Click the icon to add a specified price to your Dashboard list. This makes it easy to keep track on the prices that matter most to you.

This week, PVC prices were left unchanged across the Asian region.

An industry source in Asia, on condition of anonymity, informed a Polymerupdate team member, “Major Taiwanese producers held offer prices steady from their previous price levels. Meanwhile, buying sentiment continues to be weak in the region.” The source added, “The key drivers of global crude oil trading have recently experienced significant shifts. On the upside, U.S. sanctions on Iran and other oil producers, ongoing unrest in the Middle East, and a weakening U.S. dollar have the potential to exert a bullish pressure on oil prices. However, demand forecasts are being weighed down by US President Donald Trump’s tariff policies, while OPEC+ has only marginally increased production. Furthermore, the downgrading of economic growth projections by the International Monetary Fund (IMF) in its latest World Economic Outlook has added to an already uncertain global environment. As a result, oil prices are likely to face downward pressure.”

The source added, “The key drivers of global crude oil trading have recently experienced significant shifts. On the upside, U.S. sanctions on Iran and other oil producers, ongoing unrest in the Middle East, and a weakening U.S. dollar have the potential to exert a bullish pressure on oil prices. However, demand forecasts are being weighed down by US President Donald Trump’s tariff policies, while OPEC+ has only marginally increased production. Furthermore, the downgrading of economic growth projections by the International Monetary Fund (IMF) in its latest World Economic Outlook has added to an already uncertain global environment. As a result, oil prices are likely to face downward pressure.”

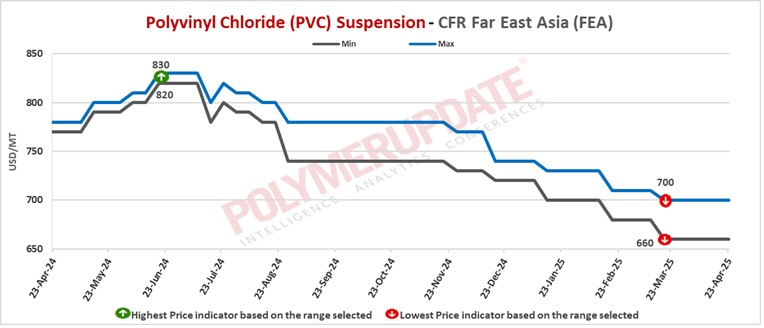

In China, PVC prices were assessed at the USD 660-700/mt CFR levels, constant from the previous week.

In China, a producer from Taiwan has offered its PVC resin suspension grade at the USD 700/mt levels for shipment in May 2025. Meanwhile, Chinese producers have offered PVC (ethylene-based) at the USD 630/mt levels and PVC (carbide based) is offered at the USD 610/mt levels on FOB basis.

In China, the PVC import market has remained subdued as participants awaited the May shipment offers from Taiwan, which have been reported as stable compared to the previous month. Regional spot trading has also weakened, as many market participants were busy attending the 37th International Exhibition on Plastics and Rubber Industries (Chinaplas) in Shenzhen, China, with the Songkran holidays in Thailand adding to the muted market sentiment.

Meanwhile, domestic PVC prices have largely remained stable this week, as tighter supply during the peak maintenance season has countered recent declines in PVC futures.

PVC futures have treaded a downward trajectory this week, with trading fluctuations narrowing compared to the previous week due to lacklustre trading activity. The majority of market participants were busy attending the Chinaplas conference last week, which restricted both export and domestic trading activities. Additionally, alleviating economic concerns regarding tariff issues have contributed to the decline in PVC futures.

In recent times, domestic macroeconomic sentiment has been poor, and the uncertainty surrounding foreign trade has dampened the short-term market outlook. However, in the long term, expectations of cuts to the domestic reserve requirement ratio and interest rates may provide ongoing support to the market. Currently, the fundamentals of PVC supply and demand remain weak. PVC production facilities are focusing on maintenance, leading to a decrease in production, while domestic demand remains stagnant, with foreign trade export deliveries being the primary source of goods. New orders have been cautiously reduced, and the pace of inventory reduction in the industry is anticipated to slow. Short-term cost support is weak, and the fundamentals do not sufficiently bolster spot PVC prices.

Additionally, the prices of upstream raw materials such as calcium carbide and ethylene have experienced a slight decline due to reduced supply pressure from downstream maintenance, resulting in weak bottom support for PVC production costs.

The United States implemented a 145% tariff on imports from China, to which China responded with a 125% tariff on imports from the United States. These significant measures have influenced the demand for PVC in China, leading to an increased supply from Chinese manufacturers in the spot market across Asia.

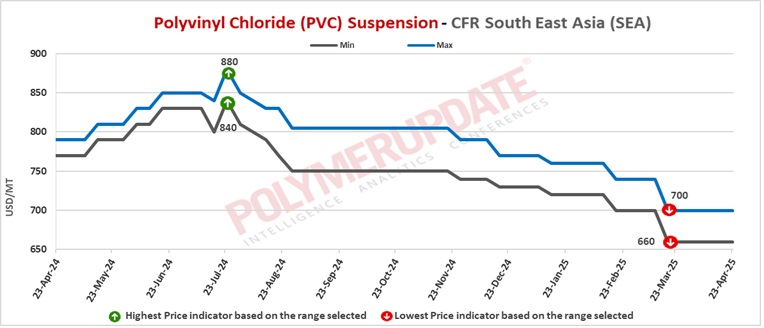

In Southeast Asia, PVC prices were assessed at the USD 660-730/mt CFR levels, up USD (NC/+30/mt) from the previous week.

In Southeast Asia, a Taiwanese producer has offered its PVC resin suspension grade at the USD 730/mt levels for shipment in May 2025.

In Southeast Asia, PVC prices remained stable although import activity has remained sluggish as buyers opted to hold off due to weak spot demand.

The United States has imposed relatively high tariffs on numerous Southeast Asian nations, with imports from Vietnam facing a 46% tariff, for instance. Although the US has suspended reciprocal tariffs on all trading partners for a period of 90 days since April 9, the demand for PVC continues to be impacted by the baseline import tariff of 10%, along with uncertainty regarding whether ongoing negotiations will postpone or mitigate the severity of the US's forthcoming reciprocal tariffs. Buyers are closely observing the situation during this 90-day pause in reciprocal tariffs.

Despite the decline in import activity throughout the week, Chinese ethylene-based s-PVC offers have remained consistently available in the market. Additionally, the commencement of AGC Vinythai's new 400,000 mt/year s-PVC unit in Thailand is anticipated to be finalized by the second quarter, following some delays. It is still too early to conclude that the initiation of new s-PVC production in Thailand will significantly lengthen the s-PVC balance, as the producer will also be managing production expansions of chlor-alkali and EDC facilities, to supply the new facility later in the year.

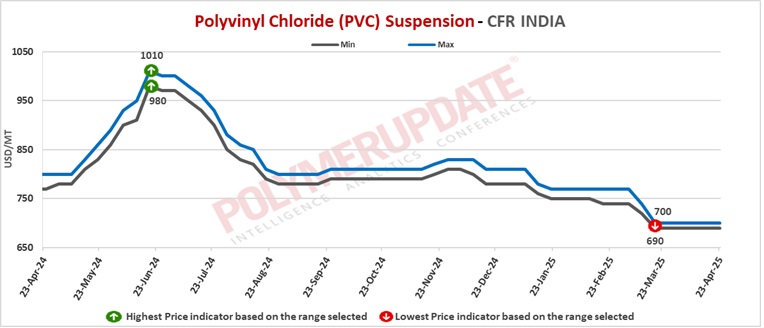

In India, PVC prices were assessed at the USD 690-700/mt CFR levels, stable from last week.

In India, a major Taiwanese producer has offered its PVC suspension grades (S65D/S65/S60/S70) at the USD 700/mt levels and (B57) grade at the USD 720/mt levels on CIF Nhava Sheva/Mundra/ Chennai ports basis for May shipment. These offers are stable from the previous month’s offers. Add USD 40/mt for CIF Kolkata/Cochin/Pipavav ports. For LC 90 days (Add USD 10/mt).

| PVC Offer Prices from Taiwan (USD/MT - LC at Sight) | |||||

| May | April | March | February | January | |

| CIF India | 700 | 700 | 740 | 760 | 785 |

| CFR China Main Port | 700 | 700 | 725 | 725 | 740 |

| CIF Southeast Asia | 730 | 730 | 755 | 755 | 770 |