Click the icon to add a specified price to your Dashboard list. This makes it easy to keep track on the prices that matter most to you.

This week, PVC prices were left unchanged in the Asian region. An industry source in Asia, on condition of anonymity, informed a Polymerupdate team member, “International oil prices have continued their upward trend, driven by heightened geopolitical tensions linked to the prolonged Russia-Ukraine conflict. Market sentiment has also been influenced by growing uncertainty around potential new U.S. sanctions that could target specific oil-producing nations, raising concerns over future supply disruptions and tightening global inventories..”

An industry source in Asia, on condition of anonymity, informed a Polymerupdate team member, “International oil prices have continued their upward trend, driven by heightened geopolitical tensions linked to the prolonged Russia-Ukraine conflict. Market sentiment has also been influenced by growing uncertainty around potential new U.S. sanctions that could target specific oil-producing nations, raising concerns over future supply disruptions and tightening global inventories..”

The source added "PVC prices stayed steady with the quotations from leading Asian PVC producers in October holding constant compared to September. Market participants observed that supply conditions were robust, and product availability in the region was plentiful, enabling buyers to obtain the material with ease. The steadiness in prices, along with sufficient inventory levels, fostered a balanced market situation, signalling no urgent demand for either price hikes or cuts. This indicates that both supply and demand fundamentals for PVC in the region are presently balanced, reinforcing a stable market perspective in the short term.”

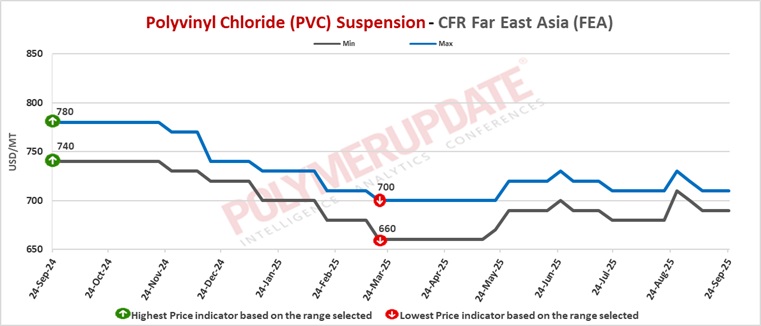

In China, PVC prices were assessed at the USD 690-710/mt CFR levels, rolled over from the previous week.

In China, a Taiwanese producer has offered its PVC resin suspension grade at the USD 710/mt levels, for shipment in October 2025.

The macro and industry outlook for PVC is bleak. There are no new updates prior to the National Day holiday, and market trends remain weak with demand for spot PVC noted to be low. The PVC spot market is stagnant, and an increase in supply is anticipated.

The maintenance activities of local PVC production enterprises are anticipated to experience deceleration, with steady production being the primary emphasis during the holiday season. Furthermore, a portion of the newly introduced production capacity will be fully leveraged, and market supply will revert to elevated levels. Domestic demand is expected to increase in small amounts prior to the holiday, while foreign trade exports are experiencing pressure from price competition. Industry inventories are anticipated to keep growing.

Concurrently, the spot prices for China's ethylene-based and carbide-based polyvinyl chloride (PVC) experienced some increases, attributed to rising prices in the nation's local yuan-denominated futures market. Nonetheless, increases were limited since local supply continued to be plentiful. Demand in the primary export market, India, was hampered by a prolonged monsoon season. Southeast Asia, a significant export market, experienced scattered instances of restocking despite overall stable market conditions. Demand continues to be weak as numerous converters are well supplied due to the extended supply surplus.

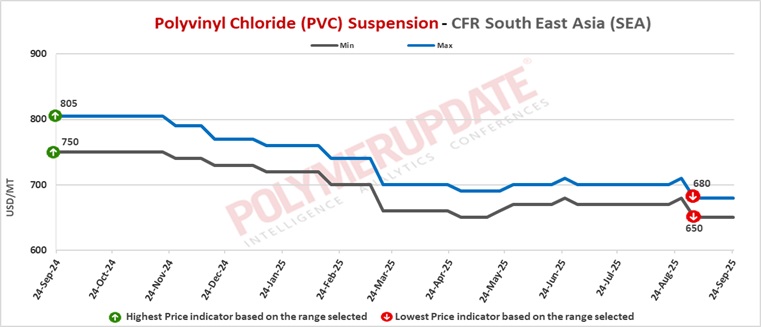

In Southeast Asia, PVC prices were assessed stable at the USD 650-680/mt CFR levels.

In South East Asia, a producer from Taiwan has offered its PVC resin suspension grade at the USD 670-680/mt levels, for shipment in October 2025.

In the markets of China and Southeast Asia, sentiment was noted to be subdued as participants took a cautious approach in anticipation of the forthcoming holidays. Trading activity diminished as both buyers and sellers adopted a cautious stance, leading to limited market fluctuations. The pause in activity demonstrates typical pre-holiday attitude, as market participants refrain from significant deals until after the holiday season, leading to a briefly subdued trading atmosphere throughout the region.

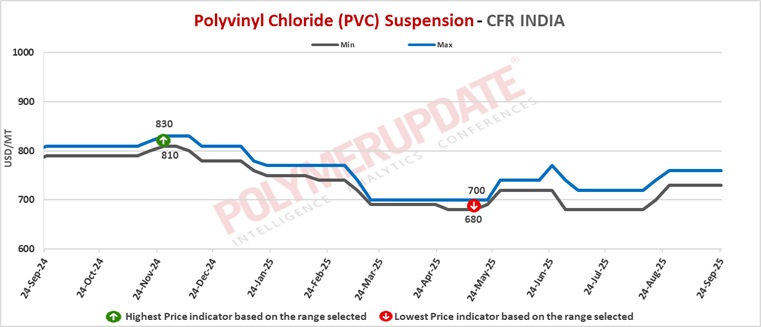

In India, PVC prices were assessed at the USD 730-760/mt CFR levels, constant week on week.

RIL has announced price protection in PVC wef September 16, 2025 till October 01, 2025, 6 am, or next price change, whichever is earlier.

A major Taiwanese producer has offered its PVC suspension grades (S65D/S65/S60/S70/B57) at the USD 760/mt levels on CIF Nhava Sheva/Mundra/Chennai ports basis with shipment for October 2025 (LC at sight). These offers have been rolled over from the previous month's offers.

In Pakistan, PVC prices were assessed flat at the USD 695-725/mt CFR levels.

In Pakistan, overseas producers have offered their PVC resin suspension grades in the range of USD 695-725/mt levels, for shipment in October 2025.

In Pakistan, spot demand remained weak as heavy rainfall and flooding hindered downstream offtake. Spot offers stayed constrained, and low purchasing interest coupled with restricted market conversations maintained muted market activity. Abundant regional supply has left buyers reluctant, with weaker offers anticipated for both local and imported volumes. Market participants anticipate that reconstruction demand in areas affected by floods will offer an extra lift as post-monsoon activities pick up pace.

In Sri Lanka, PVC prices were assessed at the USD 690-720/mt CFR levels, constant from the previous week.

In Sri Lanka, overseas producers have offered their PVC resin suspension grades in the range of USD 690-720/mt levels, for shipment in October 2025.

The overall fundamentals in the Sri Lanka market remained broadly unchanged as compared to the prior week, even as regional supply continues to exceed softened demand sentiments, indicative of dampened market conditions.

In Bangladesh, PVC prices were assessed steady at the USD 680-720/mt CFR levels.

In Bangladesh, overseas producers have offered their PVC resin suspension grades in the range of USD 680-720/mt levels, for shipment in October 2025.

Demand for PVC has been weak, limited by the abundant supply of cheaper Chinese material. Prices were mostly stable throughout the week as additional suppliers offered price discounts to encourage buying interest. Nonetheless, spot demand continues to be viewed primarily on a necessity basis and is influenced by ongoing price inelasticity.

In upstream developments, India has extended the deadline for implementing the Bureau of Indian Standards (BIS) certification mandate for EDC (Ethylene Dichloride) and VCM (Vinyl Chloride Monomer) to September 12, 2026. This extension allows producers and importers more time to meet the certification requirements, guaranteeing that products adhere to the specified quality and safety standards. The move aims to alleviate immediate compliance burdens on manufacturers while ensuring regulatory oversight of essential chemical intermediates in the Indian market.

Feedstock EDC prices were assessed at the USD 185-195/MT CFR China levels while CFR South East Asia EDC prices were assessed at the USD 195-205/MT levels, both unchanged week on week.

CFR South East Asia VCM prices were assessed flat at the USD 540-550/mt levels and CFR China VCM prices were assessed steady at the USD 505-515/mt levels.

Feedstock ethylene prices on Tuesday were assessed at the USD 840-850/mt CFR North East Asia levels, a fall of USD (-5/mt) from the previous week. Meanwhile, CFR South East Asia ethylene prices were assessed flat at the USD 835-845/mt levels.

In plant news, Hanwha Solutions is likely to take off stream its No.1 Polyvinyl chloride (PVC) plant around November 4, 2025 for maintenance. The unit is likely to remain offline for about one week. Located in Ulsan, South Korea, the No.1 plant has a production capacity of 210,000 mt/year.

In another plant news, Hanwha Solutions Chemical is likely to shut down its No. 2 Polyvinyl chloride (PVC) plant for maintenance turnaround from November 4, 2025, with operations expected to resume on November 10, 2025. Located in in Ulsan, South Korea, the No.2 plant has a production capacity of 95,000 mt/year.