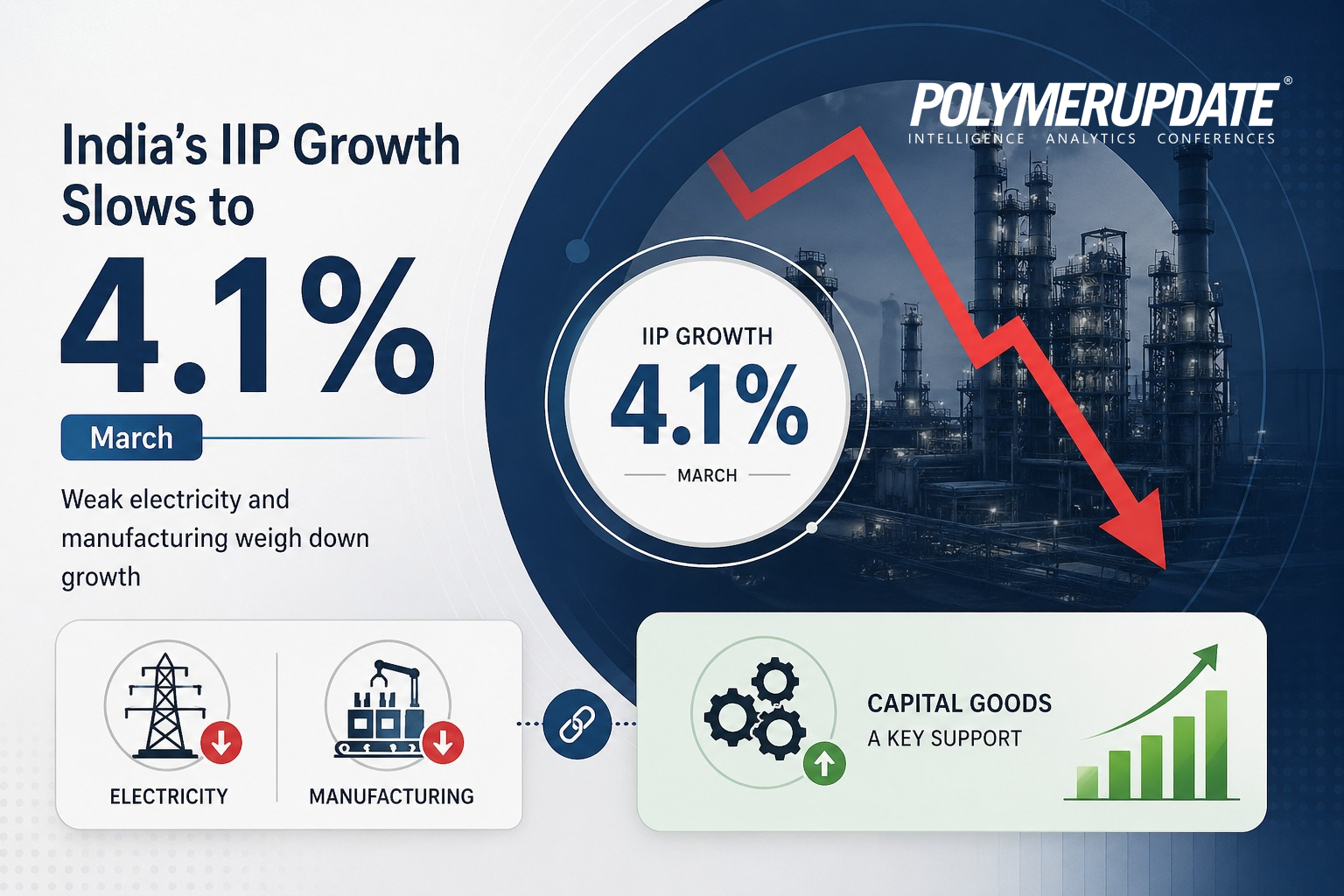

India’s factory output growth, measured by the Index of Industrial Production (IIP), slowed to a five-month low of 4.1 percent in March due to a sharp moderation in electricity generation, sluggish momentum in manufacturing, and raw material supply disruptions arising from geopolitical conflicts in West Asia. However, the slowdown in the manufacturing sector was partly offset by continued strength in the capital goods segment. Notably, the March IIP reflects a decline from 5.1 percent in February 2026, though it is higher than 3.9 percent recorded in March 2025.

Data compiled by the Ministry of Statistics & Programme Implementation (MoSPI) showed that India’s IIP grew by 5.2 percent in February 2026, improving from 4.8 percent in January 2026, driven by a 6 percent rise in manufacturing, 3.1 percent growth in mining, and 2.3 percent in electricity. The February growth was supported by strong performance in basic metals (13.2 percent) and motor vehicles (14.9 percent). The IIP growth rate for March 2026 stood at 4.1 percent, compared with 5.2 percent (Quick Estimate) in February 2026.

Madan Sabnavis, Chief Economist at Bank of Baroda, said, “Industrial growth, as measured by the IIP, was 4.1 percent in March, which is higher than our expectations of 1–2 percent. For the full year, it stood at 4.1 percent. This number is therefore impressive, given that core sector growth was negative for the month. The March IIP assumes significance as it is the first month of the war when the impact would have been felt at a preliminary level. Manufacturing stood out with 4.3 percent growth, which is comforting. Mining rose by 5.5 percent and electricity by 0.8 percent.”

Manufacturing sector growth

Manufacturing sector growthThe growth rates of the three sectors—mining, manufacturing, and electricity—for March 2026 were 5.5 percent, 4.3 percent, and 0.8 percent, respectively. The Quick Estimate of the IIP stands at 173.2, compared with 166.3 in March 2025. The indices of industrial production for the mining, manufacturing, and electricity sectors in March 2026 stood at 166.8, 169.4, and 221.3, respectively.

Dipti Deshpande, Principal Economist at Crisil Ltd, said, “Industrial output slowed in March as IIP growth eased, broadly reflecting the early impact of the West Asia conflict. Key sectors such as textiles, chemicals, electronics, leather products, and wood products reported a decline in output year-on-year, while refining, food products, paper products, non-metallic mineral products, basic metals, and electrical equipment saw slower output growth year-on-year. Sectors such as automobiles and machinery and equipment continued to register improvement.”

Domestic manufacturing has begun to bear the brunt of costlier and tighter supplies of petroleum products and natural gas. Manufacturing IIP growth slowed to 4.3 percent from 5.9 percent. The Purchasing Managers’ Index also slipped in March from February but remained in the expansion zone, indicating a likely uneven impact of the conflict across sectors and over time, depending on their ability to absorb the shock. The impact on a sector’s output will occur when inputs become more expensive or less available.

Energy supply restorationWhile the government is gradually restoring the supply of energy and other critical inputs to industry, the prolonged conflict has kept commodity prices elevated. Crisil has lowered its gross domestic product (GDP) growth forecast for fiscal 2027 to 6.8 percent from 7.1 percent. The revision reflects the impact of two full months of the West Asia conflict, including damage to energy infrastructure, the effects of which are likely to linger amid gas supply shortages and higher input and shipping costs.

Although some manufacturers are expected to switch to alternative fuels to compensate for natural gas shortages, cost pressures will persist. Export disruptions will further weigh on the domestic industry. The March data capture only part of the shock, as uncertainty and weak producer sentiment have yet to fully manifest in production data. The deeper impact is expected to emerge over time, particularly in the first quarter of the current fiscal year.

Key takeawaysFourteen of the 23 industries showed positive growth. The leaders were the auto segment, followed by machinery, metal products, and basic metals. On the downside, the consumer electronics segment recorded negative growth. Industries such as food products, leather, wood, chemicals, and textiles witnessed a decline in output. Weak export demand also contributed partly to the subdued performance. The pharmaceutical sector, too, recorded muted growth.

Industries related to capital formation witnessed better traction and supported overall growth. Accordingly, capital goods and infrastructure sectors performed well. The consumer goods segment, however, continued to present a mixed picture. Consumer durables grew by 5.3 percent, aided mainly by the auto segment, while electronics remained in the negative zone.

Fast-moving consumer goods (FMCG) continued to lag, with growth of just 1.1 percent. It remains to be seen whether there will be any reversal in April. The impact of GST has not yet been reflected in terms of higher demand for FMCG products. Meanwhile, the capital goods and infrastructure segments have witnessed healthy growth, supported by front-loaded government spending on capital expenditure.

DILIP KUMAR JHA

Editor

dilip.jha@polymerupdate.com