Click the icon to add a specified price to your Dashboard list. This makes it easy to keep track on the prices that matter most to you.

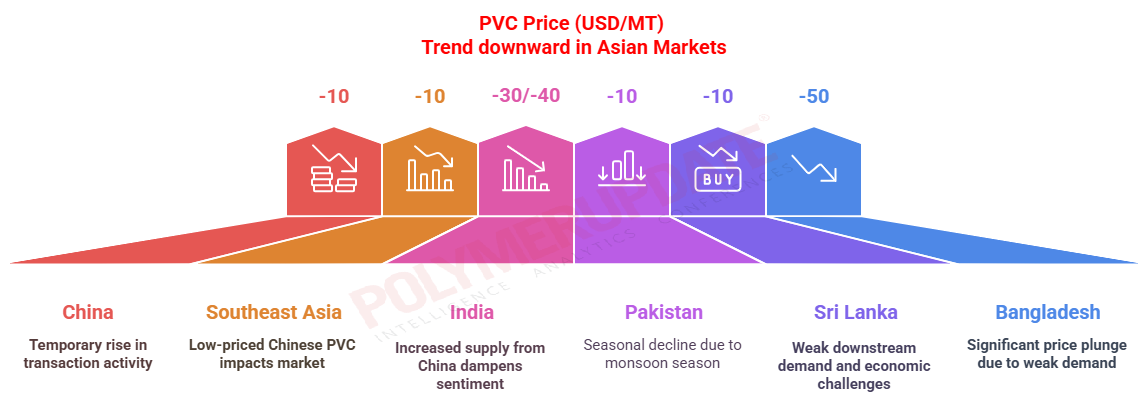

This week, PVC prices down adjusted in the Asian region.

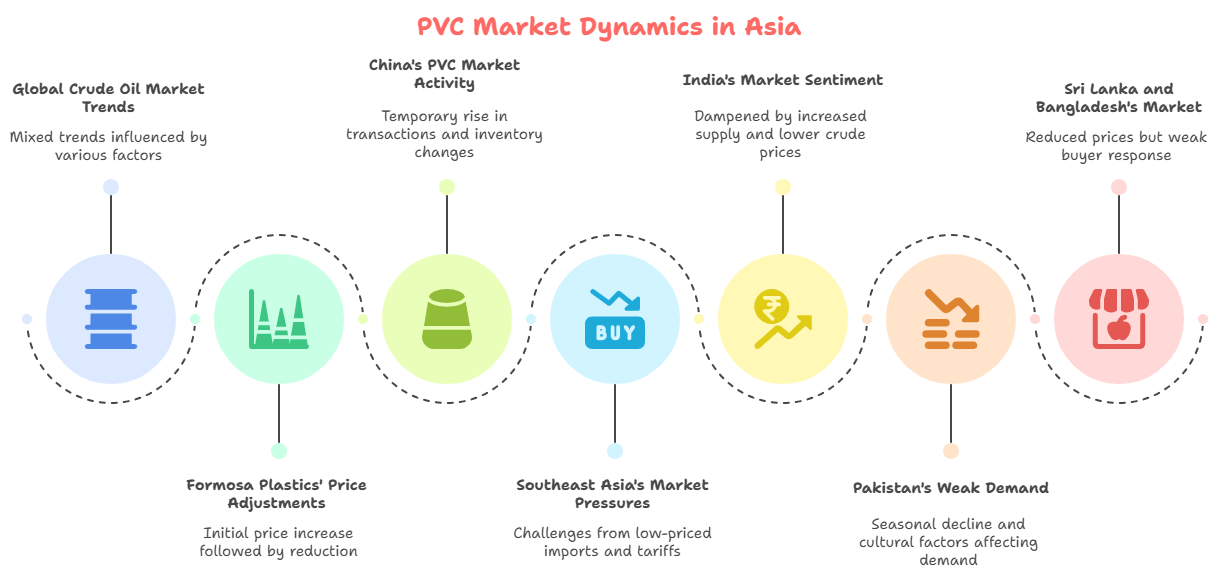

An industry source in Asia, on condition of anonymity, informed a Polymerupdate team member, "The global crude oil market has been exhibiting mixed trends, shaped by both supportive and limiting factors. On the positive side, reduced U.S. tariff pressures, ongoing sanctions on key oil producers, and strong seasonal demand in the U.S. provide some upward momentum. However, bearish influences such as easing tensions between Iran and Israel, expectations of an OPEC+ output increase, and broader global economic concerns are capping price gains. Additionally, the U.S. has signalled efforts to restart peace talks between Russia and Ukraine, helping to ease geopolitical tensions and reduce supply risks. Meanwhile, container shipping rates from East Asia and China to the U.S. are under pressure, as rising capacity on major trans-Pacific routes is driving down freight prices despite steady trade flows.”

The source added, “Formosa Plastics Corporation of Taiwan recently announced higher PVC offers for July shipments due to rising production costs stemming from volatile oil prices and higher freight charges. Nonetheless, market sales did not meet expectations since the de-escalation of Middle East conflicts resulted in decreased crude prices and lower shipping expenses. Moreover, during their usual off-season, buyers opposed the price increase, and competition from more affordable mainland Chinese exports exerted additional pressure on sales. Consequently, the company reduced its offer price for July/August and offered discounts on bulk purchases to stay competitive in a market landscape marked by uncertainties.”

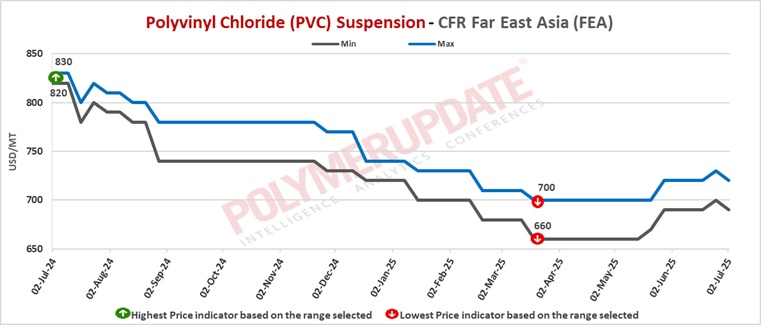

In China, PVC prices were assessed at the USD 690-720/mt CFR levels, a fall of USD (-10/mt) week on week.

In China, a Taiwanese producer has offered its PVC resin suspension grades at the USD 700/mt, for shipment in July/August 2025.

In China, there has been a temporary rise in transaction activity within the market, prompting companies to modify their inventories. This surge is primarily fuelled by heightened procurement from downstream sectors. Nevertheless, social inventory has also experienced a slight uptick, mainly due to manufacturers increasing their operating rates, which results in ongoing supply-side pressure. Anticipated domestic PVC maintenance activities are set to escalate next week, with Xinpu Chemical and Erong planning to boost their maintenance volumes, which will further contribute to a reduction in supply. In spite of this, domestic demand continues to be weak. The operating rates for hard PVC products are projected to decrease further, while operations for soft products, although performing relatively better, have seen a slight decline compared to the same period last year. Additionally, foreign demand is currently in its off-season, which adds to the pressure on export orders. In the near term, the market is unlikely to overcome the issue of oversupply. The ongoing decline in the real estate sector continues to significantly impact PVC demand, with pipe production—a crucial aspect of traditional PVC consumption—remaining at low levels. While the current plant maintenance will limit some supply, this effect is expected to be counterbalanced by the start-up of new domestic production capacity, which may lead to an increase in social inventory. The overall market outlook reflects a combination of expanding capacity, weak downstream demand, and decreasing cost support.

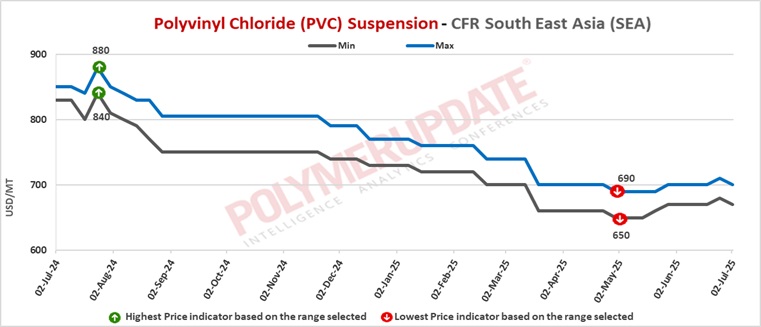

In Southeast Asia, PVC prices were assessed at the USD 670-700/mt CFR levels, lower by USD (-10/mt) from the previous week.

In Southeast Asia, a producer from Taiwan has offered its PVC resin suspension grade at the USD 670-680/mt, for shipment in July / August 2025. South Korean producer offered its PVC resin suspension grade at the USD 700/mt, for shipment in July 2025. Other Asian producers offered their PVC resin suspension grade in the range of USD 650-680/mt CFR levels, for shipment in July /August 2025.

In Southeast Asia, discussions in the spot PVC market faced heightened pressure due to multiple factors. Firstly, the availability of low-priced PVC materials from China led to a decline in local prices, posing challenges for regional suppliers to maintain their competitiveness. Secondly, the introduction of US tariffs on Southeast Asian countries starting in early July created uncertainty and likely diminished purchasing interest, as import costs and trade conditions became more complex. Furthermore, Malaysia's proposed implementation of a 5% sales and service tax on PVC imports raised costs, which in turn dampened domestic demand. Collectively, these elements resulted in a decline in market activity and a reduction in the demand for PVC in Southeast Asia.

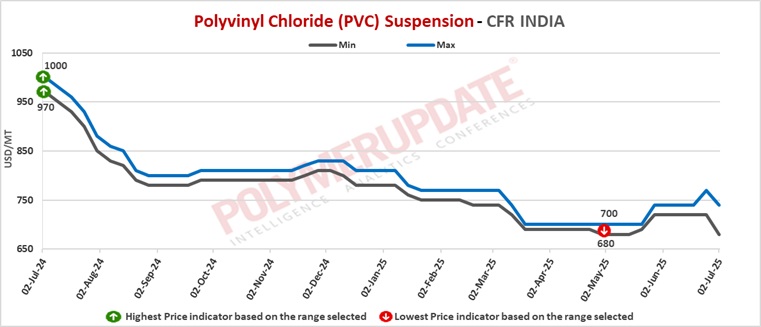

In India, PVC prices were assessed at the USD 680-740/mt CFR levels, a week on week sharp drop of USD (-30/-40/mt).

A domestic industry source informed a Polymerupdate team member, “Reliance Industries Limited has increased its PVC prices by Re.1/kg basic with effect from July 1, 2025.”

A major Taiwanese producer has down revised its offers for PVC suspension grades (S65D/S65/S60/S70) at the USD 745/mt levels while grade (S57 & B57) is on offer at the USD 755/mt levels on CIF Nhava Sheva/Mundra/Chennai port basis with shipment for August 2025 (LC at sight). A South Korean producer has offered its PVC resin suspension grade at the USD 745/mt, for shipment in July/August 2025.

A producer from Saudi Arabia has offered its PVC resin suspension grade at the USD 740/mt CFR levels, for shipment in July/August 2025. A Chinese producer has offered its PVC (ethylene-based) at the USD 680-685/mt levels. Meanwhile, carbide-based PVC was on offer at the USD 660/mt levels.

This week, sentiment was dampened in India’s PVC market due to an increase in supply from China, following the extension of the Bureau of Indian Standards (BIS) deadline until December 2025. This extension has led buyers to be more inclined to accept shipments from China. Furthermore, the recent decrease in crude oil prices—resulting from the ceasefire between Israel and Iran—has further impacted market sentiment, as lower crude prices generally lower feedstock costs but may also indicate a decline in overall demand.

A trader in India stated that new offers for PVC material loading in July from Asia (excluding China) emerged last week. However, the market's reaction was tepid as Chinese suppliers were offering material at a substantial discount of over USD 60/mt, which made it challenging for other suppliers to compete. In response to weak demand and aggressive pricing from China, several Asian suppliers lowered their offer prices by approximately USD 20/mt throughout the week in an effort to draw buyers to the market.

Pipe manufacturers in India are currently operating at lower output rates due to weak downstream demand. This situation is exacerbated by widespread rainfall across the nation, which has hindered construction activities and related demand. Furthermore, the abundant availability of competitively priced Chinese PVC shipments is exerting pressure on local imports. With peak monsoon conditions anticipated to continue until the end of August, the near-term import demand for PVC is expected to remain low.

In Pakistan, PVC prices were assessed at the USD 720-760/mt CFR levels, down USD (-10/mt) from last week.

In Pakistan, an Indonesian producer has offered its PVC resin suspension grade at the USD 750-760/mt, for shipment in July/August 2025. A Chinese producer has offered its PVC (carbide-based) at the USD 745/ levels.

In Pakistan, the purchasing sentiment has remained weak due to the usual seasonal decline in demand brought about by the monsoon season. Spot offers have been stable throughout the week, indicating a cautious yet steady market; however, actual transaction volumes have been restricted due to the sluggish demand. Additionally, the commencement of Muharram is anticipated to further limit market activity in the upcoming week, as businesses and buyers generally scale back their operations during this time. This cultural aspect is likely to lead to ongoing subdued demand and restricted trading.

In the wake of the tariff reduction announcement on PVC imports in Pakistan, some producers initially increased their offer prices, although this rise was quite minimal. Despite the reduction in tariffs, the purchasing sentiment has continued to be weak, with demand remaining subdued amid persistent seasonal and market pressures.

In Sri Lanka, PVC prices were assessed at the USD 700-750/mt CFR levels, a week on week decline of USD (-10/mt).

In Sri Lanka, overseas producers have offered PVC resin suspension grades in the range of USD 700-750/mt, for shipment in July/August 2025.

In Bangladesh, PVC prices at the USD 680-710/mt CFR levels, a plunge of USD (-50/mt) from the pervious week.

In Bangladesh, a Taiwanese producer has offered PVC resin suspension grade at the USD 710/mt, for shipment in July/August 2025. A Chinese producer has offered its PVC (ethylene-based) at the USD 680/mt levels. Meanwhile, carbide-based PVC was on offer at the USD 670/mt levels.

In Sri Lanka and Bangladesh, PVC import offers experienced a marked decrease. In spite of the reduced prices, buyers largely exhibited a lack of response, indicating persistent weakness in downstream demand. Market activity was considerably muted, particularly due to sluggish demand from essential sectors such as construction and infrastructure. Furthermore, overarching economic challenges, including currency fluctuations and obstacles in obtaining import financing, further suppressed purchasing interest, hindering market recovery.

Feedstock EDC prices were assessed at the USD 170-180/mt CFR China level while CFR South East Asia EDC prices were assessed at the USD 175-185/mt levels, both constant week on week.

Feedstock CFR South East Asia VCM prices were assessed stable at the USD 560-570/mt levels while CFR China VCM prices were assessed flat at the USD 520-530/mt levels.

Feedstock ethylene prices on Tuesday were assessed at the USD 855-865/mt CFR South East Asia levels, meanwhile CFR North East Asia ethylene prices were assessed at the USD 845-855/mt levels, both rolled over from the previous week.

In plant news, China General Plastics Corporation (CGPC) is likely to take off stream its Polyvinyl chloride (PVC) in July 2025 for maintenance. Further details on the duration of the shutdown could not be ascertained. Located in Toufen, Taiwan, the plant has a production capacity of 230,000 mt/year.