Click the icon to add a specified price to your Dashboard list. This makes it easy to keep track on the prices that matter most to you.

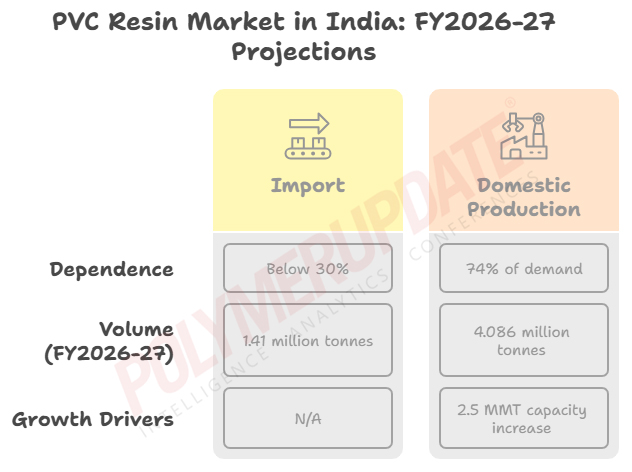

India's reliance on imported polyvinyl chloride (PVC) resin is projected to decline to less than 30 percent of the country’s total demand for the plastic raw material by the financial year 2026-27, according to a study by the leading rating agency, Care Ratings Ltd. This reduction is attributed to a significant increase in domestic production, driven by substantial investments in greenfield and brownfield projects.

The study indicates that India’s PVC import dependence is expected to stand at 1.41 million tonnes, approximately 26 percent of the anticipated total demand of 5.496 million metric tonnes (MMT) in FY 2026-27. Domestic production is set to meet the remaining 74 percent of demand, with a record volume of 4.086 million tonnes.

| PVC resin demand-supply dynamics (million tonnes) | |||

| Financial year (April-March) | Domestic production | Imports | Total demand |

| 2026-27 | 4.086 | 1.410 | 5.496 |

| 2025-26 | 1.711 | 3.378 | 5.089 |

| 2024-25 | 1.621 | 3.091 | 4.712 |

| 2023-24 | 1.507 | 2.735 | 4.242 |

| 2022-23 | 1.571 | 2.326 | 3.897 |

| 2021-22 | 1.498 | 1.475 | 2.973 |

Sources: Care Ratings Ltd, and Polymerupdate Research

"Given the robust and sustained demand for PVC resin observed in recent years, the top five industry players are establishing large-scale manufacturing capacities. An incremental PVC resin production capacity of around 2.5 MMT is expected to become operational by FY27. As a result, India’s import dependency for PVC resin is projected to decline from around 3 MMT in FY 2024-25 to approximately 1.4 MMT in FY 2026-27," the study states. Healthy demand growth

Healthy demand growth

Demand for PVC resin has grown at a healthy compounded annual growth rate (CAGR) of 6.2 percent during FY 2020-2025. PVC resin demand reached 4.7 million metric tonnes (MMT) in FY 2024-25, reflecting approximately 11 percent year-on-year (YoY) growth. This surge was driven by robust demand from end-user sectors, supported by favourable government initiatives such as the Pradhan Mantri Awas Yojana and the Jal Jeevan Mission. Moving forward, the growth momentum is expected to persist, with PVC demand projected to expand at a rate of around 8 percent per annum, reaching 5.5 MMT by FY 2026-27.

This growth is anticipated to be fuelled by strong demand from end-user sectors, given the currently low per capita consumption of PVC in India. PVC resin (suspension and paste) is primarily utilized in key sectors such as irrigation systems (pipes), real estate (plumbing and building materials), infrastructure (water supply and sanitation), and automotive. Notably, approximately 80 percent of PVC resin demand stems from the production of pipes and fittings, while wires and cables account for about 7 percent. These products play critical roles in the aforementioned end-use sectors, underpinning the projected growth in demand.

Stagnant domestic output in recent years

Driven by robust demand growth and stagnant domestic manufacturing capacity, which has remained around 1.8 million metric tonnes (MMT) over the past few years, the demand-supply gap for PVC resin widened significantly. This gap increased from approximately 1.5 MMT in FY 2021-22 to around 3 MMT in FY 2024-25, primarily met through a steady rise in imports from countries like China, Japan, Taiwan, South Korea, and the USA.

Despite this, substantial import dependency is expected to persist in the foreseeable future due to the inadequate and unreliable availability of a key raw material, ethylene dichloride (EDC). This limitation may hinder the PVC industry's ability to undertake further large-scale capacity expansions.

In the immediate aftermath of the COVID-19 pandemic, domestic PVC prices and the PVC-EDC spread improved during FY 2020-21 and FY 2021-22 due to supply-side constraints. However, PVC prices experienced a significant correction in FY 2022-23 as supply normalized and global demand weakened. During FY 2023-2025, challenging global macroeconomic conditions led to subdued international demand for PVC, resulting in an oversupply in the global market. This surplus was redirected to countries like India, where PVC demand remained robust.

China’s dumping

Excess capacity and weak demand in China have led to significant dumping of PVC into the Indian market over the past few years. Imports from China, which constituted only about 3 percent of India’s total PVC imports in FY 2019-20, surged to approximately 40 percent in FY 2024-25. Similarly, subdued demand in the USA resulted in the diversion of surplus production to India.

This influx of imports exerted sustained pressure on PVC prices, which dropped by 24 percent, from US$ 1,026 per tonne in FY 2022-23 to US$ 782 per tonne in FY 2024-25. Consequently, the PVC-EDC spread also contracted, adversely affecting the profitability of domestic PVC manufacturers.

India’s import restrictions

In February 2024, India’s Department of Chemicals and Petrochemicals issued a Quality Control Order requiring a BIS certificate for PVC imports, which is expected to take effect on June 24, 2025, following several postponements. Additionally, in October 2024, the Directorate General of Trade Remedies (DGTR), in its preliminary findings, recommended imposing an Anti-Dumping Duty (ADD) of up to US$ 339 per tonne on imports of suspension-grade PVC resin from seven countries: China, Indonesia, Japan, South Korea, Taiwan, Thailand, and the United States.

The primary aim of this ADD is to protect domestic manufacturers. It could be implemented once the DGTR submits its final findings and receives approval from the Ministry of Finance. Furthermore, in March 2025, the Ministry of Finance notified an ADD of up to US$ 707 per tonne on imports of paste-grade PVC resin from China, South Korea, Malaysia, Norway, Taiwan, and Thailand.

Price spread

The Care Ratings study anticipates the PVC-EDC (ethylene dichloride) spread to remain under pressure, averaging below US$ 400 per tonne during April–September 2025, due to a slowdown in major global economies and the ongoing trade war, despite robust domestic demand. However, with BIS quality standards expected to take effect soon and the potential imposition of Anti-Dumping Duty (ADD) on suspension-grade PVC resin imports, the PVC-EDC spread is projected to improve to approximately US$ 500 per tonne during October 2025–March 2026, providing relief to domestic PVC manufacturers.

Outlook

Care Ratings foresees a significant transformation in India’s PVC resin market, driven by robust annual demand growth projected at approximately 8 percent, reaching 5.5 million metric tonnes (MMT) by FY 2026-27. The addition of nearly 2.5 MMT in domestic capacity by FY 2026-27 is expected to more than double current production levels, reducing import dependency from around 62 percent in FY 2024-25 to below 30 percent of total domestic consumption by FY 2026-27.

“Moreover, the anticipated enforcement of BIS quality standards and the likely imposition of Anti-Dumping Duty on suspension-grade PVC resin imports are expected to curtail low-priced imports, support domestic price recovery, and improve the PVC-EDC spread to approximately US$ 500 per tonne during October 2025–March 2026,” said Rohan Deshmukh, Assistant Director at Care Ratings Ltd.

DILIP KUMAR JHA

Editor

dilip.jha@polymerupdate.com