Click the icon to add a specified price to your Dashboard list. This makes it easy to keep track on the prices that matter most to you.

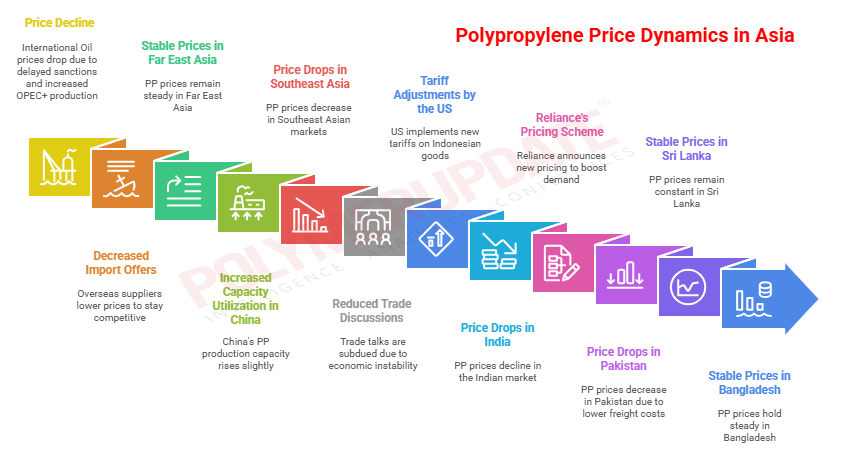

This week, Polypropylene prices dropped in parts of Asia.

An industry source in Asia, on condition of anonymity, informed a Polymerupdate team member, “International oil prices experienced a decline, largely attributed to the delayed enforcement of U.S. sanctions targeting Russian energy exports. This postponement has eased immediate supply concerns in global markets. Additionally, the continued production increases by OPEC+ a coalition of the Organization of the Petroleum Exporting Countries and allied producers- have further contributed to downward pressure on prices by boosting overall supply amid relatively stable demand conditions.”

The source added, “The persistent decrease in import offers from overseas suppliers has greatly impacted the continuing weakness in market prices. Overseas sellers, aiming to stay competitive amidst uncertain global demand and fluctuating currencies, are offering material at significantly lower prices. This trend has heightened competition among local and international sellers while also leading buyers to take a wait-and-see stance, expecting additional decreases.”

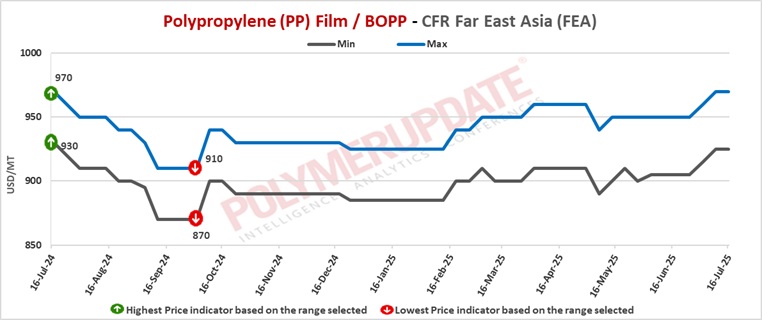

In Far East Asia, PP raffia and PP injection prices were assessed at the USD 885-920/mt CFR levels, both stable week on week. PP film were assessed flat at the USD 925-970/mt CFR levels. PP BOPP prices were assessed steady at the USD 895-940/mt CFR levels. PP block copolymer prices were also assessed stable at the USD 935-960/mt CFR levels.

In China, a producer from the Middle East has offered its PP raffia and PP injection grade at the USD 885/mt levels, for shipment in end July/early August 2025. A producer from Saudi Arabia has offered its PP raffia and PP injection at the USD 920/mt levels, for shipment in end July/early August 2025.

In China, polypropylene capacity utilization experienced an uptick with a partial resumption, yet ample supply and off-season demand maintained significant market pressure. There was hardly any support for spot prices due to low downstream activity. The supply-demand gap decreased marginally, improving sentiment, but is anticipated to expand once more, heightening price pressure.

Weaker support for crude oil and cautious shipments led to a decline in spot prices. Due to restricted cost-side impact and sluggish procurement activity, market sentiment stayed wary. Futures remained low, leading to price reductions that encouraged some downstream purchases, maintaining a moderately active trading environment

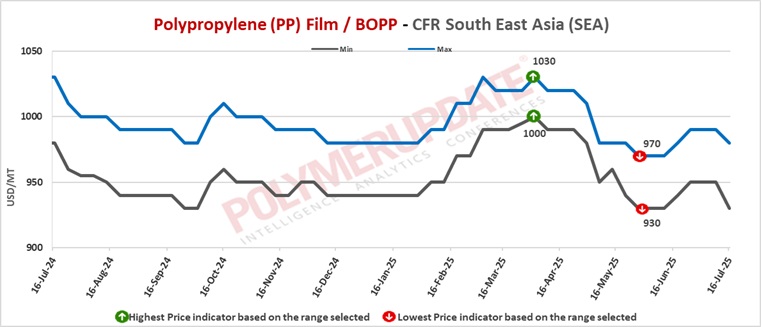

In Southeast Asia, PP raffia and PP injection grade prices were assessed at the USD 880-930/mt CFR levels, both dropped by USD (-10/-20/mt) from the previous week. PP film prices were assessed at the USD 930-980/mt CFR levels, a week on week decrease of USD (-10/-20/mt). BOPP prices were assessed at the USD 890-950/mt CFR levels, while PP block copolymer prices were assessed at the USD 940-980/mt CFR levels, both down adjusted by USD (-10/-20/mt) from last week.

In Vietnam, a Saudi Arabian producer has offered its PP raffia and PP injection grade at the USD 880-890/mt levels, for shipment in end July/ early August 2025. A producer from Middle East has offered its PP raffia and PP injection at the USD 930/mt levels, for shipment in end July/ early August 2025.

In Southeast Asia, trade discussions were subdued because of economic instability from tariff adjustments by the US, low demand for finished products, and local pricing competition. Output increased as producers in Indonesia and Malaysia ran their plants at maximum capacity levels, with Malaysia facing pressure to complete creditor reliability tests. Indonesia's import demand stayed subdued, as domestic prices were more favourable.

The United States has implemented a flat 19% tariff on all goods imported from Indonesia, marking a significant reduction from the previously proposed rate of 32%. This has sparked a swift response in trade circles. To prepare for heightened competition and offload current stock levels, traders have started offering material at prices lower than assessed levels, exerting downward pressure in the market. The initiative is anticipated to alter trade patterns and affect regional pricing trends, especially in industries dependent on products from Indonesia.

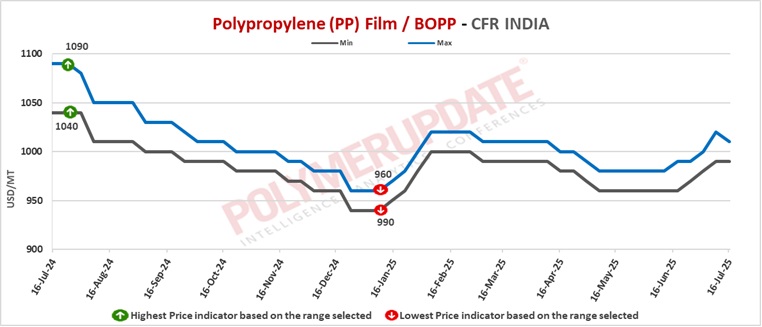

In India, PP raffia and PP injection prices were assessed at the USD 945-970/mt CFR levels, lower by USD (-5/-10/mt) from the previous week. PP film prices were assessed at the USD 975-990/mt CFR levels while PP BOPP prices were assessed at the USD 965-990/mt CFR levels, both week on week declined by USD (-5/-10/mt). PP block copolymer prices were assessed at the USD 985-1010/mt CFR levels, a fall of USD (-5/-10/mt) from the previous week.

In India, a Middle eastern producer has offered its PP raffia and PP injection grade at the range of USD 945-970/mt levels, for shipment in end July/ early August 2025. A producer from China has offered its PP raffia and PP injection grade at the USD 950/mt levels, for shipment in end July/early August 2025.

Reliance Industries Limited (RIL) announced its polypropylene (PP) pricing scheme for the domestic Indian market for July 2025 in an effort to stimulate buying activity amid weak demand and cautious market sentiment. The scheme includes revised grade-wise offers for various PP grades such as homopolymer, random copolymer, and impact copolymer, aiming to provide price incentives and encourage fresh procurement from downstream buyers. Market participants are watching closely to see whether the revised offers will revive momentum in a sluggish market influenced by lower import offers and subdued end-user demand.

Polypropylene prices in India fell as trading activity diminished following sizeable July order volumes. Chinese-sourced PP homopolymer has seen a slight softening due to reduced freight expenses, resulting in a few transactions at lower price points. Additional decreases in freight could put strain on August bids. Domestic supply continues to be sufficient, but demand is expected to decline because of monsoon-related disruptions in construction and packaging. Although certain producers in the Middle East are experiencing disruptions, the effect on Indian supply is anticipated to be slight.

In Pakistan, PP raffia and PP injection grade prices were assessed at the USD 950-980/mt levels, both down adjusted by USD (NC/-10/mt) from last week. PP film and BOPP prices were assessed at the USD 990-1010/mt CFR levels, both dropped by USD (NC/-10/mt) from the previous week. PP block copolymer prices were assessed at the USD 1000-1040/mt CFR levels, both week on week decreased by USD (NC/-10/mt).

In Pakistan, a producer from Saudi Arabia has offered its PP raffia and PP injection grade at the USD 980/mt levels, for shipment in end July/early August 2025. A Middle Eastern producer has offered its PP raffia and PP injection grade at the USD 950/mt levels, for shipment in end July/early August 2025.

In Pakistan, PP prices declined this week as reduced freight expenses enhanced the competitiveness of Asian-origin shipments, applying downward pressure on domestic price levels. In reaction, a primary supplier from the Gulf Middle East region lowered its prices to safeguard market share and maintain price competitiveness. Although there was a short surge in buying interest after the government reduced customs duties, the momentum swiftly dissipated once authorities reintroduced a 2% import duty. The abrupt change in policy reduced optimism, causing numerous buyers to defer purchase commitments while awaiting potential additional price changes or more definitive policy guidance clearer policies

In Sri Lanka, PP raffia and PP injection grade prices were assessed at the USD 950-990/mt CFR levels, both steady week on week. PP film and BOPP prices were assessed at the USD 1000-1020/mt CFR levels, both constant from last week. PP block copolymer prices were assessed flat at the USD 1030-1040/mt CFR levels.

In Sri Lanka, a producer from Saudi Arabia has offered its PP raffia and PP injection grade at the USD 990/mt levels, for shipment in end July/early August 2025. A Middle Eastern producer has offered its PP raffia and PP injection grade at the USD 950/mt levels, for shipment in end July/early August 2025.

In Sri Lanka, polypropylene (PP) prices held steady last week, even with weak purchasing sentiment throughout the region. Market activity was restricted as buyers maintained a wary approach due to macroeconomic unpredictability and an absence of urgent demand. Despite adequate regional supply, no notable price changes occurred, indicating a balanced yet sluggish market sentiment

In Bangladesh, PP raffia and PP injection prices were assessed at the USD 940-970/mt CFR levels, both steady from the previous week. PP film and BOPP prices were assessed at the USD 960-980/mt CFR levels, both week on week constant. PP block copolymer prices were assessed stable at the USD 1000-1040/mt CFR levels.

In Bangladesh, a producer from Saudi Arabia has offered its PP raffia and PP injection grade at the USD 940/mt levels, for shipment in end July/early August 2025. A Middle Eastern producer has offered its PP raffia and PP injection grade at the USD 970/mt levels, for shipment in end July/early August 2025.

In Bangladesh, demand outlook softened following reports that the US was in plans to implement a 35% import tariff on goods from the nation. Local suppliers observed weak sales as purchasers stayed out of the market, while low-priced goods originating from China aggravated price pressure. Overall spot indications were scarce

Feedstock propylene prices on Tuesday were assessed at the USD 770-780/mt CFR China levels, a week on week drop of USD (-5/mt). Meanwhile, FOB Korea propylene prices were assessed stable at the USD 735-745/mt levels.

In plant news, Jingbo Polyolefin is in plans to take off stream its No.2 Polypropylene (PP) unit on July 16, 2025 for maintenance. The unit is slated to remain offline for about 45 days. Located in Shandong province, China, the No.2 unit has a production capacity of 400,000 mt/year.

In other plant news, Dongming Petrochemical is likely to take off stream its Polypropylene (PP) unit by end July 2025 for maintenance. The unit is slated to remain offline for about 45 days. Located in Shandong province of China, the PP unit has a production capacity of 200,000 mt/year.

In another plant news, Shandong Chambroad Sinopoly New Material is likely to shut down its No.1 Polypropylene (PP) plant on July 15, 2025. Further details on the duration of the shutdown could not be ascertained. Located in Binzhou, China, the plant has a production capacity of 400,000 mt/year.