Click the icon to add a specified price to your Dashboard list. This makes it easy to keep track on the prices that matter most to you.

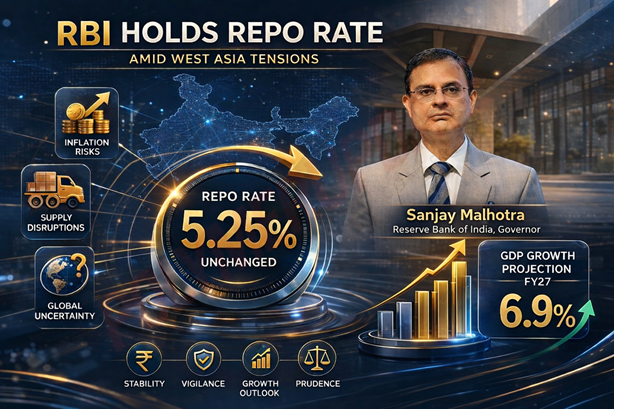

The Reserve Bank of India (RBI) on Wednesday kept the key repo rate unchanged at 5.25 percent due to ongoing economic growth challenges, despite a two-week ceasefire between the United States and Iran announced earlier in the day. The truce will halt over five weeks of drone and missile strikes and help reopen the critical transit waterway—the Strait of Hormuz—resulting in smoother movement of oil tankers and merchant ships that had remained largely disrupted since the US and Israel jointly began strikes on Iran on February 28, 2026. The decision was taken unanimously at the three-day Monetary Policy Committee (MPC) meeting that concluded on Wednesday, following a detailed assessment of evolving macroeconomic and financial developments and the outlook. The MPC voted unanimously to keep the policy repo rate under the Liquidity Adjustment Facility (LAF) unchanged at 5.25 percent. Consequently, the Standing Deposit Facility (SDF) rate remains at 5 percent, while the Marginal Standing Facility (MSF) rate and the Bank Rate remain at 5.5 percent. The Committee also decided to continue with the neutral stance.

The decision was taken unanimously at the three-day Monetary Policy Committee (MPC) meeting that concluded on Wednesday, following a detailed assessment of evolving macroeconomic and financial developments and the outlook. The MPC voted unanimously to keep the policy repo rate under the Liquidity Adjustment Facility (LAF) unchanged at 5.25 percent. Consequently, the Standing Deposit Facility (SDF) rate remains at 5 percent, while the Marginal Standing Facility (MSF) rate and the Bank Rate remain at 5.5 percent. The Committee also decided to continue with the neutral stance.

Announcing the decision of the MPC’s first meeting in FY 2026–27, RBI Governor Sanjay Malhotra stated, “After a detailed assessment of evolving macroeconomic and financial developments and the outlook, the MPC voted unanimously to keep the policy repo rate unchanged at 5.25 percent. Since the last policy meeting two months ago, geopolitical uncertainties have heightened significantly. The global economy is facing unprecedented challenges from elevated geopolitical tensions, the conflict in West Asia, and disruptions in global supply chains.”

Dipti Deshpande, Principal Economist at Crisil Ltd, commented, “The MPC maintaining status quo on both the policy rate and monetary policy stance was along expected lines. The raft of uncertainties arising from the West Asia conflict calls for prudence. It would be premature to draw firm conclusions on the impact or pre-empt the ultimate outcome of the conflict. At this juncture, what is required is maintaining adequate policy buffers and remaining nimble to act as the situation evolves.”

Rationale behind the rate pause

Before the outbreak of the conflict, India’s macroeconomic fundamentals exuded confidence, with buoyant growth and low inflation. Conditions turned adverse in March with the widening and intensification of the conflict. The fundamentals of the Indian economy are on a stronger footing at present than during previous crisis episodes, as well as relative to many other economies, providing greater resilience to withstand shocks.

Global growth faces increasing downside risks as the sharp rise in energy prices (up to 74 percent over the past five weeks) and shortages of inputs across various industries have stoked inflation fears and pushed up the geopolitical risk premium in oil markets. Heightened uncertainty precipitated by the ongoing conflict is weighing on the outlook. Safe-haven flows have exerted depreciation pressure on the currencies of major economies as the US dollar has strengthened.

While commodity prices, such as metals and gold, have moderated, financial markets have become more volatile. Equities have registered a broad-based correction. Sovereign bond yields, already elevated due to long-term fiscal sustainability concerns and driven by inflation fears, have hardened across major economies.

Impact of West Asia crisis

The initial supply shock that emerged after the West Asia crisis could potentially transform into a demand shock over the medium term if the restoration of supply chains is further delayed. This shock could have a negative impact on the Indian economy on several counts. First, elevated crude oil prices could increase imported inflation and widen the current account deficit (CAD). Second, disruptions in energy markets, fertilisers, and other commodities may adversely affect industry, agriculture, and services, thereby reducing domestic output.

Third, heightened uncertainty, increased risk aversion, and safe-haven demand could impact domestic liquidity conditions, economic activity, consumption, and investment. Fourth, weaker global growth prospects may dampen external demand and reduce remittance flows. Finally, adverse spillovers from global financial markets could tighten domestic financial conditions and raise borrowing costs. Growth impulses continue to be supported by robust private consumption and investment demand.

However, the West Asia conflict is likely to impede growth. Higher input costs arising from increased energy prices, along with rising international freight and insurance costs and supply chain disruptions that constrain the availability of key inputs for downstream sectors, could impair growth. However, the government’s prompt measures aimed at supporting exports and protecting supply chains may help mitigate the adverse impact of the conflict.

“Therefore, it is prudent to wait and watch the changing circumstances and the evolving growth-inflation outlook. Accordingly, the MPC has decided to remain vigilant and closely monitor incoming information,” Malhotra added.

GDP growth forecasts

Meanwhile, the Indian economy remained resilient in FY 2025–26. Real gross domestic product (GDP) is projected to grow by 7.6 percent (year-on-year) during the year, as per the Second Advance Estimates (SAE) of the new GDP series (base year 2022–23). Private consumption and fixed investment contributed significantly to overall growth, while net external demand remained soft. On the supply side, estimated real Gross Value Added (GVA) growth of 7.7 percent was driven by a buoyant services sector and robust manufacturing activity.

On the external front, merchandise exports may be adversely impacted by disruptions to key shipping routes and the concomitant rise in freight and insurance costs if the conflict is prolonged. On the other hand, sustained momentum in the services sector, the continuing impact of GST rationalisation, rising capacity utilisation in manufacturing, and healthy balance sheets of financial institutions and corporates should continue to support domestic demand.

In this milieu, the government’s focus on scaling up domestic manufacturing in several strategic and frontier sectors, as announced in the Union Budget 2026–27, bodes well for India’s growth trajectory. Considering these factors, the RBI has projected India’s real GDP growth for 2026–27 at 6.9 percent, with Q1 at 6.8 percent, Q2 at 6.7 percent, Q3 at 7.0 percent, and Q4 at 7.2 percent.

Inflation projections

As per the new Consumer Price Index (CPI)-based retail inflation series (2024=100), headline inflation increased to 3.2 percent in February 2026 from 2.7 percent in January. The uptick was primarily driven by unfavourable base effects, even as momentum remained muted. While food inflation increased in February, core inflation (excluding food and fuel) remained unchanged. Excluding precious metals, core inflation remained moderate at 2.1 percent in January and February, suggesting subdued underlying inflationary pressures.

The pass-through of higher global energy prices has led to price increases in select fuels such as premium petrol, liquefied petroleum gas (LPG), and diesel for industrial use. On the other hand, near-term food supply prospects have improved, supported by a robust rabi crop, providing some comfort. Considering these factors, CPI inflation for 2026–27 is projected at 4.6 percent, with Q1 at 4.0 percent, Q2 at 4.4 percent, Q3 at 5.2 percent, and Q4 at 4.7 percent. Persistently elevated energy prices due to the West Asia conflict, along with possible El Niño conditions (which could negatively impact the southwest monsoon), pose upside risks to inflation. Core inflation is projected at 4.4 percent for 2026–27.

DILIP KUMAR JHA

Editor

dilip.jha@polymerupdate.com