Click the icon to add a specified price to your Dashboard list. This makes it easy to keep track on the prices that matter most to you.

This week, HDPE prices dropped in Pakistan, Sri Lanka and Bangladesh, while staying flat in other parts of the Asian region._prices_ease_in_parts_of_South_Asia_-_visual_selection.png) An industry source in Asia, on condition of anonymity, informed a Polymerupdate team member, “Global markets are closely monitoring the upcoming US-Russia summit, as its outcome could play a pivotal role in reducing both geopolitical tensions and oil price volatility. A positive outcome, such as sanctions relief or conflict de-escalation, could increase global oil supply, lower risk premiums, and boost market confidence, potentially pushing prices down.”

An industry source in Asia, on condition of anonymity, informed a Polymerupdate team member, “Global markets are closely monitoring the upcoming US-Russia summit, as its outcome could play a pivotal role in reducing both geopolitical tensions and oil price volatility. A positive outcome, such as sanctions relief or conflict de-escalation, could increase global oil supply, lower risk premiums, and boost market confidence, potentially pushing prices down.”

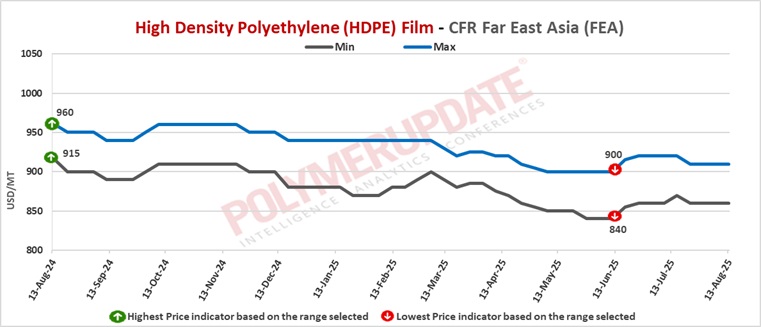

In Far East Asia, HDPE film prices were assessed at the USD 860-910/mt CFR levels while HDPE blow moulding prices were assessed at the USD 840-900/mt CFR levels, both week on week constant. HDPE injection prices were assessed stable at the USD 830-860/mt CFR levels, and HDPE yarn prices were assessed flat at the USD 880-900/mt CFR levels.

In China, a Saudi Arabian producer has offered its HDPE film grade at the USD 910/mt CFR levels, for shipment in September 2025. A producer from Middle East has offered its HDPE film grade at the USD 860/mt CFR levels, for shipment in September 2025.

In China, prices remained consistent. The US dollar price in China’s HDPE import market is presently stable, exhibiting minimal fluctuations as both buyers and sellers adopt a cautious approach. Importers are strategically purchasing during price declines, indicating a cautious observation strategy instead of active buying. Market players are attentively observing international price differences, new offer rates, and changing demand trends, which are expected to impact short-term price changes. Although domestic HDPE prices in China are still low, they are creating a negative impact on overall sentiment, leading importers to avoid raising their bid levels. On the supply side, specific foreign sellers, especially from Saudi Arabia, are maintaining their offers because of limited spot availability. This rigidity is causing a broader buy-sell spread, restricting transaction activity.

The postponement of China–US trade negotiations has redirected interest to competitively priced cargoes from the US, with imports expected to focus on major ports in the near term and domestic supply anticipated to increase from late August to early September as additional plants start operations. The increase in supply, combined with demand-driven buying downstream, is restraining market momentum, while doubts about macroeconomic stimulus and the absence of robust fundamental support persist in limiting gains. The recent 90-day prolongation of the China–US mutual tariff truce until November 10 offers temporary stability for trade movements but is improbable to cause substantial price increases without a wider demand rebound.

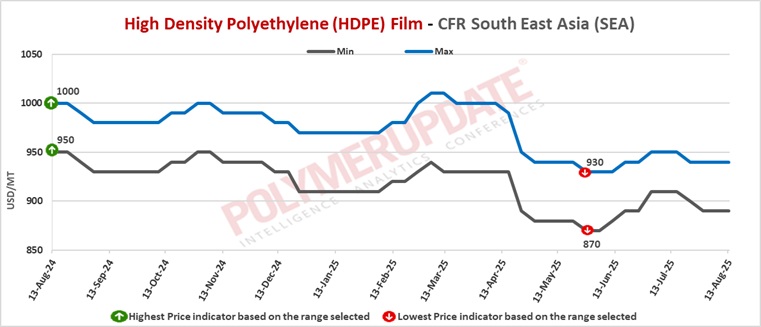

In Southeast Asia, HDPE film prices were assessed at the USD 890-940/mt CFR levels, rolled over from last week. HDPE blow moulding grade prices were assessed at the USD 840-890/mt CFR levels, unchanged week on week. HDPE injection prices were assessed flat at the USD 840-890/mt CFR levels and HDPE yarn prices were assessed steady at the USD 920-960/mt CFR levels.

In Malaysia, an Asian producer has offered its HDPE film grade at the USD 930/mt CFR levels, for shipment in September 2025. In Vietnam, a producer from Saudi Arabia has offered its HDPE film grade at the USD 880/mt CFR levels, for shipment in September 2025. Reports of some deals concluded at the USD 860/mt levels could not be confirmed officially.

In Indonesia, a Middle Eastern producer has offered its HDPE film grade at the USD 930/mt CFR levels, for shipment in September 2025. In Southeast Asia, a producer from the Middle East has offered its HDPE film grade at the USD 910-920/mt CFR levels, for shipment in September 2025.

In Southeast Asia, HDPE prices remained stable due to limited spot activity, with the majority of offers coming from regional and US suppliers. Prices could experience downward pressure in August due to the startup of new capacities, increasing supply amidst weak downstream demand, although a slight demand recovery is expected in September–October during the peak year-end period. Overall annual PE consumption is anticipated to decline compared to last year, impacted by decreased export orders due to US tariffs and weakened domestic demand associated with slower economic growth.

Price evaluations vary but are generally under pressure following a Vietnamese producer’s renewal of offers for August–September deliveries, signalling its comeback since October 2024. This resurgence has heightened competition and compressed trading ranges in Vietnam, while prices from the Middle East have declined due to greater competition and recently implemented import taxes. CFR Southeast Asia dutiable prices are evaluated on the lower side due to weak deal activity, while non-dutiable prices stay stable amid limited conversations. CFR Vietnam prices are established through a mix of finalized agreements, current offers, and purchase indications.

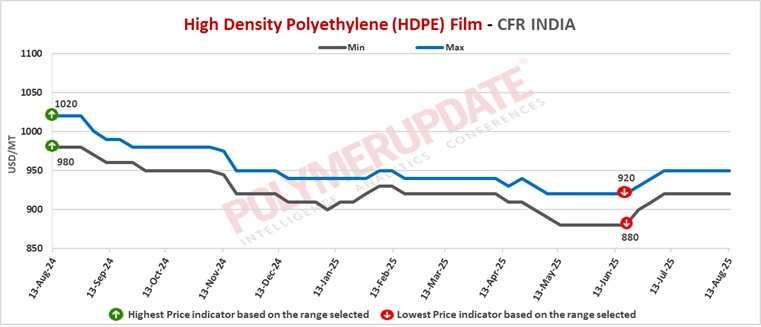

In India, HDPE film prices were assessed flat at the USD 920-950/mt CFR levels while HDPE yarn prices were assessed stable at the USD 900-940/mt CFR levels. HDPE Injection prices were assessed at the USD 910-960/mt CFR levels while HDPE blow moulding prices were assessed at the USD 910-930/mt CFR levels, both unchanged week on week.

In India, a Middle Eastern producer has offered its HDPE film grade at the USD 920/mt CFR levels, for shipment in September 2025. A Saudi Arabian producer has offered its HDPE film grade at the USD 950/mt CFR levels, for shipment in September 2025. Buying indication was heard below USD 900/mt levels.

In India, August HDPE demand remained steady but faces potential softening due to new incentives and subdued seasonal buying. The rupee’s depreciation, ongoing US trade tensions, and impending tariff hikes have curbed imports, while domestic discounts have encouraged buyers to source locally. Although festive-season restocking could offer some support, high feedstock costs combined with ample supply are expected to keep prices under downward pressure.

In Pakistan, HDPE film prices were assessed at the USD 940-970/mt CFR levels while HDPE blow moulding grade prices were assessed at the USD 950-980/mt CFR levels, both down adjusted by USD (-10/mt) week on week. HDPE yarn grade prices were assessed at the 950-980/mt CFR levels and HDPE injection grade prices were assessed at the USD 940-970/mt CFR levels, both lower by USD (-10/mt) from the previous week.

In Pakistan, a Middle Eastern producer has offered its HDPE film grade at the USD 960/mt CFR levels, for shipment in September 2025. A Saudi Arabian producer has offered its HDPE film grade at the USD 980/mt CFR levels, for shipment in September 2025.

In Pakistan, HDPE prices dropped due to weak demand and increasing inventories among importers causing ongoing downward pressure. Numerous sellers focused on selling off newly arrived shipments rather than engaging in new purchases at elevated prices, resulting in restricted new deals in the market. Inventory levels are anticipated to stay elevated during August, with only slight restocking expected around mid-September as demand increases for seasonal needs. The recent surge of Iranian HDPE supply has led to a rise in inventory levels, heightening competition among vendors and contributing to price declines. Given the weak macroeconomic outlook, limited liquidity, and cautious purchasing behaviour exhibited by downstream buyers, market conditions are anticipated to remain difficult in the short term

In Sri Lanka, HDPE film prices were assessed at the USD 940-980/mt CFR levels and HDPE blow moulding prices were assessed at the USD 940-980/mt CFR levels, both lower by USD (-10/mt) from the previous week. HDPE injection grade prices were assessed at the USD 950-970/mt CFR levels while HDPE yarn grade prices were assessed at the USD 960-980/mt CFR levels, both week on week declined by USD (-10/mt).

In Sri Lanka, a Saudi Arabian producer has offered its HDPE film grade at the USD 970/mt CFR levels, for shipment in September 2025. A overseas producer has offered its HDPE film grade at the USD 990/mt CFR levels, for shipment in September 2025.

In Bangladesh, HDPE blow moulding prices were assessed at the USD 920-960/mt CFR levels, down USD (-20/-30/mt) from last week. HDPE film prices were assessed at the USD 930-970/mt CFR levels, a week on week decrease of (-10/-20/mt) from the previous week. HDPE Injection grade prices were assessed at the USD 920-960/mt CFR levels and HDPE yarn prices were assessed at the USD 920-960/mt CFR levels, both down adjusted by USD (-10/-20/mt) week on week.

In Bangladesh, a Saudi Arabian producer has offered its HDPE film grade at the USD 970/mt CFR levels, for shipment in September 2025. A Middle Eastern producer has offered its HDPE film grade at the USD 930/mt CFR levels, for shipment in September 2025.

In Sri Lanka and Bangladesh, HDPE prices kept falling, influenced by soft purchasing demand and reduced import offers from regional and global suppliers. Abundant stocks at regional warehouses and ports strengthened the declining trend, while currency shifts and weak demand from key downstream industries like packaging and general manufacturing led to buyers becoming largely inactive. With supply surpassing existing consumption rates and no evident indications of a short-term demand rebound, market sentiment continues to be negative, and prices are anticipated to remain under stress. Moreover, decreased offers from international suppliers have added more pressure to the market.

A converter noted that across the Asian region, reports indicate that multiple transactions occurred at prices lower than the current price evaluations, highlighting the intensely competitive and weak market conditions. These agreements were primarily motivated by urgent needs instead of pre-emptive stocking, as purchasers stayed wary due to unpredictable demand forecasts and abundant supply. This necessity-driven buying trend highlights the dominant negative sentiment, as participants refrain from making substantial commitments and concentrate solely on meeting essential orders.

Feedstock ethylene prices on Tuesday were assessed stable at the USD 825-835/mt CFR South East Asia levels. Meanwhile, CFR North East Asia ethylene prices were assessed at the USD 820-830/mt levels, an increase of USD (+5/mt) week on week.

In plant news, Sinopec Maoming Petrochemical is likely to shut down its High density polyethylene (HDPE) unit in end October 2025 for maintenance. The plant is slated to remain offline until end December 2025. Located in Maoming, China, the HDPE unit has a production capacity of 350,000 mt/year.

In other plant news, USI Corp is likely to take off stream its High density polyethylene (HDPE) unit in the first half of August 2025 for maintenance. The plant is slated to remain offline for abound 20 to 25 days. Located in Kaohsiung, Taiwan, the HDPE unit has a production capacity of 160,000 mt/year.