Click the icon to add a specified price to your Dashboard list. This makes it easy to keep track on the prices that matter most to you.

This week, PS prices down adjusted in the Asian region.

An industry source in Asia, on condition of anonymity, informed a Polymerupdate team member, "Polystyrene prices in Asia are experiencing downward pressure because of falling production costs and low demand. Demand continues to be weak in crucial sectors such as electronics, automotive, construction, and packaging. The prolonged demand for polystyrene (PS) exports from Asia has stayed constrained, prompting local producers to redirect their attention to the intra-Asia market. Asian PS suppliers have faced challenges in obtaining export opportunities due to weak demand from distant markets like Europe, the Americas, and the Middle East, where local supply is abundant and global consumption remains low. Consequently, they have progressively focused on neighbouring markets in Asia to offload material, heightening competition and exerting a bearish pressure on prices in the region.”

The source added, “In the upstream market, while the core fundamentals of the international crude oil market remain steady, crude prices are expected to trend lower in the near term. Support from a softer U.S. tariff stance, ongoing sanctions against major oil-producing nations, and strong U.S. summer demand is being outweighed by easing geopolitical tensions, OPEC+ production increases, and persistent global economic concerns. The market is maintaining a cautious outlook amid limited bullish momentum and lingering supply-side pressure.”

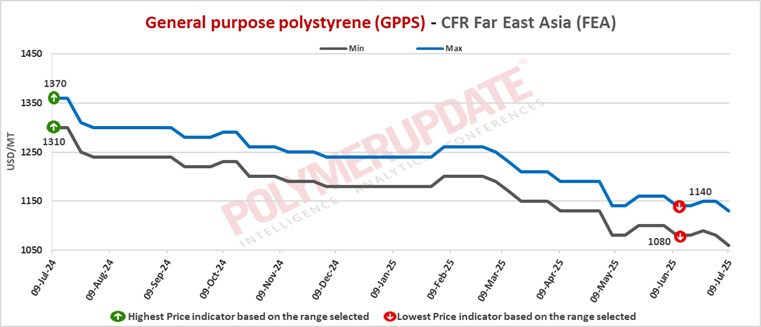

In China, GPPS prices were assessed at the USD 1060-1130/mt CFR levels, while HIPS prices were assessed at the USD 1170-1240/mt CFR levels, both dropped by USD (-20/mt) from the previous week.

In China, demand in the polystyrene (PS) spot import market stayed constrained, with only a handful of buyers expressing interest, mainly those with particular or pressing needs. The majority of participants remained inactive due to poor end-user demand and hesitant outlook, resulting in low activity in the CFR China market. This subdued demand has persistently affected overall market liquidity and pressurized sellers to offer competitive prices. In the meantime, various Chinese suppliers redirected their attention to the export market, where netbacks continued to be more advantageous than domestic sales. This shift towards exports heightened competition in key regional markets, especially in Southeast and South Asia, where an influx of attractively priced Chinese goods imposed additional pressure on domestic sellers and contributed to highly competitive pricing dynamics.

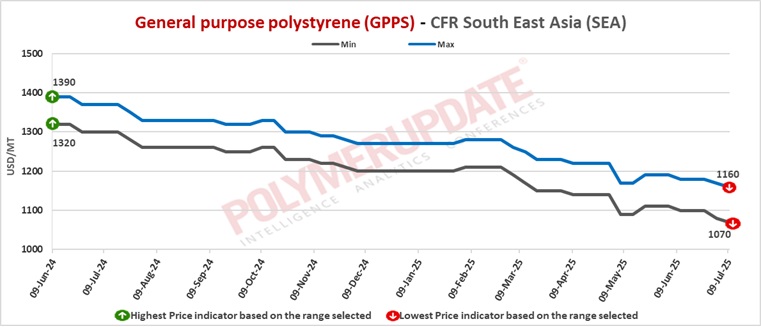

In Southeast Asia, GPPS prices were assessed at the USD 1070-1160/mt CFR levels, lower by USD (-10/mt) from last week. Meanwhile, HIPS prices were assessed stable at the USD 1180-1250/mt CFR levels.

Spot liquidity in the polystyrene market decreased considerably this week because of tariff concerns during the typical seasonal downturn. The US concluded a trade agreement with Vietnam that sets tariffs at 20% on imports and 40% on transshipped items, representing the first deal of this nature under the new US tariff policy in Southeast Asia. Although discussions may alleviate these tariffs, rates are still anticipated to stay elevated compared to earlier levels. Moreover, the US intends to release official tariff announcements with rates possibly varying between 10% and 70%, contributing to increased market uncertainty. Users of polystyrene are concerned about maintaining current demand if tariffs surpass expectations.

Taiwanese polystyrene (PS) producers are encountering heightened exchange rate risks because of the steep rise in the value of the New Taiwan dollar (NT$) compared to the US dollar. This change in currency has increased difficulties for exporters in sustaining healthy sales margins, as earnings in USD result in reduced returns when converted to NT$. The stronger NT$ has significantly diminished the profitability of global sales, applying further financial strain on manufacturers already facing low demand and regional pricing competition.

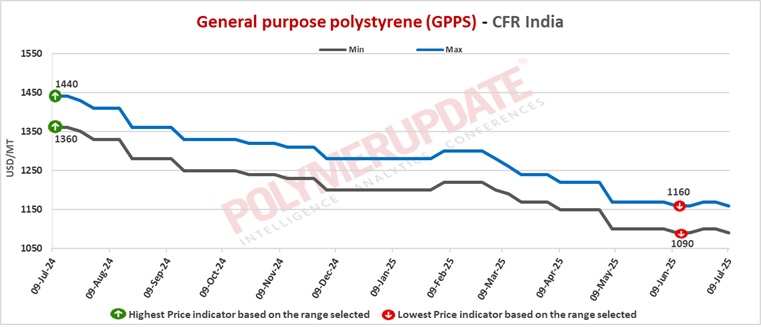

In India, GPPS prices were assessed at the USD 1090-1160/mt CFR levels, while HIPS prices were assessed at the USD 1170-1220/mt CFR levels, both week on week decreased by USD (-10/mt).

_prices_journey_southward_in_Asia_-_visual_selection_(1).png) A domestic industry source informed a Polymerupdate team member, “Supreme Petrochem has reduced GPPS grade prices by Rs.2/kg basic and HIPS grade prices by Rs.3/kg basic, with immediate effect.”

A domestic industry source informed a Polymerupdate team member, “Supreme Petrochem has reduced GPPS grade prices by Rs.2/kg basic and HIPS grade prices by Rs.3/kg basic, with immediate effect.”

In India, the seasonal slowdown in monsoon-related demand, the plentiful local supply of polystyrene imports from Iran, and recent price cuts in the domestic market have considerably reduced demand and acceptance for Asian material. The oversupply and competitive pricing landscape have created challenges for Asian exporters in establishing market presence, compelling numerous buyers to prefer more easily accessible and low-priced Iranian shipments. If demand does not increase following the monsoon season or if domestic prices don't stabilize, Asian suppliers might keep encountering difficulties in preserving their market share and pricing leverage in the region.

In Pakistan, GPPS prices were assessed at the USD 1150-1200/mt CFR levels, while HIPS prices were assessed at the USD 1250-1290/mt CFR levels, both fell by USD (-10/mt) from the previous week.

In Sir Lanka, GPPS prices were assessed at the USD 1140-1190/mt CFR levels while HIPS prices were assessed at the USD 1230-1280/mt CFR levels, both down adjusted by USD (-20/mt) week on week.

In Bangladesh, GPPS prices were assessed at the USD 1110-1160/mt CFR levels, down USD (-20/mt) from last week. HIPS prices were assessed at the USD 1190-1250/mt CFR levels, lower by USD (-10/mt) from the previous week.

In Bangladesh, the polystyrene market is experiencing a decline as weak seasonal demand aligns with a plentiful supply of competitively priced shipments from China. This pairing has considerably reduced general buyer interest and constrained conversations regarding the acquisition of Asian-sourced products. Consequently, regional traders and producers are being cautious, postponing new agreements and anticipating more distinct market indications. If demand does not increase or supply does not become limited, the market is expected to stay quiet in the short term, forcing local suppliers to present better pricing or consider different approaches to regain momentum in Bangladesh.

Even though direct trade of polystyrene (PS) between Asia and the US is restricted, the tariffs are anticipated to indirectly influence PS demand and production in the region. This effect will arise from a bottom-up approach, as trade operations in crucial downstream sectors like home appliances, toys, and packaging, which largely depend on general purpose polystyrene (GPPS) and high impact polystyrene (HIPS), might decelerate because of increased costs and diminished competitiveness. This could encourage certain downstream purchasers to redistribute sales channels or modify production strategies. It will adjust their PS purchasing volumes and frequency according to the revised trade dynamics.

Nonetheless, a few players are hopeful that the ongoing market weakness has mostly factored in uncertainties related to tariffs. As tariffs, seen as the major risk factor for H1 2025, are anticipated to be detailed in the upcoming weeks, sidelined buyers could obtain greater clarity for future budgeting and recommence regular restocking activity in a gradual manner.

In EPS, FOB North East Asia EPS general grade prices were assessed at the USD 1110-1130/mt levels while EPS fire-retardant grade prices were assessed at the USD 1180-1200/mt levels, both higher by USD (+20/mt) from the previous week.

Feedstock styrene monomer prices on Tuesday were assessed at the USD 890-900/mt FOB Korea levels while CFR China styrene monomer prices were assessed at the USD 900-910/mt levels, both constant week on week.

In plant news, Lianyungang Petrochemical has taken off stream its Polystyrene (PS) unit on June 25, 2025 for maintenance. The unit is slated to remain offline for about 20-25 days. Located in Lianyungang, China, the unit has a production capacity of 400,000 mt/year.