Click the icon to add a specified price to your Dashboard list. This makes it easy to keep track on the prices that matter most to you.

The global polymer market is witnessing a sharp upward trajectory in prices as escalating geopolitical tensions in the Middle East—triggered by the ongoing U.S.–Israel conflict with Iran—disrupt energy supplies and petrochemical trade flows. The effective closure of the Strait of Hormuz, coupled with Iranian missile strikes on key oil and gas infrastructure across Gulf countries, has triggered a surge in crude oil and feedstock costs, sending shockwaves across the plastics value chain. At the heart of the rally is the steep increase in crude oil prices, which have climbed above US$ 100 a barrel following repeated attacks on energy infrastructure and export facilities in the Gulf region. The Strait of Hormuz, a critical artery for nearly one-fifth of global oil flows, has seen traffic collapse amid security threats, severely curtailing exports from major producers such as Saudi Arabia, the UAE, Kuwait and Iraq. This unprecedented disruption has tightened global energy balances and significantly inflated the cost of petroleum-derived feedstocks.

At the heart of the rally is the steep increase in crude oil prices, which have climbed above US$ 100 a barrel following repeated attacks on energy infrastructure and export facilities in the Gulf region. The Strait of Hormuz, a critical artery for nearly one-fifth of global oil flows, has seen traffic collapse amid security threats, severely curtailing exports from major producers such as Saudi Arabia, the UAE, Kuwait and Iraq. This unprecedented disruption has tightened global energy balances and significantly inflated the cost of petroleum-derived feedstocks.

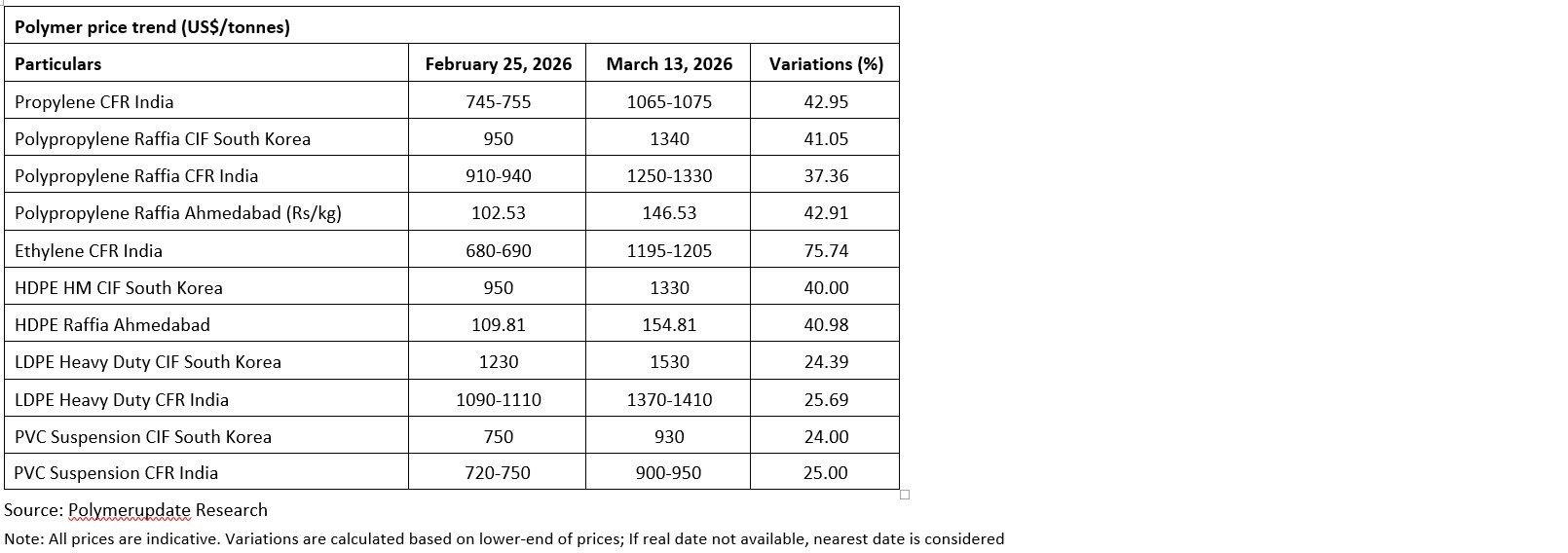

Polymer prices up 24-75% in two weeks

Polymer prices (indicative) have surged sharply by around 41–42 percent since the outbreak of the Israel–US war with Iran on February 28, 2026, as escalating geopolitical tensions disrupted global energy and petrochemical supply chains. The rally has been primarily driven by a steep increase in crude oil and naphtha prices following the effective closure of the Strait of Hormuz and repeated attacks on Gulf energy infrastructure. With nearly one-fifth of global oil flows passing through this route, the disruption has sharply inflated feedstock costs, directly impacting polymer production economics. Industry data and market feedback indicate that prices of key polymers such as polyethylene (PE), polypropylene (PP), and PET have risen significantly within a short span, with some segments witnessing increases of over 40% in less than two weeks.

The sharp rise reflects a combination of supply-side constraints and cost-push pressures across the value chain. Petrochemical exports from the Middle East have been severely disrupted due to refinery outages, force majeure declarations, and logistical bottlenecks, tightening global availability. At the same time, soaring freight rates, insurance premiums, and rerouting of cargoes have further increased the landed cost of polymers, particularly in import-dependent markets like Asia. The spike in polymer prices has already begun cascading into downstream industries, with packaging costs rising and manufacturers facing acute margin pressure amid volatile raw material markets. Being a price taker, India has also seen a substantial increase in the domestic-origin polymer prices with all primary producers raising them proportionately.

Naphtha prices surge

The prices of naphtha, a key raw material for steam crackers producing olefins like ethylene and propylene have witnessed an extraordinary surge of nearly 74 percent within just two weeks of the Israel–US war with Iran that erupted on February 28, 2026, reflecting the intensity of the supply shock gripping global energy and petrochemical markets. Naphtha prices CFR for East Asia, for example, rose to settle at US$ 1077-1079 a tonne on March 17, up from US$ 619-621 a tonne two weeks ago. The sharp escalation in crude oil prices—driven by the effective blockade of the Strait of Hormuz and widespread attacks on oil and refining infrastructure across the Gulf—has directly lifted naphtha values, given its close linkage to crude. Market data indicates that crude prices themselves surged by over 35–50% at peak levels during the initial phase of the conflict, creating a strong cost-push effect across downstream products such as naphtha.

The rally in naphtha has been further amplified by severe supply disruptions and logistical bottlenecks. Refinery run cuts across the Middle East and other regions, coupled with difficulties in moving cargoes due to security risks in key shipping lanes, have tightened global availability of the feedstock. Traders report that millions of barrels per day of refining capacity are at risk due to the ongoing conflict, while buyers in Asia and Europe are scrambling to secure alternative cargoes, adding a premium to already elevated prices. The sharp spike in naphtha prices has significantly increased production costs for steam crackers, thereby cascading into higher prices for downstream petrochemicals and polymers, and intensifying inflationary pressures across manufacturing sectors.

Naphtha has recorded a sharp spike in prices, rising nearly 20 percent within a matter of days in early March. The surge reflects a combination of supply shortages, elevated refining margins and logistical bottlenecks caused by tanker disruptions and higher freight costs. Since a majority of Asia’s petrochemical capacity relies on naphtha-based cracking, the increase in feedstock costs has directly translated into higher production costs for downstream polymers such as polyethylene (PE) and polypropylene (PP).

Feedstocks shortage

Compounding the situation is the disruption of petrochemical exports from the Middle East, a region that accounts for a substantial share of global polymer supply. With nearly 84 percent of Middle Eastern polyethylene exports dependent on the Strait of Hormuz, the blockage has constrained availability in key importing regions including Asia and Europe. The resulting supply squeeze has intensified competition for available cargoes and pushed polymer prices higher across global markets.

Recent industry reports indicate that petrochemical and polymer prices have surged globally due to feedstock shortages and supply chain disruptions stemming from the conflict. In India, the impact is already visible at the ground level, with polybag prices in key manufacturing hubs rising by as much as 80 percent due to escalating raw material costs linked to naphtha. Processors and converters are facing severe margin pressure, with many reluctant to accept new orders amid daily price volatility.

Ripple effects

The ripple effects extend beyond feedstock costs. Iranian strikes on refineries, storage facilities and export terminals across the Gulf have forced production cuts and halted shipments of refined products and petrochemicals. This has not only tightened supply but also disrupted integrated supply chains that feed into global plastics manufacturing. At the same time, several steam crackers in Asia have either reduced operating rates or shut down temporarily due to high input costs and uncertain feedstock availability, further constraining polymer output.

Freight and logistics challenges are adding another layer of cost pressure. With shipping routes through the Gulf deemed high-risk, freight rates have surged and alternative routes have lengthened delivery timelines, increasing the landed cost of polymers. The breakdown of just-in-time supply chains has forced buyers to secure material at higher premiums, reinforcing the bullish trend in polymer markets.

Outlook

Looking ahead, polymer prices are expected to remain firm with a strong upward bias as long as geopolitical tensions persist and the Strait of Hormuz remains effectively closed. While strategic reserve releases by major economies may offer temporary relief in crude markets, they do little to address shortages in petrochemical feedstocks and derivatives. Moreover, the structural dependence of the global plastics industry on Middle Eastern supply suggests that any prolonged disruption will keep polymer markets tight and volatile.

In conclusion, the ongoing conflict has exposed the vulnerability of the global petrochemical ecosystem to geopolitical shocks. With crude oil, naphtha and downstream polymer supply chains deeply interconnected, the current crisis is likely to sustain elevated polymer prices, squeeze margins for converters, and ultimately translate into higher costs for end-use industries ranging from packaging to textiles and automotive.

DILIP KUMAR JHA

Editor

dilip.jha@polymerupdate.com