Click the icon to add a specified price to your Dashboard list. This makes it easy to keep track on the prices that matter most to you.

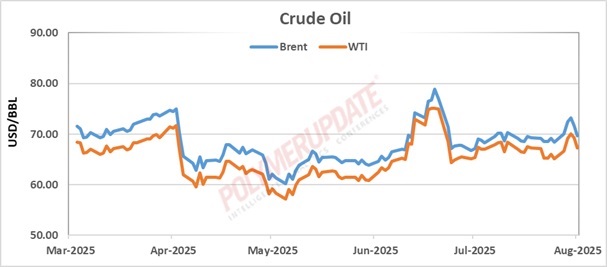

Crude oil prices settled higher last week amid sharp volatility, largely due to the most stringent sanctions imposed by the administration of President Donald Trump in the United States, targeting exports from Russia and Iran amid ongoing trade tensions and concerns over US tariffs. After sporadic gains, crude oil lost ground later in the week following expectations that the Organization of the Petroleum Exporting Countries and its allies (OPEC+) would raise output for September to compensate for the previously exercised voluntary output cut of 2.2 million barrels per day (bpd). Data compiled by Polymerupdate showed that benchmark Brent crude futures for near-month delivery on the InterContinental Exchange (ICE) began the week with strong gains, closing at US$ 70.04 a barrel on Monday, up from US$ 68.44 a barrel the previous day. The upward momentum continued, with the energy contract reaching a four-week high of US$ 73.24 a barrel on Wednesday, compared to US$ 72.51 a barrel on Tuesday. However, the gains could not be sustained, as Brent futures slumped on profit-booking to US$ 71.70 a barrel on Thursday, followed by a further decline of US$ 2.03 a barrel to US$ 69.67 a barrel on Friday. Despite the late-week pullback, Brent crude futures registered a weekly gain of 1.8 percent, or US$ 1.23 a barrel.

Data compiled by Polymerupdate showed that benchmark Brent crude futures for near-month delivery on the InterContinental Exchange (ICE) began the week with strong gains, closing at US$ 70.04 a barrel on Monday, up from US$ 68.44 a barrel the previous day. The upward momentum continued, with the energy contract reaching a four-week high of US$ 73.24 a barrel on Wednesday, compared to US$ 72.51 a barrel on Tuesday. However, the gains could not be sustained, as Brent futures slumped on profit-booking to US$ 71.70 a barrel on Thursday, followed by a further decline of US$ 2.03 a barrel to US$ 69.67 a barrel on Friday. Despite the late-week pullback, Brent crude futures registered a weekly gain of 1.8 percent, or US$ 1.23 a barrel.

Bullish sentiment also prevailed in West Texas Intermediate (WTI) Cushing futures at the start of the week, with the New York Mercantile Exchange (Nymex) near-month delivery contract closing Monday higher at US$ 66.71 a barrel, up from US$ 65.16 a barrel the previous day. Mirroring the trend in Brent, the WTI Cushing contract continued gaining momentum, reaching a one-month high of US$ 70 a barrel on Wednesday, up from US$ 69.21 a barrel on Tuesday. However, the US-centric contract retreated from this level, closing lower at US$ 69.26 a barrel on Thursday and further declining to US$ 67.33 a barrel on Friday, registering a weekly loss of 3.33 percent, or US$ 2.17 a barrel.

A report from Kedia Stocks and Commodities stated, “Crude oil prices dropped last week as markets reacted to escalating global trade tensions and a surprise build in U.S. crude inventories. The decline was primarily driven by concerns over the economic fallout from President Trump’s reaffirmed 10 percent global base tariff and newly announced retaliatory duties of up to 41 percent on nations without trade agreements with the U.S. Additionally, a 40 percent levy on rerouted goods has further amplified fears of reduced global trade flows, potentially weakening oil demand.” OPEC+ output hike

OPEC+ output hike

The eight OPEC+ countries, which had previously announced additional voluntary cuts in April and November 2023, have decided to implement a production increase of 547,000 bpd in September 2025 from the production level required in August 2025. The eight participating countries involved in these production adjustments are Saudi Arabia, Russia, Iraq, the United Arab Emirates (UAE), Kuwait, Kazakhstan, Algeria, and Oman. Leaders from these countries met virtually on August 3, 2025, to review global market conditions and outlook, and unanimously agreed to raise output for September.

In view of a steady global economic outlook and currently healthy market fundamentals, as reflected in low oil inventories, the decision aligns with the agreement reached on December 5, 2024, to initiate a gradual and flexible return of the 2.2 million bpd voluntary cuts starting from April 1, 2025. This return is structured over four monthly increments. However, OPEC+ leaders clarified that the phase-out of these additional voluntary production adjustments may be paused or reversed, depending on evolving market conditions. This flexibility will allow the group to continue supporting oil market stability.

Russian supply under stress

China, the world’s second-largest economy and largest oil importer, has backed India’s decision to import Russian oil through non-sanctioned service channels. Both India and China are crucial markets for Russian oil, absorbing nearly all volumes of crude diverted from Group of Seven (G7) countries due to sanctions. As a result, Russia has largely avoided the impact of sanctions imposed by the G7 nations, led by the United States.

On July 14, President Trump warned of fresh sanctions on buyers of Russian crude oil—including tariffs of up to 100 percent—if Moscow failed to sign a peace deal with Ukraine within 50 days, a deadline that was later shortened to 10–12 days. Russia accounts for nearly 11 percent of global crude oil supply and is also a key member of the OPEC+ coalition. It remains to be seen how Russia will respond to these new US sanctions, following the Kremlin’s missile attack on Ukraine in February 2022. Additionally, the G7 countries introduced a price cap of US$ 60 a barrel on Russian crude for open market purchases, which was later cut to US$ 47.60 a barrel in the recently announced in EU’s 18th sanctions package.

Sanctions on Iran

On Wednesday, the U.S. Treasury Department announced fresh sanctions on more than 115 Iran-linked individuals, entities, and vessels, escalating the Trump administration's maximum pressure campaign following the June bombing of Iranian nuclear sites. The U.S. had earlier imposed sanctions on several Chinese teapot refineries linked to the import of Iranian crude oil. In its largest Iran-related action since 2018, the Treasury Department’s Office of Foreign Assets Control (OFAC) designated over 50 individuals and entities and identified more than 50 vessels that are part of the vast shipping empire controlled by Mohammad Hossein Shamkhani (Hossein).

The U.S. State Department stated that Hossein—the son of Ali Shamkhani, a senior political advisor to Iran's Supreme Leader—leverages corruption through his father’s political influence at the highest levels of the Iranian regime to build and operate a massive fleet of tankers and containerships. This network transports oil, petroleum products, and other cargo from Iran and Russia to buyers worldwide, generating tens of billions of dollars in profits.

US inventory build

In yet another bearish indicator, the U.S. Energy Information Administration (EIA) reported a surge in crude oil inventories by 7.698 million barrels for the week ending July 25—the largest build in six months and contrary to expectations of a 2 million-barrel draw. Cushing inventories also rose by 690,000 barrels. However, gasoline stocks declined by 2.725 million barrels, signaling robust fuel consumption, while distillate stocks increased by 3.635 million barrels.

Despite these demand concerns, prices found some support from geopolitical risks. President Trump threatened to impose 100 percent secondary tariffs on buyers of Russian crude and warned China of severe penalties if it continues importing oil from Russia. Meanwhile, OPEC+ is expected to approve an output hike for September, although the size of the increase remains under discussion.

Outlook

While President Trump has accused Russia of using oil revenues to fund the war in Ukraine, he also accused Iran of using oil money to support Houthi pirates in carrying out terrorist activities in the Suez Canal and the Red Sea. Crude oil prices are likely to remain range-bound due to a mix of strong bullish and bearish fundamentals.

DILIP KUMAR JHA

Editor

dilip.jha@polymerupdate.com