Click the icon to add a specified price to your Dashboard list. This makes it easy to keep track on the prices that matter most to you.

The world’s fastest-growing major economy is attempting a feat with no modern precedent — an industrial, digital, and demographic transformation simultaneously, at continental scale. Whether it succeeds will determine the shape of the global economy through mid-century.

| By Professor Dr. Sajjid Mitha CEO & Founder, Polymerupdate · Polymerupdate Academy · RACE Expos and Conferences |

India currently navigates a rare “Goldilocks” moment in modern economic history. While the G7 confronts secular stagnation and China wrestles with a structural middle-income trap compounded by demographic inversion, India has emerged as the primary engine of global marginal growth. Having recently surpassed Japan to become the world’s fourth-largest economy by nominal GDP, the country is no longer merely an emerging market. It is a continental economy undergoing a sophisticated, multi-dimensional structural pivot — and the world’s institutional investors are taking note.

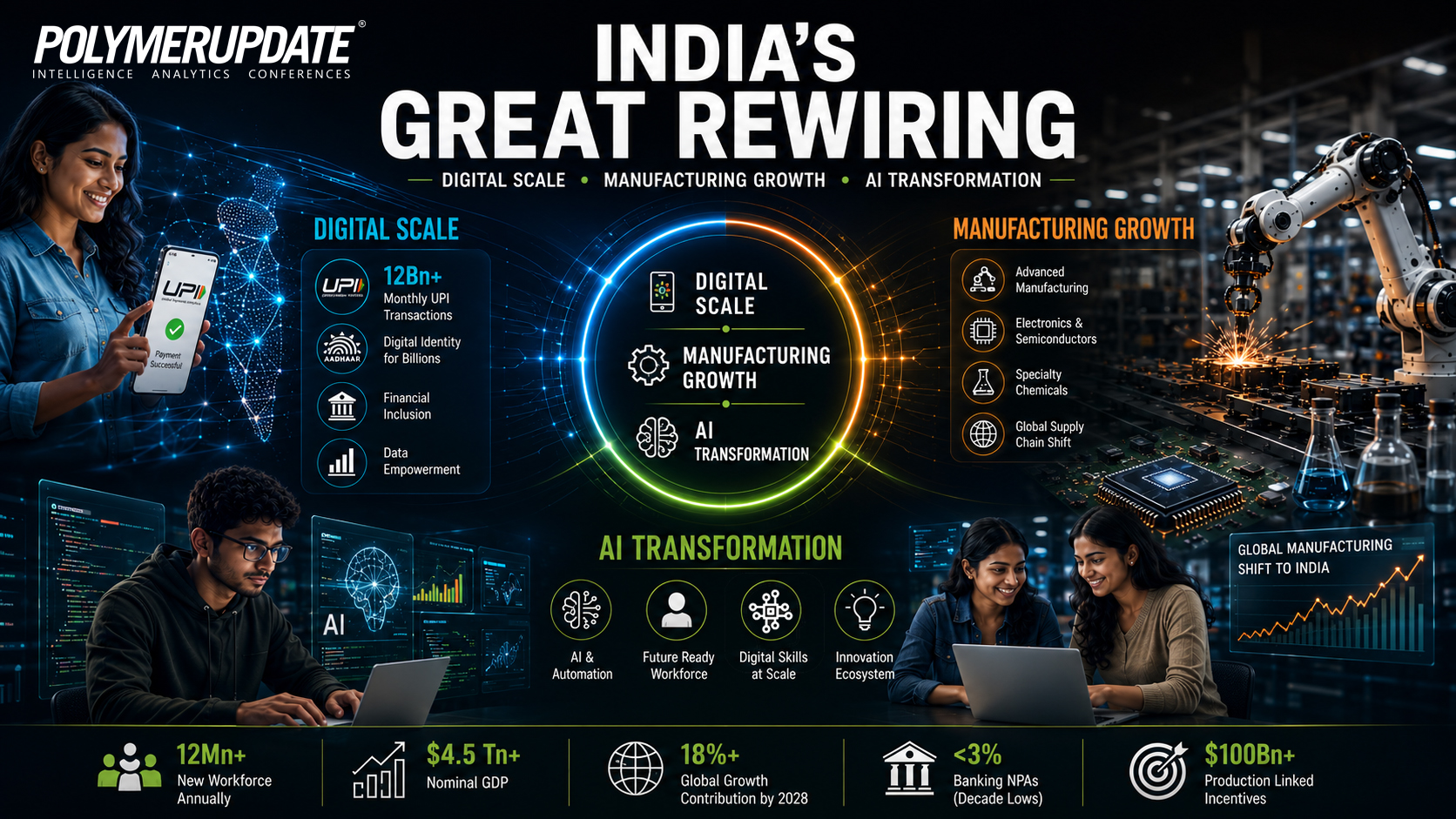

The macroeconomic architecture is formidable. With nominal GDP exceeding $4.5 trillion and a contribution to global growth projected to surpass 18% by 2028, the optimism embedded in India’s current valuations is not simply narrative. It is grounded in a fundamental resolution of the “Twin Balance Sheet” crisis that had paralysed private capital formation since roughly 2012. Banking sector non-performing assets (NPAs) have fallen below 3% — decade lows — unlocking the credit depth that a genuine private capital expenditure cycle requires..

18%+ | <3% | 12bn+ |

The Digital Public Goods Arbitrage

What separates the current Indian trajectory from the “Tiger Economies” of the 1990s is its systematic leapfrogging of traditional institutional layers through Digital Public Infrastructure — the so-called India Stack. The Unified Payments Interface (UPI) now processes over 12 billion transactions monthly, effectively formalising large swaths of the shadow economy and generating a transaction data layer that is, analytically speaking, extraordinarily valuable for credit underwriting and fiscal targeting alike.

The fiscal dividend is equally significant. The Direct Benefit Transfer (DBT) mechanism has saved the exchequer an estimated $35 billion in subsidy leakages — a sum that, redirected toward capital formation, has materially altered the quality of government spending. The World Bank and IMF have both cited India’s DPI architecture as a blueprint for developing economies seeking to compress institutional development timelines.

What India has built with UPI and Aadhaar is not merely a payments system — it is a formalisation machine. Every transaction that moves from cash to digital creates a data trail, a credit profile, a tax record. The compounding effect of that over a decade is genuinely transformational for fiscal capacity and private credit markets alike. No other country at this income level has done this at this scale.

— Senior Economist, Multilateral Development Bank — speaking on condition of anonymity

Yet the digital layer, however impressive, is infrastructure rather than output. The harder question is whether it accelerates the structural transformation of the real economy — the shift of labour from low-productivity agriculture into higher-productivity manufacturing and services — at the pace that 12 million new annual labour-force entrants demand.

The Manufacturing Paradox

For a decade, the “Make in India” initiative and its successor, the Production Linked Incentive (PLI) scheme, have sought to reposition India within the global supply chain. The geopolitical tailwind is real: the “China Plus One” strategy has driven meaningful capital commitments from Apple suppliers, semiconductor firms, and specialty chemical producers. Freight-cost normalisation post-pandemic and the US-China decoupling narrative have both served India’s interests.

The institutional data, however, demands a more measured reading. Manufacturing’s share of GDP has hovered stubbornly between 13% and 17% for two decades — a range India has been unable to escape despite considerable policy effort. The PLI scheme, backed by approximately $23 billion in incentives across 14 sectors, generated production worth 14 trillion rupees against a target of 15.52 trillion by November 2024. Reuters reported in early 2025 that the government was considering allowing the scheme to lapse given results below initial projections.

Manufacturing’s share of GDP has hovered stubbornly between 13–17% for two decades. India has been unable to escape that range despite considerable policy effort and capital.

The hurdles are structural and well-documented. Despite the Gati Shakti masterplan reducing logistics costs from approximately 14% to 9% of GDP — a genuine and under-celebrated achievement — Factor Market reforms remain the unresolved constraint. Land acquisition processes and labour market flexibility, both politically sensitive and unevenly implemented across states, continue to deter the large-scale greenfield industrial investment that would transform the employment profile.

The competitive context sharpens the urgency. Vietnam’s industry sector employs roughly 35% of its workforce; India’s is approximately 25%. Bangladesh and Vietnam have both outpaced India in low-cost, labour-intensive manufacturing export categories — the very segments where India’s labour cost advantage should, in theory, be decisive.

The PLI scheme was well-designed in concept — output-linked, time-bound, cross-sector. But it ran into the same wall every Indian industrial policy runs into: you can subsidise production, but you cannot subsidise away bad land laws or a court system that takes fifteen years to resolve a commercial dispute. Until those foundational issues are addressed, the manufacturing gap versus Vietnam and Bangladesh will persist regardless of the incentive architecture.

— Managing Director, Asia-Pacific Infrastructure Fund — speaking on condition of anonymity

The path forward likely involves a sharper sectoral concentration — doubling down on areas where India’s factor endowments provide genuine comparative advantage: specialty chemicals, advanced pharmaceuticals, defence electronics, and precision engineering. Broad-based low-cost assembly, the route China took, may no longer be available given the pace at which automation compresses the labour cost advantage.

The Labour Inflection Point: From Man-Hours to Machine Intelligence

The defining economic challenge of India’s next decade is not GDP growth — that is likely to remain robust by any comparative standard. It is labour absorption: whether the economy can generate sufficient high-quality, formal employment to productively integrate the 8 to 10 million Indians who enter the working-age population each year. GDP growth is, ultimately, a vanity metric if it does not translate into rising real wages and expanding formal employment at scale.

This challenge has been materially complicated by the arrival of Generative AI. India’s $282 billion IT services sector — which employs approximately 5.4 to 6 million workers directly and has been the primary generator of urban middle-class prosperity since the late 1990s — is facing its most significant structural test since Y2K created the offshoring opportunity.

NASSCOM, the industry body, has acknowledged that “workforce rationalization is expected in the near term” as AI reshapes service delivery. The data is already manifest in hiring patterns: Tata Consultancy Services announced layoffs of 12,000 employees in 2025; Infosys, Wipro, and others have adopted AI-first strategies that, in their own communications, target 20–30% reductions in headcount for repetitive task categories. NASSCOM’s own modelling projects that over 1.5 million IT roles will be significantly transformed within two years.

The billing model that built India’s IT sector — linear man-hours sold at a dollar-per-hour discount to Western counterparts — is structurally impaired by AI. A tool that writes boilerplate code, handles L1 support queries, and processes data entry at near-zero marginal cost removes the arbitrage that justified the model. The question is not whether the sector adapts — it will — but how fast, and whether the 2 to 3 million workers in the most exposed roles can reskill at a pace the market requires. The honest answer is that the reskilling infrastructure does not yet exist at the scale needed.

— Head of Technology Equity Research, Tier-1 Investment Bank — speaking on condition of anonymity

The optimistic case is not without foundation. India’s AI talent pool is growing at approximately 15% compounded annually; NASSCOM and NITI Aayog project a doubling of AI professionals to 1.25 million by 2027. India recorded close to 100% year-on-year growth in prompt-engineering talent in 2025 and a 30% AI engineering hiring rate that places it ahead of several advanced economies. The government’s FutureSkills PRIME platform had enrolled over 18.56 lakh candidates as of August 2025.

The issue is distributional. The graduates best positioned to capture AI-era opportunities are those from elite institutions with deep quantitative and software engineering foundations. The several million workers in tier-2 and tier-3 city business process centres — handling L1 support, data annotation, and routine back-office functions — face the steepest displacement risk and the longest reskilling pathway. This is, structurally, the same bifurcation that has characterised every major technology transition: the gains accrue rapidly at the top of the skill distribution; the losses are concentrated at the bottom.

Nations do not become superpowers through isolated islands of excellence. They succeed when the broad-based median skill level rises.

The K-Shaped Divide: Progress and Concentration

From a developmental standpoint, India presents the analyst with a genuinely complex portrait. On one reading, the poverty reduction achieved over the past decade is among the most significant in modern economic history — 171 million Indians lifted out of extreme poverty, the World Bank confirms, with the share living below $2.15 per day falling from 16.2% in 2011–12 to 2.3% in 2022–23. Aadhaar-linked direct transfers, expanding financial inclusion through Jan Dhan, and Ayushman Bharat health coverage together represent a genuine expansion of the social contract.

On another reading, the concentration of wealth at the apex of the income distribution is historically unprecedented. Research by the World Inequality Lab, drawing on income tax records and Forbes billionaire data to supplement household surveys, finds that the top 1% of Indians control approximately 40% of national wealth and capture around 22.6% of national income — levels higher than South Africa, Brazil, or the United States on this measure. The total net wealth of Indian dollar-billionaires as a share of net national income rose from under 1% in 1991 to 25% in 2022.

Agricultural distress adds a further dimension. NCRB data confirms that 10,786 farmers and agricultural labourers died by suicide in 2023 — approximately one per day — concentrated in Maharashtra and Karnataka. Agriculture still employs a disproportionate share of the workforce relative to its contribution to output. Modernising this sector through agri-tech integration and supply-chain efficiency is not merely a social imperative; it is a macroeconomic necessity. A rural economy under structural stress is a domestic consumption engine running below capacity.

The apparent contradiction between the poverty and inequality data is largely methodological: the government’s Gini index is consumption-based, which compresses apparent dispersion; income-based measures from the World Inequality Lab tell a sharper story. Both can be simultaneously accurate. India has genuinely reduced absolute deprivation while concentrating income and wealth at the top at an accelerating pace. That is the definition of K-shaped growth, and it is the defining political-economic tension of the decade ahead.

The Sovereign Transition: Momentum Versus Institutional Friction

It would be analytically mistaken — and commercially imprudent — to view India through a lens of dysfunction. On the contrary, India is one of the very few major economies attempting simultaneous transformation across manufacturing depth, digital infrastructure, energy transition, and logistics modernisation, all while maintaining democratic continuity and macroeconomic stability. That combination is rarer than the investment community perhaps appreciates.

Expressway construction is proceeding at speeds that would have seemed implausible a decade ago. Renewable energy capacity is scaling rapidly. The specialty chemicals and advanced polymers sector is absorbing supply chain relocation from China with genuine competitiveness. Defence electronics and semiconductor assembly are nascent but credible. The Gati Shakti logistics masterplan has produced measurable cost reductions. These are not narrative; they are operational.

What distinguishes India’s current moment from prior cycles of optimism — the 2003–2008 boom, the 2014 election premium — is the underlying credit cycle. Clean bank balance sheets, recovering private capital expenditure intentions, and a credit-to-GDP ratio with meaningful headroom collectively suggest that the investment cycle beginning now has more structural durability than its predecessors.

The risks are also structural rather than cyclical. Land and labour reform remain politically constrained. The judicial backlog — tens of millions of pending commercial cases — is a friction cost embedded in every cross-border investment decision. The AI-driven disruption of IT services employment, if inadequately managed, risks compressing urban consumption precisely when domestic demand needs to be the growth anchor. And the demographic dividend, the most celebrated feature of the India thesis, is time-limited: the window of favourable age structure begins narrowing materially by the mid-2030s.

The world is no longer asking whether India will matter. It already does. The question is whether India can convert extraordinary potential into broad-based prosperity at the scale its century demands.

The transition from a large economy to a transformative global power will require more than headline growth rates. It will require what institutional economists call “last-mile reform”: the politically costly, technically unglamorous work of land courts that function, labour contracts that are enforceable, skill systems that reach tier-3 cities, and agricultural markets that price risk rather than socialize it. India’s trajectory over the next ten years will be determined less by its macroeconomic potential — which is not seriously in dispute — and more by the political will to pursue the structural agenda that potential demands.

Professor Dr. Sajjid Mitha is the CEO and Founder of Polymerupdate, Polymerupdate Academy, and RACE Expos and Conferences.

| DISCLOSURES & EDITORIAL NOTES Expert quotations represent the views of individuals speaking anonymously in their professional capacity. No compensation was received by quoted individuals. All statistical references are sourced from primary institutional data: IMF World Economic Outlook, World Bank Development Indicators, RBI Annual Report 2024–25, NASSCOM AI Economy Roadmap (NITI Aayog, 2025), World Inequality Lab Working Paper 2024, NCRB Accidental Deaths & Suicides in India 2023, NPCI transaction data, and PIB press releases. Manufacturing share data drawn from CNBC / World Bank (March 2025) and Ideas for India institutional analysis (March 2026). This report is intended for professional and institutional investors. It does not constitute investment advice. Past performance is not indicative of future results. © 2026. All rights reserved. |