This week, PVC prices declined in the Asian region.

An industry source in Asia on condition of anonymity informed a Polymerupdate team member, “Lower import offers from a major overseas supplier and dull demand trends together pushed PVC prices lower in the Asian region.”

The source added, “Improved prospects of a Gaza ceasefire deal have led to crude oil prices trending lower on a day-on-day basis. Meanwhile, the U.S. Energy Information Administration has forecast a rise in demand for oil.”

In China, PVC prices were assessed at the USD 700-730/mt CFR levels, a week on week fall of USD (-10/-20/mt).

In China, a Taiwanese producer have offered PVC resin suspension grade at the USD 725/mt CFR levels, for shipment in February 2025.

In China, Chinese domestic PVC prices have maintained a steadily downward trend this week, with supply outpacing demand. Meanwhile, demand has been seasonally tepid, with production facilities likely to curtail their run rates in H2 January in the run-up to the Lunar New Year holidays. Export activity was steady in the week, with Indian buyers continuing to replenish material owing to the Bureau of Indian Standards (BIS) extending its quality control mandates on PVC imports from December 24, 2024 to June 24, 2025.

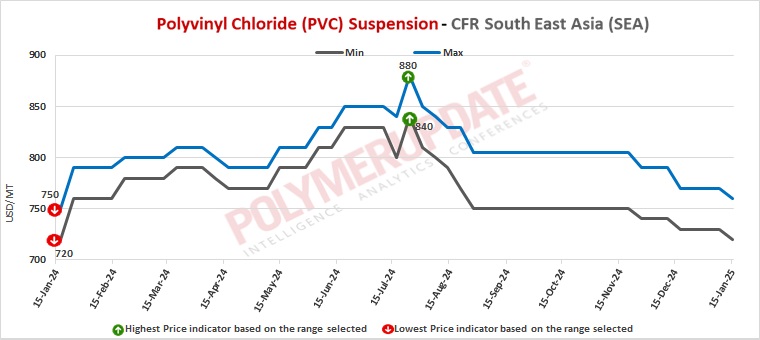

In Southeast Asia, PVC prices were assessed at the USD 720-760/mt CFR levels, a fall of USD (-10/mt) from the previous week.

In Vietnam, a producer from Taiwan have offered PVC resin suspension grade at the USD 750/mt CFR levels, for shipment in February 2025.

In Southeast Asia, PVC import prices dropped amid a supply glut situation with trading activity softening ahead of the approaching Lunar New Year holidays. Weak demand across key segments and converters holding excess supplies , with most having stocked up material already ahead of the Lunar New Year holidays, was the dominant theme in the southeast Asian markets. The month of January is likely to experience a seasonal muted demand sentiment, with participants likely to resume purchase activity from mid-February. Buying appetite for import cargoes further ebbed in the week with converters opting to wait prior to making further purchase commitments.

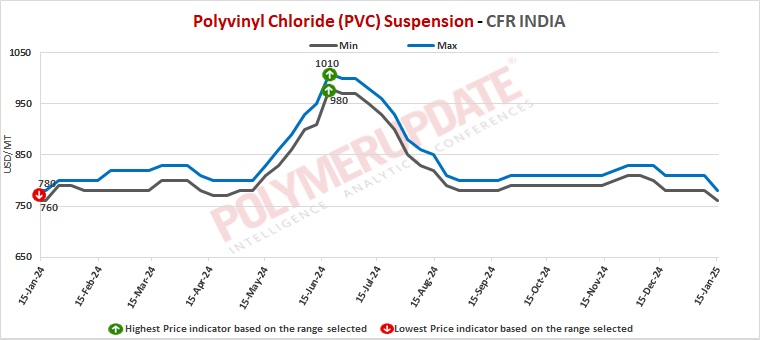

In India, PVC prices were assessed at the USD 760-780/mt CFR levels, lower by USD (-20/-30/mt) from last week.

In India, a major Taiwanese producer has offered its PVC suspension grades at the USD 760/mt levels while B57 grade is on offer at the USD 800/mt levels on CIF Nhava Sheva/Mundra/Chennai port basis for February & March 2025 shipment (LC at sight). These offers are lower by USD 25/mt from previous month’s offers. Add USD 30/mt for CIF Cochin/Kolkata/Pipavavi ports. For LC 90 days Add USD 10/mt.

In India, PVC import prices were lower this week amid no significant pickup seen in discussions. Despite the BIS extending quality control mandates on PVC imports from December 24, 2025 to June 24, 2025, purchase appetite for import cargoes has continued to be muted thus far in January. Although the advent of the Lunar New Year holidays in China usually incentivizes Indian buyers to replenish material with Chinese sellers stepping away from the market, inventories among Indian converters and traders are sufficient enough to see them through the holiday season. Meanwhile, participants are focused on the outcome of the follow-up hearing on anti-dumping duties (ADD) investigation on s-PVC imports, which expected to provide greater clarity on emerging market trends.

In Pakistan, PVC prices were assessed at the USD 780-800/mt CFR levels, a week on week decline of USD (-5/-10/mt).

In Pakistan, a producer from Indonesia has offered PVC resin suspension grade at the USD 800/mt CFR levels, for shipment in February 2025. A South Korean producer has offered PVC resin suspension grade at the USD 780/mt CFR levels, for shipment in February 2025.

In Pakistan, prices dropped owing to ample material availability and lower offers from suppliers.

In Sri Lanka, PVC prices were assessed at the USD 770-800/mt CFR levels, a fall of USD (-20/mt) from the previous week.

In Sri Lanka, overseas supplier have offered PVC resin suspension grade at the USD 770-800/mt CFR levels, for shipment in February 2025.

In Sri Lanka, prices declined on the back of weak demand sentiments. Meanwhile, market feedback pointed to lower offers surfacing from China in the region.

In Bangladesh, PVC prices were assessed at the USD 770-800/mt CFR levels, a week on week drop of USD (-10/mt).

In Bangladesh, a Taiwanese producer have offered PVC resin suspension grade at the USD 770/mt CFR levels, for shipment in February 2025.

In Bangladesh, PVC import discussions remain muted with minimal import offers emerging from usual sellers in Taiwan. Most converters have exhibited an unwillingness to purchase China-origin s-PVC cargoes.

Feedstock EDC prices were assessed at the USD 275-285/mt CFR China levels while CFR South East Asia EDC prices were assessed at the USD 275-285/mt levels, both rolled over from last week.

Feedstock CFR South East Asia VCM prices were assessed at the USD 550-560/mt level, a week on week steep drop of USD (-45/mt). CFR China VCM prices were assessed at the USD 505-515/mt levels, a fall of USD (-10/mt) from the previous week.

Feedstock ethylene prices on Tuesday were assessed flat at the USD 865-875/mt CFR North East Asia level. Meanwhile, CFR South East Asia ethylene prices were assessed at the USD 905-915/mt levels, a week on week decline of USD (-10/mt).

In plant news, Hanwha Solutions is likely to undertake a planned maintenance turnaround at its Polyvinyl chloride (PVC) unit on February 24, 2025. The unit is slated to remain offline until March 10, 2025. Located in Yeosu, South Korea, the unit has a production capacity of 480,000 mt/year.