Click the icon to add a specified price to your Dashboard list. This makes it easy to keep track on the prices that matter most to you.

By Professor Dr Sajjid Mitha

CEO & Founder, Polymerupdate | Polymerupdate Academy | RACE Expos and Conferences

The trains running from Xi'an to Tehran are not merely moving goods. They are moving history.

For the better part of a century, the architecture of global commerce has been, at its core, a maritime proposition — and, by extension, an American one. From the Strait of Malacca to the Strait of Hormuz, from the choke of Suez to the breadth of the Pacific, the world's trade has flowed through passages that the United States Navy has, explicitly or tacitly, held in trust. This was not mere projection; it was the operating system of the postwar order. Whoever commanded the sea-lanes commanded the system.

What is changing is not the oceans. It is the cost of needing them.

I. THE CORRIDOR

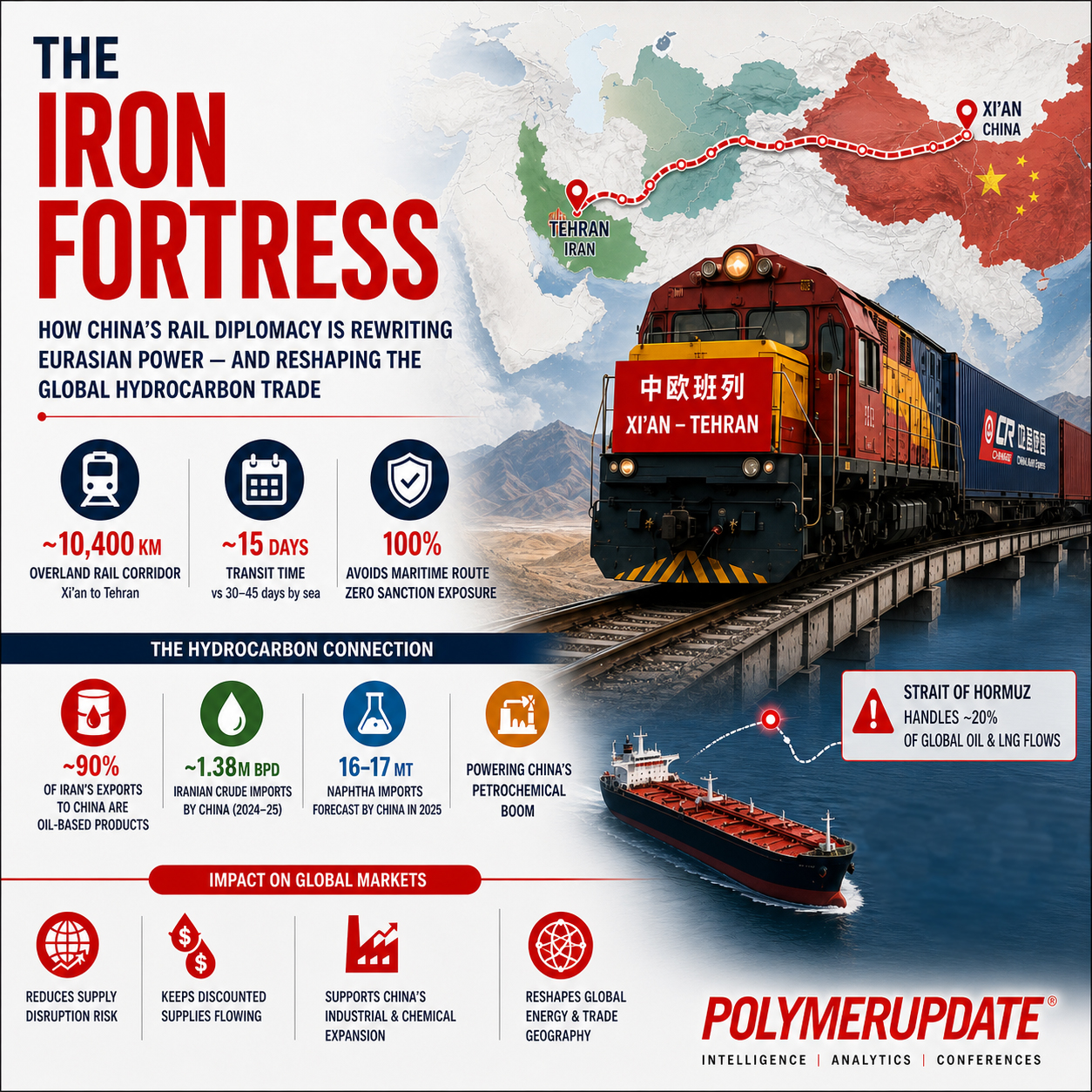

When the Xi'an–Tehran rail corridor came to life in 2025, the logistical particulars attracted predictable attention: roughly 10,400 kilometres of track, transit times compressed to some 15 days, a ribbon of steel drawn across the ancient heartland of Eurasia to terminate at Iran's Aprin Dry Port. The numbers are impressive enough on their own terms. But to read this as a story about faster shipping is to miss the point by a considerable distance.

The corridor's true significance is jurisdictional.

This is trade that never touches a coastline. It never enters contested waters. It never passes through a port where a compliance officer, an insurance underwriter, or a U.S. Treasury designation might slow or strangle it. From departure to arrival, it moves through the sovereign territories of politically aligned states, beyond the operational reach of the enforcement mechanisms that Western powers have spent decades perfecting. The rails are infrastructure. The jurisdiction is strategy.

For Beijing, the corridor represents the most credible answer yet to what military planners have long called the "Malacca dilemma" — the uncomfortable dependence on a single maritime artery through which the bulk of China's seaborne energy imports must pass, and which, in a crisis, could be interdicted. No single overland corridor eliminates that vulnerability; the arithmetic of maritime shipping, where one vessel carries what dozens of trains cannot, ensures the sea retains its primacy. But primacy and monopoly are different things. What the rail spine provides is dilution — enough optionality to change strategic calculations, even if not enough to overturn them.

For Tehran, the calculus is more immediate, and the stakes more visceral. Sanctions, in their modern form, are an instrument of financial topology: they work by controlling the ledgers, the registries, the clearing systems, and the maritime insurance networks through which global commerce moves. Move the commerce overland, through states that neither recognise the sanctions nor enforce them, and the instrument loses its edge. Geography, transformed by infrastructure, becomes leverage. The corridor does not make Iran sanction-proof. But it makes Iran meaningfully harder to isolate — and that is a different kind of power.

II. THE HYDROCARBON THREAD

To understand what is actually moving along this corridor — and what it means — requires a detour into chemistry as much as geopolitics.

Roughly ninety percent of Iran's exports to China are oil-based products: petrochemicals, petroleum products, and gases, alongside mining commodities such as copper and iron concentrate. This is not a bilateral trading relationship so much as a vertical supply chain disguised as diplomacy — and hydrocarbons are its connective tissue.

Begin with crude. Between 2024 and 2025, China imported approximately 1.38 million barrels per day of Iranian crude oil, accounting for around 13.4 percent of the country's total maritime oil imports, with over eighty percent of Iran's crude exports flowing to a single buyer: China. The scale of this dependency is remarkable on both sides. Iran cannot meaningfully sell its oil without China, and China has quietly built its feedstock security around Iranian supply. The gap left by China's major state-owned refineries — which pulled back from Iranian crude after the United States withdrew from the nuclear deal in 2018 — was filled by independent refineries, the so-called "teapots" clustered in Shandong province, which by 2025 accounted for an estimated ninety percent of Iran's oil exports to China. These nominally private operations have provided Beijing with a layer of plausible deniability while sustaining the flow; beneath their independent exteriors, many connect closely to the Chinese state through joint ventures and partnerships with state-owned enterprises.

“The teapots don't operate in a vacuum. Everyone in Shandong knows where the crude is coming from, and everyone has quietly made their peace with it. The discount is too good, the volumes too reliable, and the government is not exactly losing sleep over it.”

— A Shandong-based crude trading executive, speaking on condition of anonymity

The rail corridor's most immediately practical hydrocarbon role, however, is not crude — it is the lighter, more manageable products that sit higher up the value chain. Naphtha — the pale, volatile feedstock that steam crackers consume to produce ethylene and propylene, the molecular ancestors of nearly every plastic on earth — is where the geopolitical and the industrial converge with particular force. China is the world's largest naphtha importer, with analysts forecasting purchases of around 16 to 17 million tonnes in 2025 alone, driven by a wave of new petrochemical capacity coming online. Iranian naphtha, priced at a steep discount to Middle Eastern benchmarks, feeds those crackers cheaply and, when it moves overland, invisibly. The volumes are significant enough to have drawn repeated U.S. Treasury enforcement actions, with sanctioned shadow-fleet tankers documented carrying millions of barrels of Iranian naphtha through circuitous transshipment routes to obscure origin.

Iran converts its hydrocarbons into progressively more refined products — crude to naphtha, naphtha to ethylene, ethylene to polyethylene — and moves them east along a route that Western enforcement mechanisms cannot easily reach.

The polymers tell a similar story, and one with greater commercial texture. Iran's leading petrochemical exports include methanol, polyethylene in both high-density and low-density grades, and mono-ethylene glycol (MEG), with polyethylene shipments rising eleven percent year-on-year in 2024, driven almost entirely by higher volumes destined for China. China alone imported over five million tonnes of methanol from Iran in 2024, along with approximately eight million tonnes of Iranian LPG — propane and butane — making it acutely exposed to any interruption in those supplies. These are not marginal quantities. They are the raw materials from which packaging film, pipe, fibre, and countless manufactured goods are made — the unglamorous but indispensable feedstocks of industrial civilisation.

China was by far Iran's largest polyethylene customer in 2024, accounting for over sixty-three percent of Iran's HDPE exports by value and nearly seventy-eight percent of its LDPE exports. The concentration is striking, and strategically significant in both directions. Iran is structurally dependent on Chinese demand to absorb its polymer output; China, for its part, receives Iranian polymers at prices no Western-aligned supplier can match, because Iranian producers — cut off from international capital markets, priced in yuan, and indifferent to Western compliance frameworks — have no alternative but to sell at a discount.

“Iranian polyethylene has become the quiet subsidy underpinning China's plastics conversion industry. When you strip out the Iranian volumes, the landed cost economics for a mid-sized converter in Guangdong look very different. It is not a marginal input — it is structural.”

— A Singapore-based petrochemical market analyst covering Asian polymer trade flows

This is the economic logic of the corridor rendered in molecular terms: Iran converts its hydrocarbons into progressively more refined products — crude to naphtha, naphtha to ethylene, ethylene to polyethylene — and moves them east along a route that Western enforcement mechanisms cannot easily reach. China receives discounted feedstocks and finished polymers that reduce its input costs across the entire downstream manufacturing chain. The arrangement is mutually reinforcing, self-deepening, and, crucially, structured to be resilient against external disruption.

The limits are real. Bulk crude oil — the lifeblood of the relationship — still moves overwhelmingly by sea, because rail capacity remains limited compared to tanker shipments, and the economics of moving large volumes overland cannot yet compete with maritime scale. What the corridor enables, for now, is the movement of lighter, higher-value products: condensates, naphtha, LPG, polymers in bagged or containerised form — products where volume is manageable and value per tonne justifies the freight premium.

This is not nothing. On the contrary, it is precisely the part of the hydrocarbon value chain where Iran has the most to gain: value-added processing rather than raw commodity export, captured margin rather than discounted crude. The strategic implication is that the corridor is not merely a conduit for existing trade flows. It is an incentive structure that rewards Iran for investing in downstream petrochemical capacity — and Beijing, through its $400 billion, 25-year cooperation agreement signed in 2021, has committed to providing the capital to build it. Iran holds the second-largest natural gas reserves in the world and the fourth-largest crude oil reserves, and has invested heavily in domestic processing capacity, with major petrochemical hubs at Assaluyeh and Bandar Imam already producing ethylene polymers, methanol, MEG, and LPG at significant scale. Every new cracker deepens Iran's integration into the Chinese supply chain and widens the range of products that can move profitably by rail — shifting the balance, molecule by molecule, away from the maritime dependency that Western sanctions were designed to exploit.

III. THE QUIET EROSION

There is a financial dimension to this story that resists the drama that analysts and policymakers tend to prefer.

Trade along the Xi'an–Tehran axis is increasingly settled in yuan or arranged through barter-adjacent structures: energy exchanged for machinery, raw commodities for built infrastructure. This is not, in any serious sense, a challenger to the dollar system — not yet, perhaps not ever at scale. But it is a parallel mechanism, and parallel mechanisms have a habit of maturing quietly, accumulating relevance at the margins until the margins become the mainstream.

The institutions that give the dollar its coercive utility — SWIFT, correspondent banking, the network of financial compliance that underpins Western sanctions architecture — depend for their power on universality. Since 2012, China has been purchasing Iranian oil primarily in yuan. China's Cross-Border Interbank Payment System (CIPS) processed RMB 175.49 trillion in cross-border yuan payments in 2024, a jump of 42.6 percent from the prior year, and is being integrated into Belt and Road trade flows as a functional alternative to SWIFT. What emerges is not a rival system so much as a fragmented topology: less efficient than the integrated global financial order, certainly, but significantly more resistant to disruption from outside.

Western policymakers have tended to underestimate this dynamic, partly because it lacks spectacle, and partly because economists are right that fragmentation carries genuine costs. There is no dramatic announcement, no singular rupture — just a slow, patient migration of trade flows into channels designed for resilience rather than efficiency. The danger is in mistaking the absence of crisis for the absence of change.

IV. THE LATTICE

The deeper story is not China and Iran. It is the system forming around them.

Corridors linking Central Asia to Iran intersect with routes binding Iran to Pakistan; those routes begin to rhyme with Russia's emerging southern trade arteries, diverted and deepened by the pressures of European sanctions after 2022. What is taking shape is not a single corridor but a lattice — redundant, multi-directional, politically buffered against external interference at any single node. A network, unlike a line, does not break when cut. It routes around the cut.

“Two years ago we were moving a handful of containers a month between Turkmenistan and the Iranian border. Now the scheduling is weekly, the volumes have tripled, and we have enquiries we cannot yet handle. The cargo mix has shifted too — more bagged resins, more chemicals, less general freight. The corridor is becoming a petrochemical artery and nobody in the West seems to be paying attention to that.”

— A logistics operations director based in Ashgabat, managing trans-Caspian freight services

This is Eurasia rediscovering its historical default. Before the age of sail concentrated power at sea, the great Eurasian land routes — the Silk Roads in their many iterations — sustained civilisations and empires for millennia. The shift to maritime dominance was not natural; it was technological. Technology, it turns out, can shift again.

The consequences for Western strategy are uncomfortable to articulate, and therefore often go unarticulated. Maritime dominance remains overwhelming; the U.S. Navy is not being challenged, and will not be challenged in any conventional sense for the foreseeable future. But dominance in one domain becomes less decisive when the flows that matter can increasingly bypass that domain. Sanctions lose their immediacy when the target has alternative arteries. Deterrence loses its grip when the chokehold has been partially released.

V. THE LIMITS OF THE FORTRESS

The idea of a sanctions-proof "Iron Fortress" deserves honest interrogation, and its architects would be the first to acknowledge its limits — at least privately.

Rail corridors are not invulnerable. They are simply vulnerable in different ways: to political instability in transit states, to capacity ceilings, to the sobering economics of overland freight in a world where container shipping retains spectacular advantages of scale. The Central Asian states through which these corridors pass are not monolithic; they are sovereign actors with their own interests, their own relationships with Western institutions, and their own histories of volatility. Dependence has not been eliminated — it has been redistributed, and the new dependencies carry their own risks.

The economics matter too. For hydrocarbons specifically, the constraints are acute: bulk crude and large-volume liquid feedstocks remain the province of the tanker, not the tank wagon. The rail corridor handles containerisable products — bagged polymers, drums of methanol, cylinders of LPG — where volumes per shipment are modest relative to a Very Large Crude Carrier. The corridor economy will remain, for the foreseeable future, complementary rather than competitive with global maritime trade.

None of which is to dismiss what has been built. The point is not that Beijing has constructed an impregnable alternative to the existing order. The point is that it has constructed an option — and in geopolitics, optionality is itself a form of power.

VI. A LONGER GAME

What the Xi'an–Tehran corridor ultimately represents is a wager on the shape of the coming world.

The wager is this: that in a fractured, multipolar order — one where no single power can sustain the cooperative consensus that underwrote postwar globalisation — the decisive advantage will belong not to the actor with the most dominant position in any single domain, but to the actor with the most redundant, most resilient, most politically diversified network of connections. Control, in this vision, is less about projection and more about ensuring that no adversary can, at a critical moment, simply turn the lights off.

Washington, for its part, continues to invest in maritime deterrence — in the South China Sea, in the Gulf, in the Indo-Pacific architecture of alliances and access agreements. These are not wasted investments; the sea remains the spine of global commerce, and will remain so for decades. But the competition has acquired a second board, and on that board the contest is not fleet versus fleet. It is system versus system.

The trains leaving Xi'an carry electronics, machinery, and consumer goods. They return with crude, naphtha, liquefied gas, methanol, and polyethylene — the molecular raw material of modern industry, flowing east along a route that bypasses every chokepoint, every compliance desk, and every enforcement mechanism that Western sanctions architecture depends upon. The exchange is ancient in its logic, modern in its routing, and deliberate in its design. Corridor by corridor, molecule by molecule, the centre of gravity shifts — not dramatically, not irreversibly, but with the quiet, compounding persistence of the structurally intentional.

Beijing, on that particular timetable, is running ahead of schedule.

ABOUT THE AUTHOR

Professor Dr. Sajjid Mitha is CEO and Founder of Polymerupdate, a leading intelligence platform covering the global polymers and petrochemicals industry. He writes at the intersection of commodity markets, geopolitics, and global supply chain strategy.

SOURCES & REFERENCES The following sources informed the research and factual claims contained in this article. 1. BusinessToday. "Beyond Strait of Hormuz: How China Iran rail system countered US threat." March 3, 2026. businesstoday.in * All market data, volume figures, and trade statistics reflect information available as of the date of publication. Readers should verify figures against primary sources before use in commercial or regulatory contexts. |