This week, Low density polyethylene prices climbed in the Asian region.

An industry source in Asia wishing to remain unidentified informed a Polymerupdate team member, “Energy prices have trended higher with the Organization of Petroleum Exporting Countries (OPEC) up revising its oil energy demand forecast for 2024 and 2025. Meanwhile, container space constraints have led to a spike in ocean freight rates over the last few weeks.”

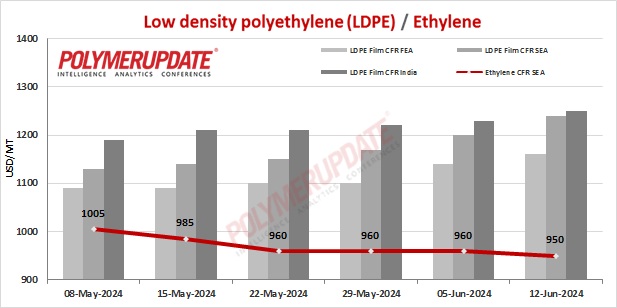

In Far East Asia, LDPE film grade prices were assessed at the USD 1120-1160/mt CFR levels, an increase of USD (+20/mt) from the previous week.

In China, Middle Eastern producers have offered their LDPE film grades in the range of USD 1120-1160/mt CFR levels for shipment in end June/early July 2024.

In China, import prices were largely assessed on the basis of deals and offers during the current week. Offers to China were limited as suppliers rerouted their cargoes to other markets in Asia in hopes of higher netbacks. Low density polyethylene (LDPE) enquiries remained healthy on the back of high domestic prices.

In Southeast Asia, LDPE film grade prices were assessed at the USD 1190-1240/mt CFR levels, a week on week steep rise of USD (+40/mt).

In Vietnam, a Saudi Arabian producer has offered its LDPE film grade at the USD 1240/mt CFR levels for shipment in end June 2024. A producer from the Middle East has offered its LDPE film grade at the USD 1190/mt CFR levels for shipment in end June/early July 2024.

In Southeast Asia, local converters and distributors in the key market of Vietnam resorted to replenishing material in bulk quantities over the past two weeks owing to an unanticipated tightening of LDPE supplies. Market participants opined that shipments of LDPE import cargoes could be delayed by a further 2-3 weeks owing to severe vessel congestion at the Singapore transshipment port in May. The congestion, which is expected to last through June, is likely to exacerbate the short supply situation of LDPE material in Vietnam. Hence, LDPE material could attract a premium in Vietnam with regional plants likely to hike their LDPE offers.

In Indonesia, trading activity was muted with buyers staying away from the market ahead of the Eid al-Adha festival.

In India, LDPE prices were assessed at the USD 1220-1250/mt CFR levels, up USD (+20/mt) from last week. The overall LDPE sentiment in the domestic market is bullish owing to ongoing high freight rates stemming from vessel congestion which has driven local producers to defer from announcing fresh incentive schemes.

In India, Middle Eastern producers have offered their LDPE film grades in the range of USD 1220-1250/mt CFR levels for shipment in end June/early July 2024.

A domestic industry source informed a Polymerupdate team member, “Most market participants remained concerned over an ensuing short supply situation as a South Korean petrochemical producer notified Indian domestic customers that orders placed for Polyvinyl chloride, Ethylene vinyl acetate and LDPE in May for June/July shipment would be cancelled. Spikes in ocean rates and vessel space crunch were cited as reasons for the cancellation. The announcement has distressed Indian buyers, many of whom have opened Letters of Credit (LCs) to acquire funds for buying material. The South Korean producer further indicated that other South Korean producers could be struggling with high freight rates and vessel shortages, though announcements to the effect have not been made by them.

In Pakistan, LDPE prices were assessed at the USD 1170-1200/mt CFR levels, a week on week increase of USD (+10/mt).

In Pakistan, overseas suppliers have offered their LDPE film grades in the range of USD 1170-1200/mt CFR levels for shipment in end June / early July 2024.

In Sri Lanka, LDPE prices were assessed at the USD 1220-1260/mt CFR levels, a rise of USD (+20/mt) from last week.

In Sri Lanka, overseas producers have offered their LDPE film grades in the range of USD 1220-1260/mt CFR levels for shipment in end June / early July 2024.

In Bangladesh, LDPE prices were assessed at the USD 1230-1250/mt CFR levels, a week on week rise of USD (+30/mt).

In Bangladesh, overseas suppliers have offered their LDPE film grades in the range of USD 1230-1250/mt CFR levels for shipment in end June / early July 2024.

In Pakistan, Sri Lanka and Bangladesh, activity was limited owing to vessel space shortage and high freight rates. Most of the buyers also remained away from the markets ahead of the Eid al-Adha festival.

In feedstock news, CFR South East Asia ethylene prices were assessed at the USD 940-950/mt levels, a fall of USD (-10/mt) from the previous week. CFR North East Asia feedstock ethylene prices were assessed at the USD 830-840/mt levels, a week on week drop of USD (-20/mt).

In plant news, Zhejiang Petroleum & Chemical (ZPC) has been running its No.2 Low density polyethylene (LDPE) unit at curtailed capacity levels. The reason behind the lower operational runs could not be ascertained. Located in Zhoushan, Zhejiang in China, the No.2 LDPE unit has a production capacity of 400,000 mt/year.

Shenhua Xinjiang Energy is likely to shut down its Low density polyethylene (LDPE) unit in July 2024. The exact date and duration of the shutdown could not be ascertained. Located in Xinjiang, China, the LDPE unit has a production capacity of 270,000 mt/year.