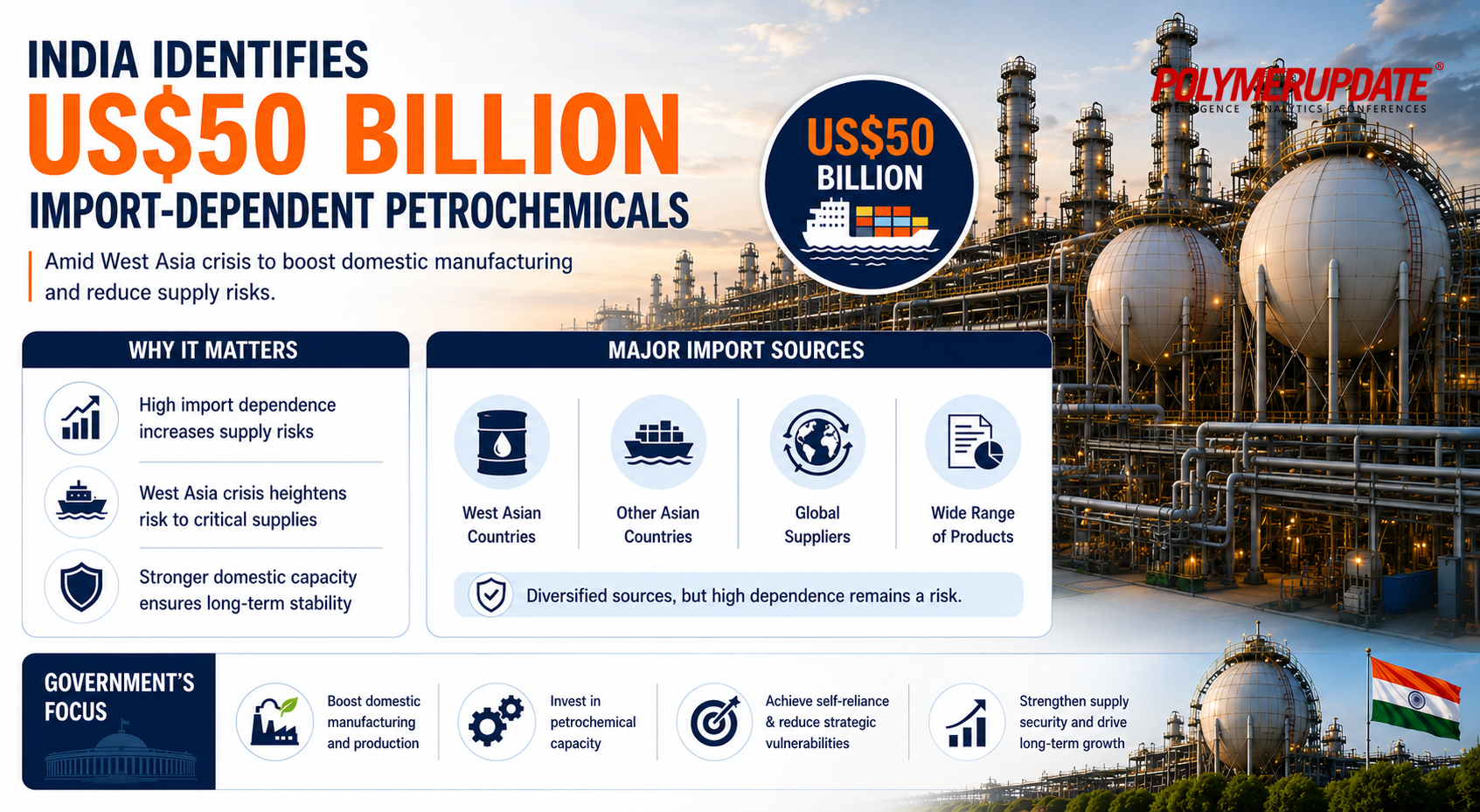

India has intensified efforts to strengthen domestic petrochemical manufacturing by identifying nearly US$ 50 billion worth of petrochemical products that are currently fully dependent on imports, as the country grapples with severe supply disruptions caused by the ongoing West Asia crisis and geopolitical instability in the Strait of Hormuz. The key objective of these efforts is to restrict the foreign currency (forex) outgo and protect the Industry downstream industries from price volatility, stemming from supply disruptions.

The Department for Promotion of Industry and Internal Trade (DPIIT) has identified around 200 petrochemical products where India remains heavily import reliant and has sought an urgent response from industry stakeholders regarding the feasibility of establishing indigenous production capacities. The move is aimed at reducing dependence on overseas suppliers, conserving valuable foreign exchange reserves, and improving supply-chain resilience during a period of heightened global uncertainty.

According to industry sources, DPIIT held a high-level meeting with leading petrochemical manufacturers last week and asked them to assess the technological, financial, and infrastructural requirements needed to manufacture these import-dependent products within the country. The initiative forms part of the government’s broader strategy to enhance self-reliance in critical industrial raw materials and shield downstream industries from volatile global supply conditions.

Supply disruptions

Supply disruptionsThe urgency behind the move has intensified following the prolonged crisis in West Asia, which has severely disrupted global energy and petrochemical trade flows. The conflict, which escalated after the US-Israel drone and missile strikes on Iran on February 28 that reportedly killed Iranian Supreme Leader Ayatollah Ali Khamenei, triggered widespread retaliatory actions from Tehran across the Gulf region.

Subsequently, Iran’s Islamic Revolutionary Guard Corps (IRGC) tightened control over the Strait of Hormuz, one of the world’s most critical maritime trade routes for crude oil, liquefied natural gas, and petrochemical shipments. Reports of oil tankers and merchandise vessels being detained in the Hormuz region led to significant disruptions in global trade flows and caused sharp spikes in energy and petrochemical prices.

India, which imports a substantial portion of its crude oil and petrochemical requirements from the Middle East, has emerged as one of the major economies vulnerable to these disruptions. Delays in shipments, rising freight costs, insurance premiums, and supply shortages have already begun affecting several downstream manufacturing industries.

Products under scannerThe petrochemical products identified by DPIIT largely comprise intermediate raw materials that are extensively used across key sectors such as packaging, construction, automotive, agriculture, textiles, healthcare, paints, and consumer goods manufacturing. Among the major import-dependent polymers listed are polyvinyl chloride (PVC), low-density polyethylene (LDPE), linear low-density polyethylene (LLDPE), polypropylene (PP), polystyrene (PS), and Acrylonitrile Butadiene Styrene (ABS). These materials are critical inputs for the production of packaging films, pipes, fittings, automotive parts, household appliances, storage containers, and a wide range of consumer products.

Any disruption in the supply of these raw materials directly impacts the cost structure of several industries, particularly fast-moving consumer goods (FMCG), infrastructure, construction, e-commerce packaging, and automobile manufacturing. Market participants said that persistent volatility in raw material availability has already started exerting inflationary pressure on multiple industrial supply chains.

Apart from polymers, the list also includes high-value industrial chemicals such as phosphoric acid, ammonia, acetic acid, and toluene, which are extensively used in agriculture, fertilizers, food processing, pharmaceuticals, paints, coatings, and industrial manufacturing applications. In addition, engineering plastics and specialty resins such as polycarbonates and propylene copolymers — widely used in medical devices, automotive components, electronics, and advanced packaging materials — continue to witness strong import dependence due to limited domestic manufacturing capacities.

Focus on domestic investmentIndustry experts believe the government’s initiative could open up massive investment opportunities across India’s petrochemical value chain, especially at a time when global companies are seeking supply-chain diversification outside traditional manufacturing hubs. India’s petrochemical demand has been expanding steadily over the last decade, driven by rapid urbanisation, rising disposable incomes, infrastructure expansion, increasing consumption of packaged goods, and growth in sectors such as automobiles, healthcare, renewable energy, and electronics manufacturing.

However, domestic production capacities for several specialised petrochemical products have not kept pace with the rising demand, resulting in widening import dependence. According to industry estimates, India’s per capita polymer consumption still remains significantly lower than the global average, indicating substantial long-term growth potential for the domestic petrochemical industry. The government believes that enhancing local manufacturing could not only reduce import bills but also help position India as a competitive global manufacturing hub for petrochemicals and specialty chemicals.

However, industry participants caution that setting up domestic capacities for several of these products would require substantial capital investments, advanced technologies, feedstock availability, environmental clearances, and long gestation periods. Petrochemical projects are highly capital intensive and often require integrated refinery and cracker infrastructure to remain globally competitive.

HeadwindsExperts also pointed out that feedstock security remains a major challenge for India, especially given its dependence on imported crude oil and liquefied natural gas. Any large-scale expansion in petrochemical manufacturing would therefore require long-term policy support, infrastructure development, competitive energy pricing, and stable regulatory frameworks. Nevertheless, the current geopolitical disruptions have reinforced the importance of supply-chain localisation and strategic industrial self-reliance. Policymakers increasingly view petrochemicals as a critical sector due to their widespread linkages with manufacturing, infrastructure, agriculture, healthcare, and consumer industries.

With global trade uncertainties likely to persist and geopolitical tensions continuing to impact maritime trade routes, India’s push toward domestic petrochemical manufacturing is expected to gain further momentum in the coming months. Industry stakeholders now await additional policy incentives, fiscal support measures, and investment frameworks that could accelerate the development of local capacities and reduce the country’s vulnerability to external supply shocks.

Impact on Indian petrochemical industryThe ongoing West Asia crisis has emerged as a major threat to India’s petrochemical industry, particularly due to prolonged disruptions in the Strait of Hormuz — one of the world’s most critical maritime routes for crude oil, liquefied natural gas, and petrochemical trade. Escalating tensions between Iran, the United States, and Israel have severely impacted the movement of cargo vessels and energy shipments across the Gulf region, resulting in sharp spikes in freight costs, insurance premiums, and feedstock prices.

Since India imports a substantial portion of its crude oil, liquefied petroleum gas (LPG), and petrochemical raw materials from the Middle East, the disruption has tightened domestic supply availability and pushed up prices of key polymers and industrial chemicals such as polypropylene (PP), polyvinyl chloride (PVC), polyethylene (PE), ammonia, methanol, and phosphoric acid. The supply uncertainty has started affecting downstream sectors including packaging, automotive, construction, textiles, paints, pharmaceuticals, and fast-moving consumer goods (FMCG), thereby increasing inflationary pressure across industrial value chains.

Forex reserves trendIndia's forex reserves currently stand at approximately US$ 688.9 billion. While this is a slight dip from their all-time high of over US$ 730 billion, the overarching trend is a massive accumulation over recent years. This robust war chest provides a comfortable import cover of about 8 to 11 months. Reserves have seen modest contractions recently (dropping roughly US$ 8 billion in late May). This is primarily due to the Reserve Bank of India (RBI) actively selling dollars in the forex market to shield the Indian Rupee from geopolitical-driven volatility and higher crude oil prices.

Over the past few years, the baseline trend has been upward. Rising to over US$ 700 billion earlier in the year, this expansion reflects strong macroeconomic fundamentals, resilient Foreign Direct Investment (FDI), and steady capital inflows into Indian markets. The reserves primarily consist of Foreign Currency Assets (FCA), a growing stockpile of gold, Special Drawing Rights (SDRs), and a reserve position in the International Monetary Fund (IMF).

DILIP KUMAR JHA

Editor

dilip.jha@polymerupdate.com