trade with a mildly bullish bias this month, supported by improving global market sentiment, tight oil inventories, and summer demand. However, gains are likely to be capped by OPEC+ output hikes and unresolved US-China trade frictions. Despite recent optimism surrounding US-China talks, China has refrained from purchasing US crude for the second consecutive month, signalling that tensions remain unresolved.

DILIP KUMAR JHA

Editor

dilip.jha@polymerupdate.com