Click the icon to add a specified price to your Dashboard list. This makes it easy to keep track on the prices that matter most to you.

At least 40 percent of ethylene production capacity in the European Union faces the risk of closure due to ageing infrastructure and elevated production costs. Several projects have already announced shutdowns in recent years, driven by unaffordable energy prices—particularly for natural gas—and stricter environmental regulations. These factors, combined with global oversupply and a shift in demand towards sustainable chemicals, have eroded the competitiveness of the European chemical sector. The closure of multiple plants has increased the European Union’s reliance on imported primary chemicals, including key building blocks such as ethylene and propylene. These are essential inputs for the production of plastics, pharmaceuticals, and various industrial products. As a result, consumers in the European Union have ramped up imports of chemical raw materials from China and the Middle East, where these goods are more competitively priced compared to domestically produced alternatives.

The closure of multiple plants has increased the European Union’s reliance on imported primary chemicals, including key building blocks such as ethylene and propylene. These are essential inputs for the production of plastics, pharmaceuticals, and various industrial products. As a result, consumers in the European Union have ramped up imports of chemical raw materials from China and the Middle East, where these goods are more competitively priced compared to domestically produced alternatives.

Closure threat

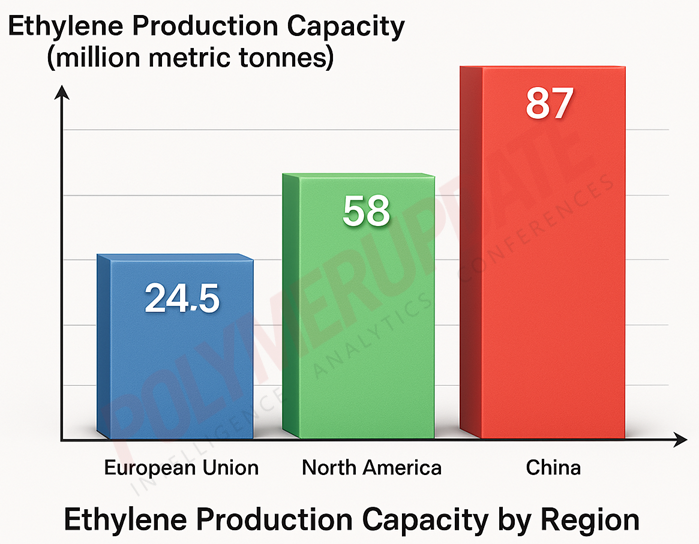

A report by the global consultancy firm Wood Mackenzie estimates the total ethylene production capacity in the European Union at 24.5 million metric tonnes (MMT). At least two-fifths of these plants are at high to medium risk of closure, including shutdowns announced since late 2024, the report stated. These facilities are primarily small- to mid-sized and have been operating at an average capacity utilisation of 80 percent or lower—levels considered economically unviable.

These plants are also required to comply with stringent environmental regulations, particularly regarding carbon dioxide (CO₂) emissions. A document issued in March this year by eight EU member states warned that over 50,000 jobs in the petrochemical industry could be at risk due to potential closures of additional crackers in Europe by 2035. Steam crackers, which convert hydrocarbons into base chemicals such as ethylene and propylene, are at the centre of this crisis. These chemicals are essential to a wide range of sectors, including plastics, pharmaceuticals, and industrial manufacturing.

Major chemical companies are shutting down operations in Europe after several consecutive years of financial losses. For example, Versalis—the petrochemical division of Italy’s Eni—has posted cumulative losses of over €3 billion over the past five years. The company has decided to close Italy’s last two steam crackers and redirect around €2 billion in investments toward bio-refineries and chemical recycling projects.

Similarly, other global players—including Dow Chemicals, ExxonMobil, Shell, and TotalEnergies—are either scaling back operations or reassessing their assets across Europe to stem losses. These companies have been incurring losses since 2023, largely due to elevated energy prices, particularly for natural gas, following supply disruptions from Russia in response to EU sanctions.

High energy costs

The European chemical industry reflects three significant recent changes. First, high prices for natural gas and electricity have driven up production costs for energy-intensive chemicals. Second, a global oversupply of many chemicals has resulted in depressed unit margins and reduced volumes. Third, demand is shifting towards more sustainable chemicals.

Most European facilities rely on naphtha—a derivative of crude oil refining—as their primary feedstock. As a result, European ethylene producers have been burdened with elevated raw material costs due to a sharp rise in naphtha prices in recent years. Prior to and during the COVID-19 outbreak, naphtha prices in Europe were quoted at around US$335–375 per metric tonne. At that time, benchmark Brent crude futures hovered around US$35–40 per barrel.

Immediately after Russia’s invasion of Ukraine in February 2022, Western nations, led by the United States, imposed multiple sanctions on Russian energy exports, even though several energy-dependent countries—many of them developed—relied heavily on supplies from Moscow. In retaliation, Russia curtailed energy supplies to Europe. Consequently, European countries were forced to source energy from the United States, which increased both costs and transit time.

This disruption led to a surge in energy prices across the European Union, making them unaffordable for many households and prompting governments to order the shutdown of energy-intensive factories. Brent crude prices subsequently doubled or even tripled from pre-COVID levels, averaging around US$70–80 per barrel. This pushed naphtha prices in the European market to US$500–550 per tonne, rendering many chemical plants economically unviable.

Unlike their counterparts in the United States, China, and the Middle East, European chemical producers had limited flexibility to upgrade plants and switch to ethane as a feedstock, due to cost constraints and existing infrastructure limitations.

Aging infrastructure

Using ethane as a raw material for ethylene production is significantly more cost-effective than using naphtha. Most ethylene plants in the United States, the Middle East, and China use ethane, which is derived from shale gas and natural gas liquids. In contrast, the European Union lacks access to shale gas and natural gas liquids, making its chemical plants largely dependent on naphtha as the primary feedstock for ethylene production.

According to reports, producing one tonne of ethylene in Europe costs approximately €740 when using naphtha. In comparison, U.S. producers can achieve costs below €370 per tonne using ethane, while Middle Eastern producers benefit from even lower rates—around €185 per tonne. These cost disparities are further exacerbated by ageing infrastructure: the average steam cracker in Europe is over 40 years old, compared to just 11 years in China, according to an analysis by Citi.

As a result, Europe has become structurally dependent on foreign chemical supplies. EU data shows that the bloc was a net importer of ethylene and propylene every year from 2019 to 2023.

Global capacity expansion

According to consulting firm ADI Analytics, North America's ethylene capacity is expected to grow to 58 million metric tonnes by 2030, up from 54 million metric tonnes currently. Meanwhile, China will add 6.5 percent to its ethylene capacity annually between 2025 and 2030, reaching nearly 87 million metric tonnes of ethylene production per year, China National Chemical Information Centre CEO Huang Yinguo said recently. That would be more than triple the EU's current capacity.

In contrast, Europe’s ethylene capacity has been contracting consistently. To circumvent European and U.S. tariffs, Chinese producers are setting up plants in Southeast Asia aimed at exporting directly to Western markets. Similar competitive pressures have forced Japanese and South Korean petrochemical producers to operate at reduced capacity since 2023.

In the Middle East, a €55 billion merger between Abu Dhabi National Oil Company (ADNOC) and Austria’s OMV will form the Borouge Group, which is poised to become the world’s fourth-largest polyolefins producer. Borouge plans to target the European market directly, adding further downward pressure on EU-based manufacturers.

DILIP KUMAR JHA

Editor

dilip.jha@polymerupdate.com