Click the icon to add a specified price to your Dashboard list. This makes it easy to keep track on the prices that matter most to you.

This week, HDPE prices were left unchanged in the Asian region._prices.png) An industry source in Asia, on condition of anonymity, informed a Polymerupdate team member, “The Russia–Ukraine conflict remains a significant source of uncertainty, heightening concerns about disruptions to global supply chains. Simultaneously, persistent U.S. sanctions on major oil-producing countries have exacerbated already fragile market conditions. Together, these converging factors have driven up international crude oil prices, amplifying volatility and creating a more unpredictable landscape in the global energy market.”

An industry source in Asia, on condition of anonymity, informed a Polymerupdate team member, “The Russia–Ukraine conflict remains a significant source of uncertainty, heightening concerns about disruptions to global supply chains. Simultaneously, persistent U.S. sanctions on major oil-producing countries have exacerbated already fragile market conditions. Together, these converging factors have driven up international crude oil prices, amplifying volatility and creating a more unpredictable landscape in the global energy market.”

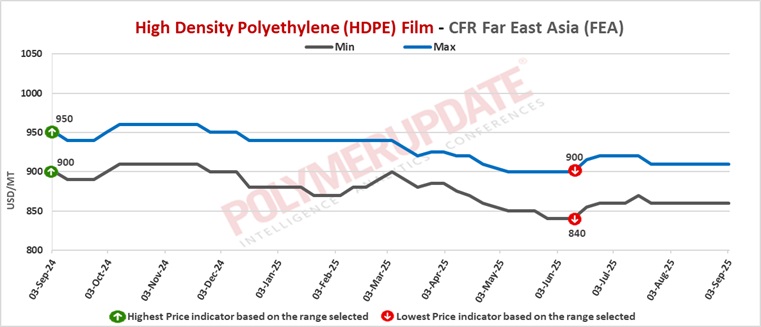

In Far East Asia, HDPE film prices were assessed at the USD 860-910/mt CFR levels while HDPE blow moulding prices were assessed at the USD 840-900/mt CFR levels, both steady week on week. HDPE injection prices were assessed stable at the USD 830-860/mt CFR levels, and HDPE yarn prices were assessed flat at the USD 880-900/mt CFR levels.

In China, a Saudi Arabian producer has offered its HDPE film grade at the USD 900/mt CFR levels, for shipment in September 2025. A producer from Middle East has offered its HDPE film grade at the USD 890-900/mt CFR levels, for shipment in September 2025. An Asian producer has offered its HDPE film grade in the range of USD 860-880/mt CFR levels, for shipment in September 2025.

In China, the HDPE market showed stability to softness, mainly affected by increasing disparities between buyer and seller expectations. Middle Eastern suppliers upheld strong pricing tactics in expectation of forthcoming Quarter 4 plant shutdowns, intending to achieve improved margins during times of decreased production. In contrast, purchasers favoured more economical U.S. shipments, resulting in transaction prices remaining close to the lower range of the market. The abundance of sufficient spot supply, along with a slow recovery in downstream markets, further limited price increases, as demand from downstream sectors stayed weak.

Despite an increase in dollar-denominated offers from various regions, actual trading activity stayed constrained, indicating a cautious market outlook. In general, the Chinese HDPE market is anticipated to stay fairly stable in the short term, experiencing only slight price variations as market players manage the equilibrium between supply, demand, and regional pricing factors.

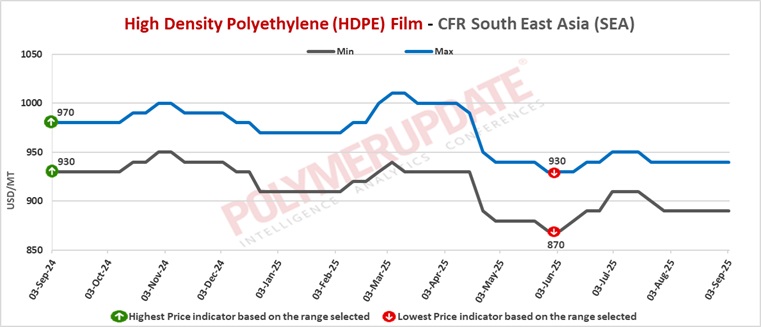

In Southeast Asia, HDPE film prices were assessed at the USD 890-940/mt CFR levels while HDPE blow moulding grade prices were assessed at the USD 840-890/mt CFR levels, both rolled over week on week. HDPE injection prices were assessed steady at the USD 840-890/mt CFR levels and HDPE yarn prices were assessed stable at the USD 920-960/mt CFR levels.

In Vietnam, a Saudi Arabian producer has offered its HDPE film grade at the USD 910-940/mt CFR levels, for shipment in September 2025. A producer from Middle East has offered its HDPE film grade at the USD 900/mt CFR levels, for shipment in September 2025. A South Korean producer has offered its HDPE film grade at the USD 900/mt CFR levels, for shipment in September 2025. A producer from USA has offered its HDPE film grade at the USD 880/mt CFR levels, for shipment in September 2025.

In the Philippines, a producer from Asia has offered its HDPE film grade at the USD 940/mt CFR levels, for shipment in September 2025. In Malaysia, an Asian producer has offered its HDPE film grade at the USD 940/mt CFR levels, for shipment in September 2025.

HDPE prices in Southeast Asia have seen a decline in demand despite stable pricing, as the introduction of new capacities in Malaysia and Vietnam has boosted supply and heightened competition in the market. The influence of US-sourced offers for shipments in November–December also played a role in the decrease, though total volumes are still restricted, preventing sharp price drops. Converters are currently replenishing their stocks in preparation for high demand seasons in October and November; nonetheless, total demand is still low compared to last year, with production facilities running at approximately 60% capacity rates. US exports continue to encounter challenges from reciprocal tariffs of 19–20%, which impair market competitiveness.

In Vietnam, HDPE offtake is anticipated to experience a minor increase before the Mid-Autumn Festival but is still projected to remain below 2024 figures. Regional import prices have stayed stable to weak, with reduced supply from the Middle East offering support for specific grades. However, the availability of competitively priced US and regional shipments has restricted any substantial price increases, leading to an overall cautious market perspective in Southeast Asia.

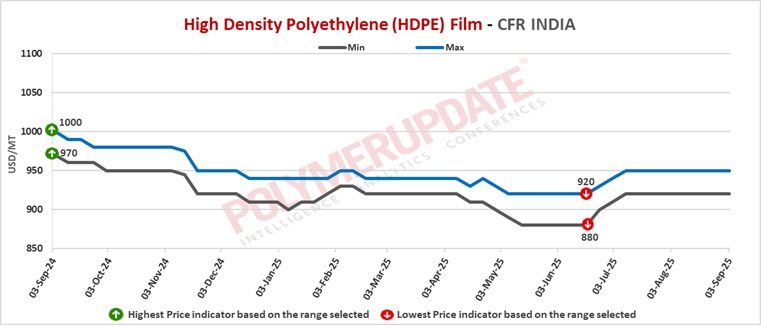

In India, HDPE film prices were assessed steady at the USD 920-950/mt CFR levels while HDPE yarn prices were assessed flat at the USD 900-940/mt CFR levels. HDPE Injection prices were assessed at the USD 910-960/mt CFR levels while HDPE blow moulding prices were assessed at the USD 910-930/mt CFR levels, both constant from the previous week.

A domestic industry source informed a Polymerupdate team member, “Reliance Industries Limited has rolled over HDPE grade prices, with effect from September 1, 2025.”

In India, a Middle Eastern producer has offered its HDPE film grade at the USD 930/mt CFR levels, for shipment in September 2025. Although bidding was heard at the USD 910/mt levels, it could not be confirmed officially.

In India, prices in the HDPE market have generally remained steady. Market sentiment in India has been significantly dull due to persistent macroeconomic issues. The recent U.S. decision to enforce an extra 25% tariff on Indian imports, raising total duties to 50%, coupled with the rupee’s drop to near-record lows against the dollar, has intensified trade uncertainties and escalated cost pressures for industries reliant on imports. This situation has led to hesitant purchasing patterns, as market players are looking for more definite offers before finalizing deals. Furthermore, intense rainfall in northern regions of the country has hindered logistics and supply chains, further undermining trade operations and business morale.

Outlooks for demand recovery before festivals are varied, as some sellers are hopeful for higher consumption from converters in September, while others are wary because of ongoing excess supply and pricing challenges. In particular, the demand for high-density polyethylene (HDPE) has declined, as various converters halted US-directed bag shipments due to the tariffs. Looking ahead, seasonal influences might offer some backing to demand; nevertheless, general restocking enthusiasm is expected to remain limited, hindered by cost pressures influenced by currency fluctuations and a surplus of regional supply, which together restrict market optimism.

In Pakistan, HDPE film prices were assessed at the USD 940-970/mt CFR levels while HDPE blow moulding grade prices were assessed at the USD 950-980/mt CFR levels, both unchanged from the previous week. HDPE yarn grade prices were assessed at the 950-980/mt CFR levels and HDPE injection grade prices were assessed at the USD 940-970/mt CFR levels, both constant week on week.

In Pakistan, Middle Eastern producers have offered their HDPE film grades in the range of USD 940-970/mt CFR levels, for shipment in September 2025.

In Pakistan, HDPE prices have stayed stable lately; however, market sentiment was generally weak with inclement weather affecting demand. Flooding and intense rainfall interrupted transport from import hubs and the Karachi port to production facilities, significantly limiting trade operations and logistics. The domestic market encountered extra strain due to an excess of material, prompted by large inventories stemming from heightened shipments of Iranian HDPE and prior orders placed in July. As demand stays low and supplies are abundant, market sources expect that supply glut situations will probably continue until October, putting downward pressure on prices and restricting market activity.

In Sri Lanka, HDPE film prices were assessed at the USD 940-980/mt CFR levels and HDPE blow moulding prices were assessed at the USD 940-980/mt CFR levels, both stable from last week. HDPE injection grade prices were assessed at the USD 950-970/mt CFR levels while HDPE yarn grade prices were assessed at the USD 960-980/mt CFR levels, both unchanged week on week.

In Sri Lanka, overseas producers have offered their HDPE film grades in the range of USD 940-980/mt CFR levels, for shipment in September 2025.

In Bangladesh, HDPE blow moulding prices were assessed steady at the USD 920-960/mt CFR levels. HDPE film prices were assessed flat at the USD 930-970/mt CFR levels. HDPE Injection grade prices were quoted steady at the USD 920-960/mt CFR levels. HDPE yarn prices were assessed stable at the USD 920-960/mt CFR levels.

In Bangladesh, Middle Eastern producers have offered their HDPE film grades in the range of USD 930-970/mt CFR levels, for shipment in September 2025.

In Sri Lanka and Bangladesh, HDPE prices stayed relatively consistent amid subdued buying activity. Market participants reported limited purchasing interest from both end-users and distributors, largely due to ongoing economic uncertainties, cautious sentiment, and concerns over demand recovery. Buyers appeared hesitant to commit to new imports amid fluctuating market conditions and high inventories. As a result, despite steady prices, the overall activity level remained muted, indicating a wait-and-see approach until clearer demand signals emerge in the region.

Feedstock ethylene prices on Tuesday were assessed at the USD 835-845/mt CFR North East Asia levels, stable week on week. CFR South East Asia ethylene prices were assessed at the USD 830-840/mt levels, higher by USD (+5/mt) from the previous week.

In plant news, USI Corp has taken off stream its High density polyethylene (HDPE) unit around September 1, 2025 for maintenance. However, details regarding the duration of the shutdown remain unclear. Located in Kaohsiung, Taiwan, the HDPE unit has a production capacity of 160,000 mt/year.

In other plant news, Ningxia Baofeng Energy has taken off stream its High density polyethylene (HDPE) unit around August 31, 2025, for maintenance. However, the exact date and duration of the shutdown remain unclear. Located in Yinchuan, Ningxia in China, the HDPE unit has a production capacity of 400,000 mt/year.

In another plant news, Sinopec Maoming Petrochemical is likely to undertake a planned turnaround at its High density polyethylene (HDPE) units in early November 2025. However, details regarding the duration of the shutdown remain unclear. Located in Guangdong, China, the HDPE units have a production capacity of 400,000 mt/year.